复

黄仁勋在 GTC 2026 上都说了什么?(给技术小白通俗版本)

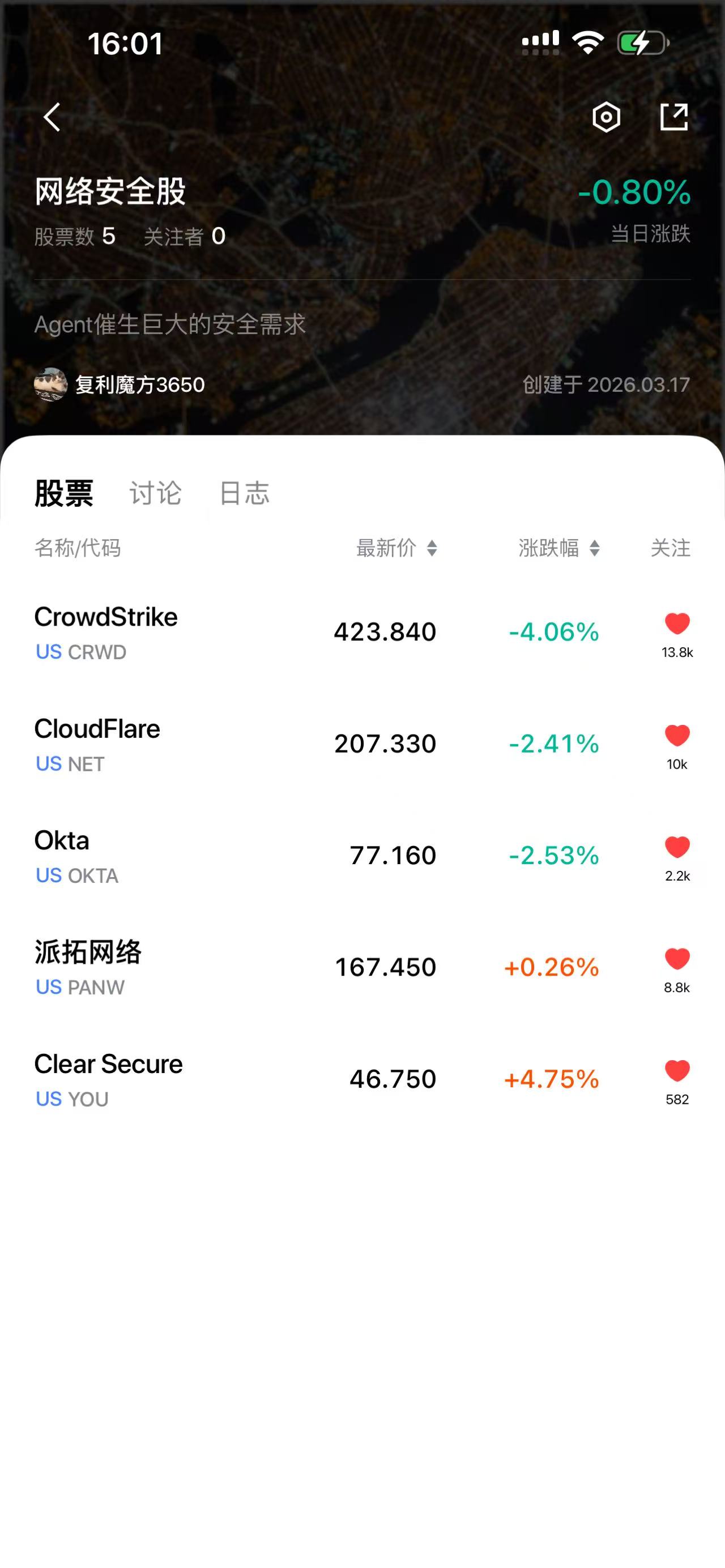

写在前面,我认为英伟达还是 2026 年比较确定的标的,理由:云大厂还是非常疯狂地砸算力(四巨头资本开支合计,约 6350 亿美元,+55%)Agent 时代的来临,算力需求爆炸了,有点像 ChatGPT 时刻去年和今年,英伟达还没怎么涨,这是重点,哈哈哈另外,网络安全股,也很可能值得关注,Agent 会催生大量安全的需求,我接触的到一些公司,担心安全问题,禁止本地部署。。。也就是说,实用...

Nvidia~

写在前面,我认为英伟达还是 2026 年比较确定的标的,理由:云大厂还是非常疯狂地砸算力(四巨头资本开支合计,约 6350 亿美元,+55%)Agent 时代的来临,算力需求爆炸了,有点像 ChatGPT 时刻去年和今年,英伟达还没怎么涨,这是重点,哈哈哈另外,网络安全股,也很可能值得关注,Agent 会催生大量安全的需求,我接触的到一些公司,担心安全问题,禁止本地部署。。。也就是说,实用...

The market didn't buy Jensen Huang's story last night? The market showed no mercy as NVIDIA's stock price still plummeted. Even more embarrassing, NVIDIA's overnight drop happened right after Jensen Huang began his keynote speech. I think the main reasons are: first, the overall market was weak with the Nasdaq down nearly 2%; second, NVIDIA had already rebounded over 10 points, so the GTC positive news was already priced in; third, the market is too short-term focused and failed to recognize that this Show should be viewed from the perspective of long-term AI development...

+1

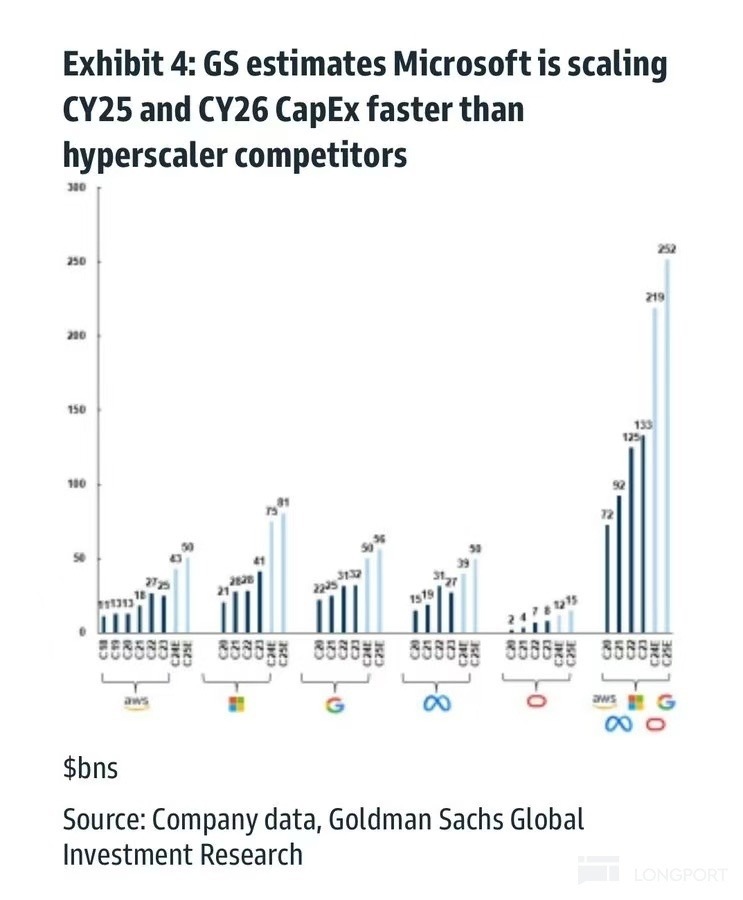

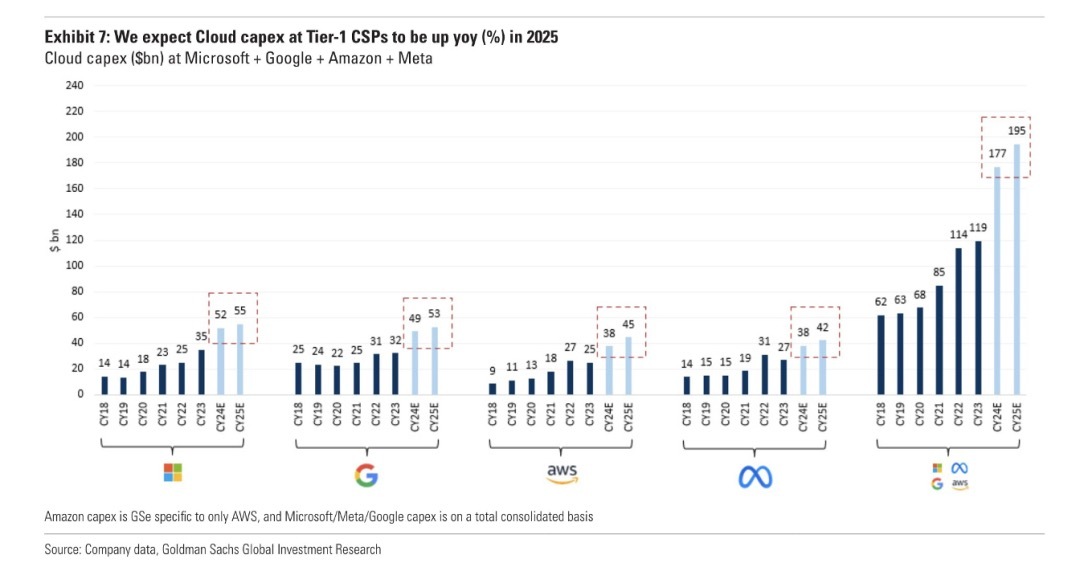

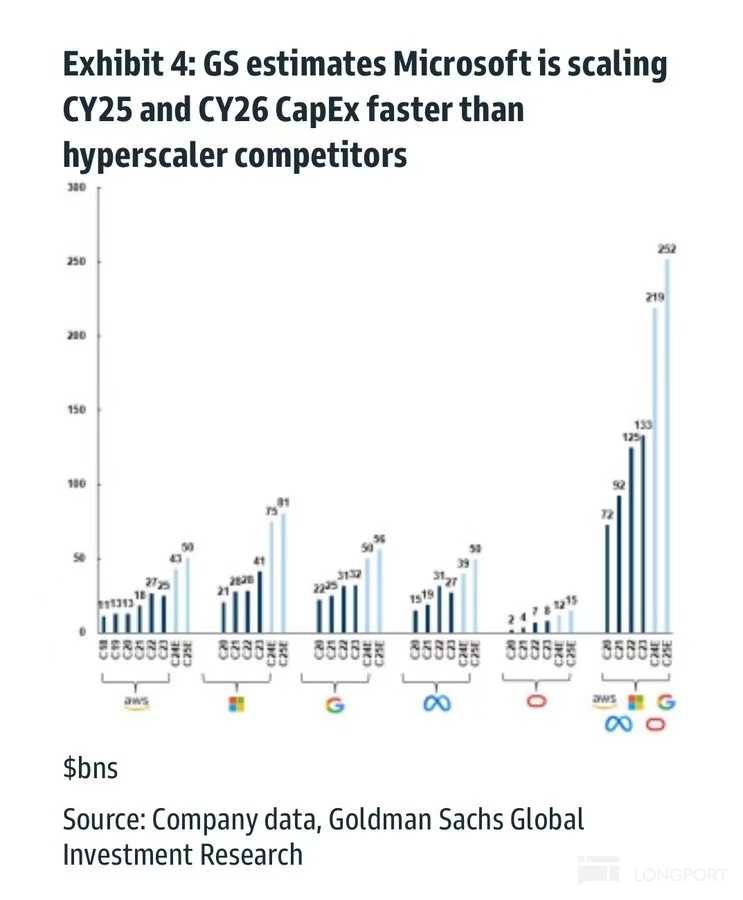

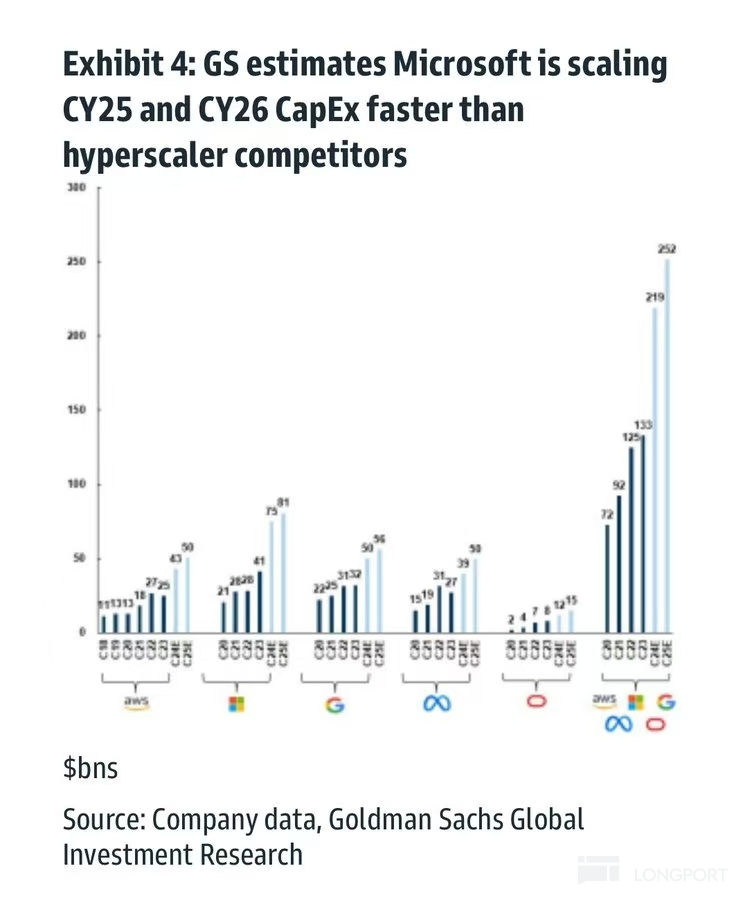

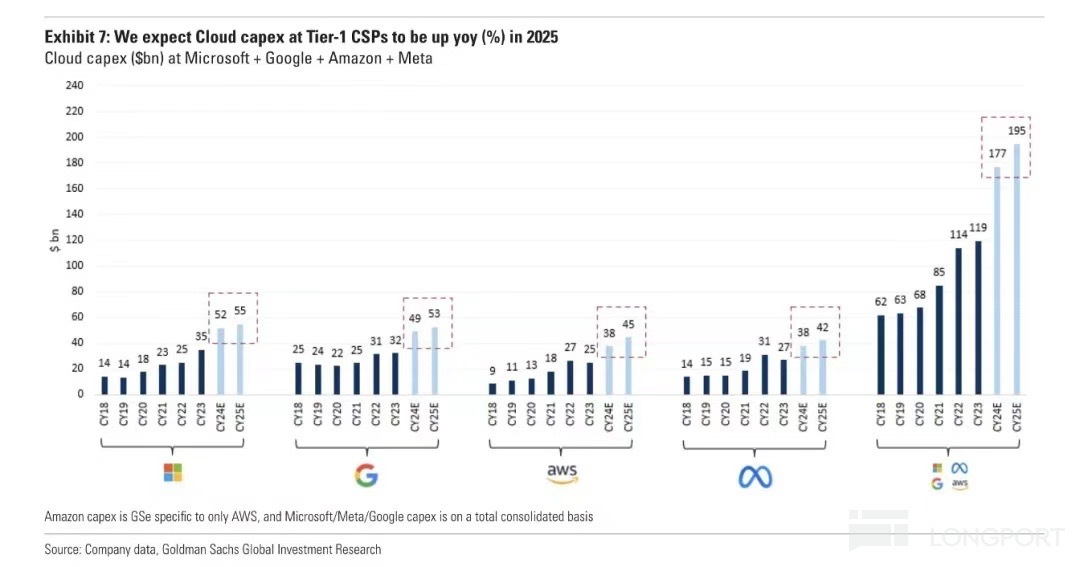

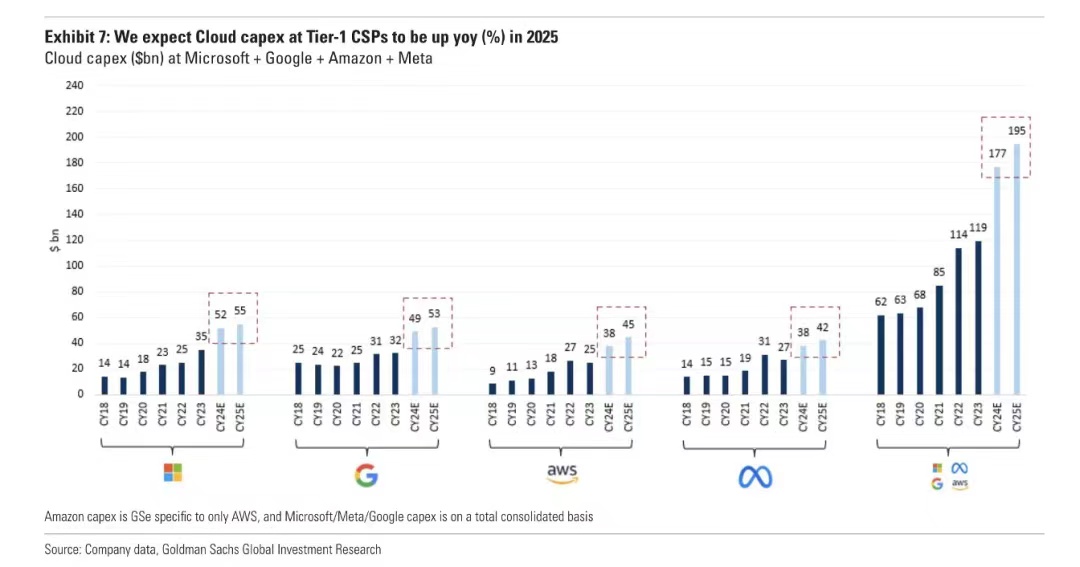

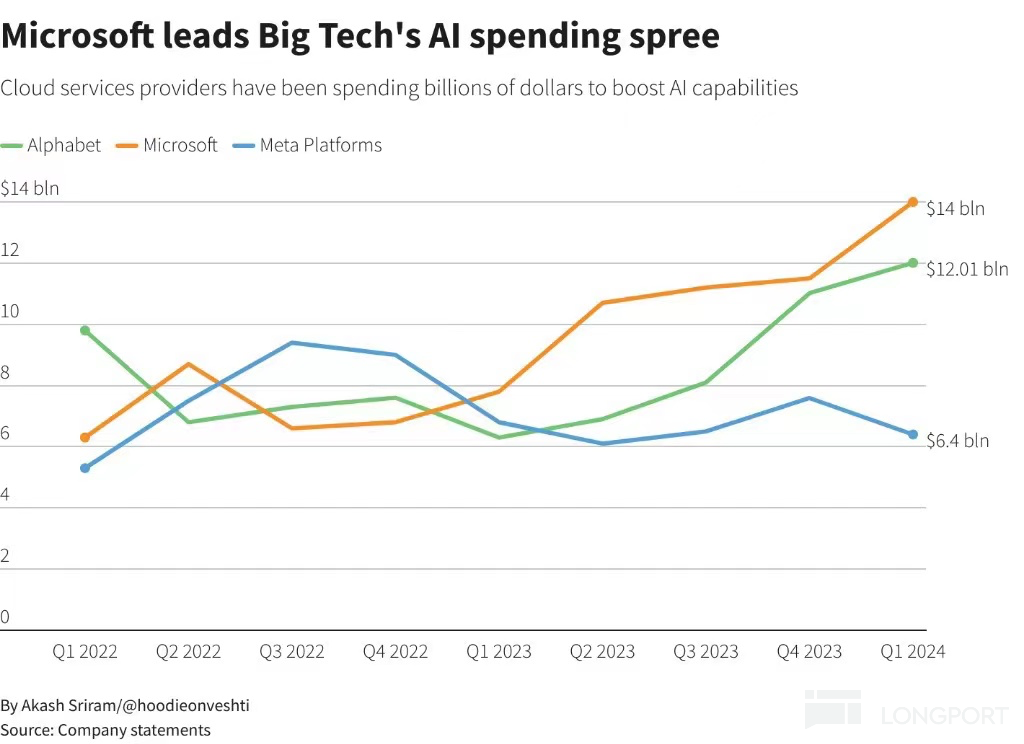

+1Analysis of the capital expenditures of major companies: Last year, Goldman Sachs made predictions in May and October regarding the capital expenditures of major giants such as Microsoft, Google, Meta, and Amazon (all major clients of Nvidia). The two forecasts estimated growth of 14% and 15% respectively by 2025. At the end of October and the beginning of November, several major companies announced their financial reports, indicating an upward adjustment in capital expenditures. So what is the real situation? Recently, Microsoft, Google, Amazon, and Meta all released their financial reports. Alphabet announced on Tuesday that its capital expenditure plan for this year is $75 billion...

Regarding NVIDIA's rare downgrade of target price by HSBC: the target price has been lowered from $195 per share to $185 per share (based on a 32 times PE valuation). HSBC also reduced NVIDIA's earnings per share forecast for the fiscal year 2026 by 6%. Reason: It is expected that NVIDIA's GB200 supply chain issues will continue into the first half of fiscal year 2026 (from February 2025 to July 2025), resulting in limited "upside" growth potential for NVIDIA in the first half...

Non-investment advice, everyone, just take a look. I believe the most important thing in stock trading is trading expectations, and among those expectations, the most important is the expectation of performance growth. Goldman Sachs made a prediction in October, estimating the capital of several giants including Microsoft, Google, Meta, and Amazon (all major clients of Nvidia) to grow by 64% in 2024 (USD 219 billion) and by 15% in 2025 (USD 252 billion). At the end of October and the beginning of November, several giants announced their financial reports, and capital expenditures were slightly adjusted upwards. For example, Meta, Mark Zuckerberg said...

Riding the trend, but not recommending gambling on options before earnings unless you're very confident and have sufficient cash flow (it's okay to lose). As for this earnings report, it's hard to understand, details here: Nvidia's earnings tomorrow morning, bullish or bearish? Let's talk about options. Having played with derivatives for years, from leveraged trading in A-shares in 2014, buying warrants in 2018, to trading US stock options later. Got plenty of experience, both good and bad. Sharing here, newbies might want to take a look. I think there's only one way to make money with options, and big money at that: buying long-term, low-priced options...

+2

+2First, the conclusion: This time it's unclear, with no clear bullish or bearish view. If forced to give a view, it's 55% bearish and 45% bullish. The last two times were clearly bullish, mainly because the market cap was low (1.66 trillion and 2.33 trillion respectively), the bull market sentiment was strong, and earnings growth was rapid. The main reasons for the uncertainty this time: 1. The current price level is a bit awkward, with a market cap of 3.15 trillion, and the rebound has already surged from 90 to 130. This earnings report is different from the previous two—the current market cap is not low. 2. This quarter's earnings...

+1

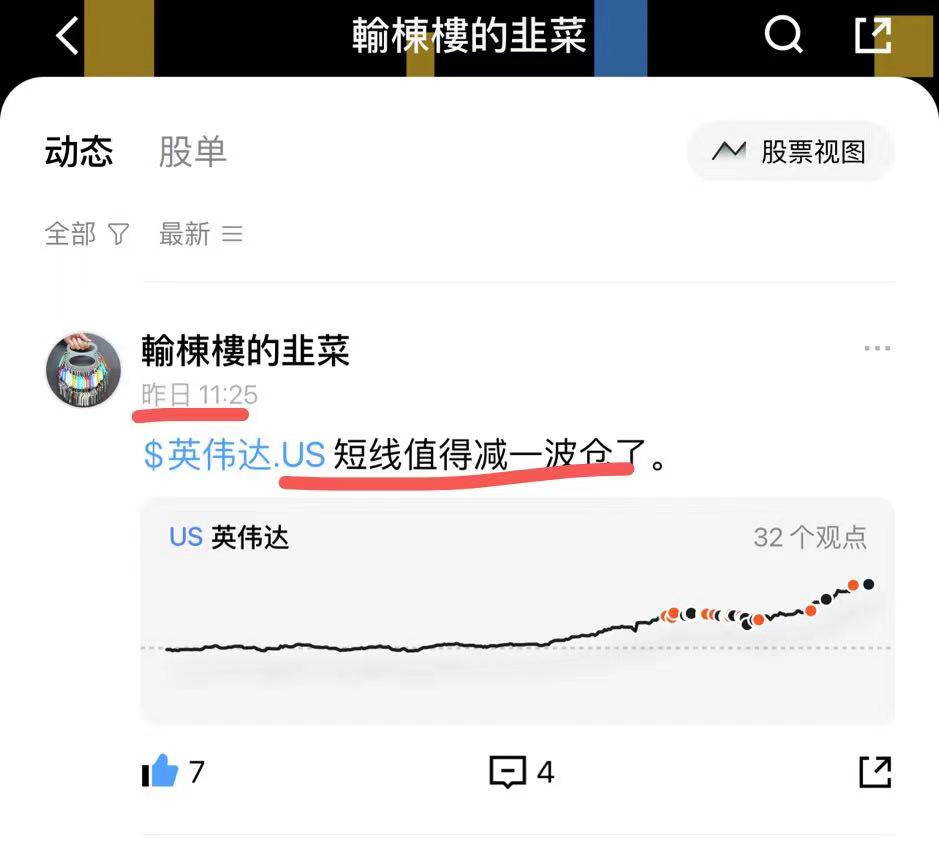

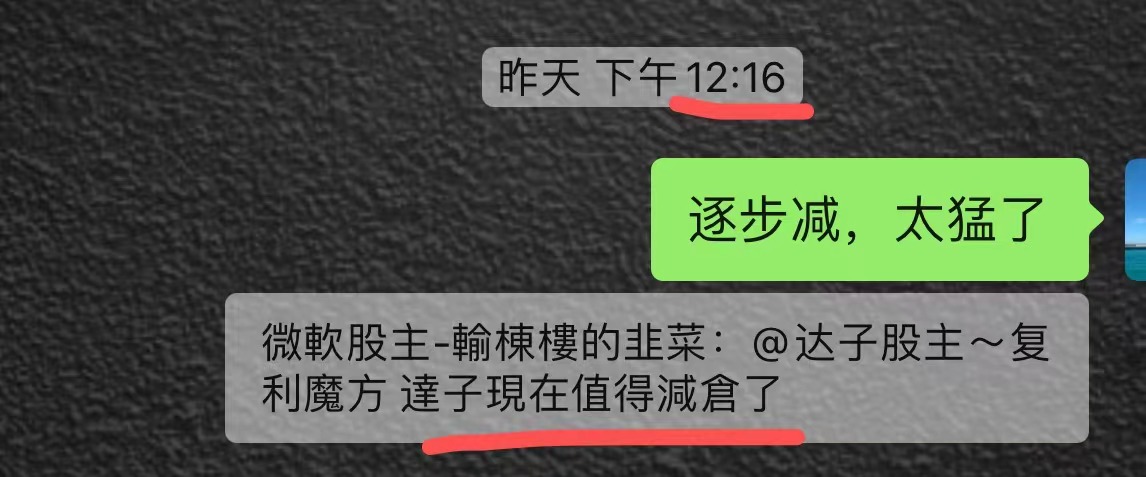

+1Yesterday morning, I saw NVIDIA's after-hours trading surge again, which felt a bit crazy. (Additionally, tonight is the quadruple witching day, with trillions of derivatives expiring, so volatility should be relatively high.) These past few days, I’ve been a bit worried that this wave of AI frenzy might be peaking (though I don’t know exactly when). Coincidentally, StockPro from Microsoft also mentioned it yesterday at noon, suggesting gradually reducing short-term positions—I quite agree. $3.3 trillion has already surpassed my aggressive target of $3 trillion (set for 2024). I’m not entirely sure about the future trend, as it’s beyond my understanding now. Everyone has a fear of heights, after all. But I know...

+5

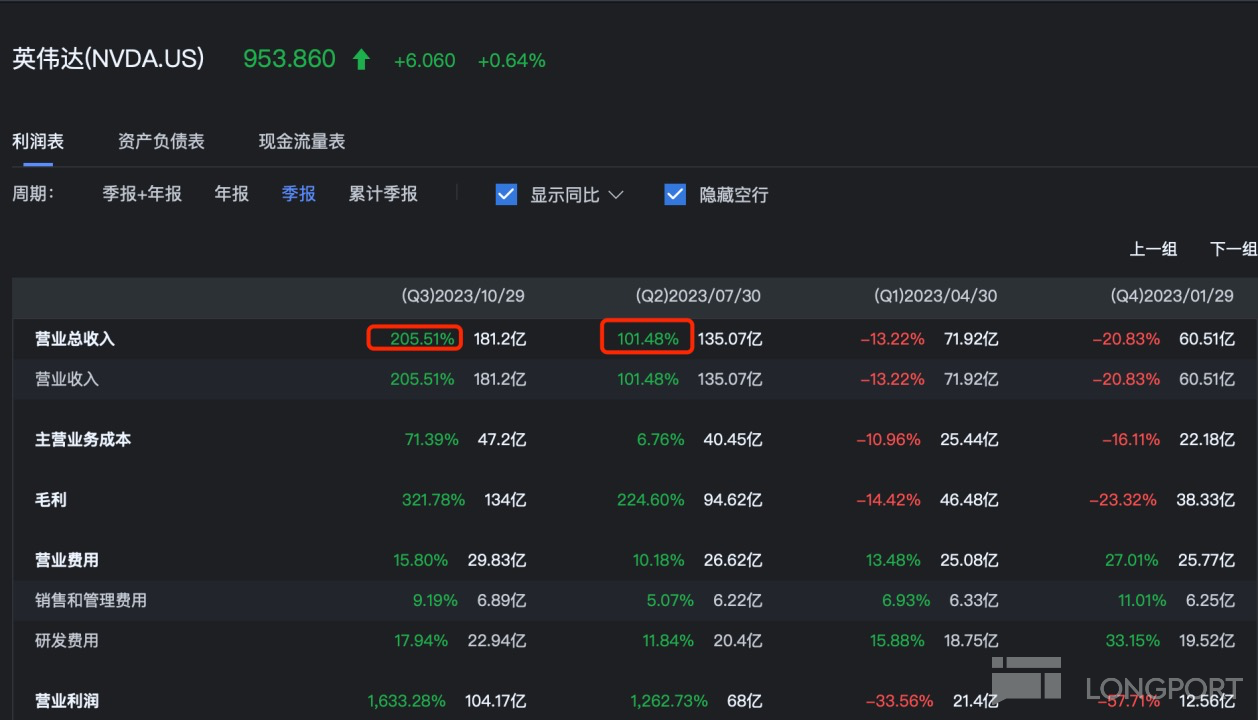

+5The main reasons are: 1. Outstanding performance; 2. Strong demand for GPUs, with major customers' capital expenditures continuing to surge; 3. The index has hit a new high, the big brother is back. 1. Outstanding performance. I've shared this chart multiple times since April 8th (EPS growth quadrupled), mainly because the growth expectations are very clear. Analysts predict NVIDIA's Q1 revenue to reach $24.69 billion, a year-over-year increase of 243.3%. Growth is still accelerating, with last quarter's growth at 205%...

+1

+1先说核心观点:继续看多;那如果财报没有达到已经拉满的预期呢,那肯定下跌 ---- 下跌就是机会呀!不构成投资建议。我个人观点很强烈,多就是多,空就是空,看不懂就是看不懂,打脸也很常见,都是概率问题。继续看多理由如下 1、业绩分析具体数据我也懒得分析了,除了大涨就是大涨,具体看他们弄的这篇内容:一文速览 | 英伟达财报前瞻合集来了!关注的重点是:2,产品线 H100 的需求情况(肯定是爆满的啦)...

+6

+6