D

TSLA (Q1'26 Trans): $25bn All-In Bet, When Will AI Monetize?

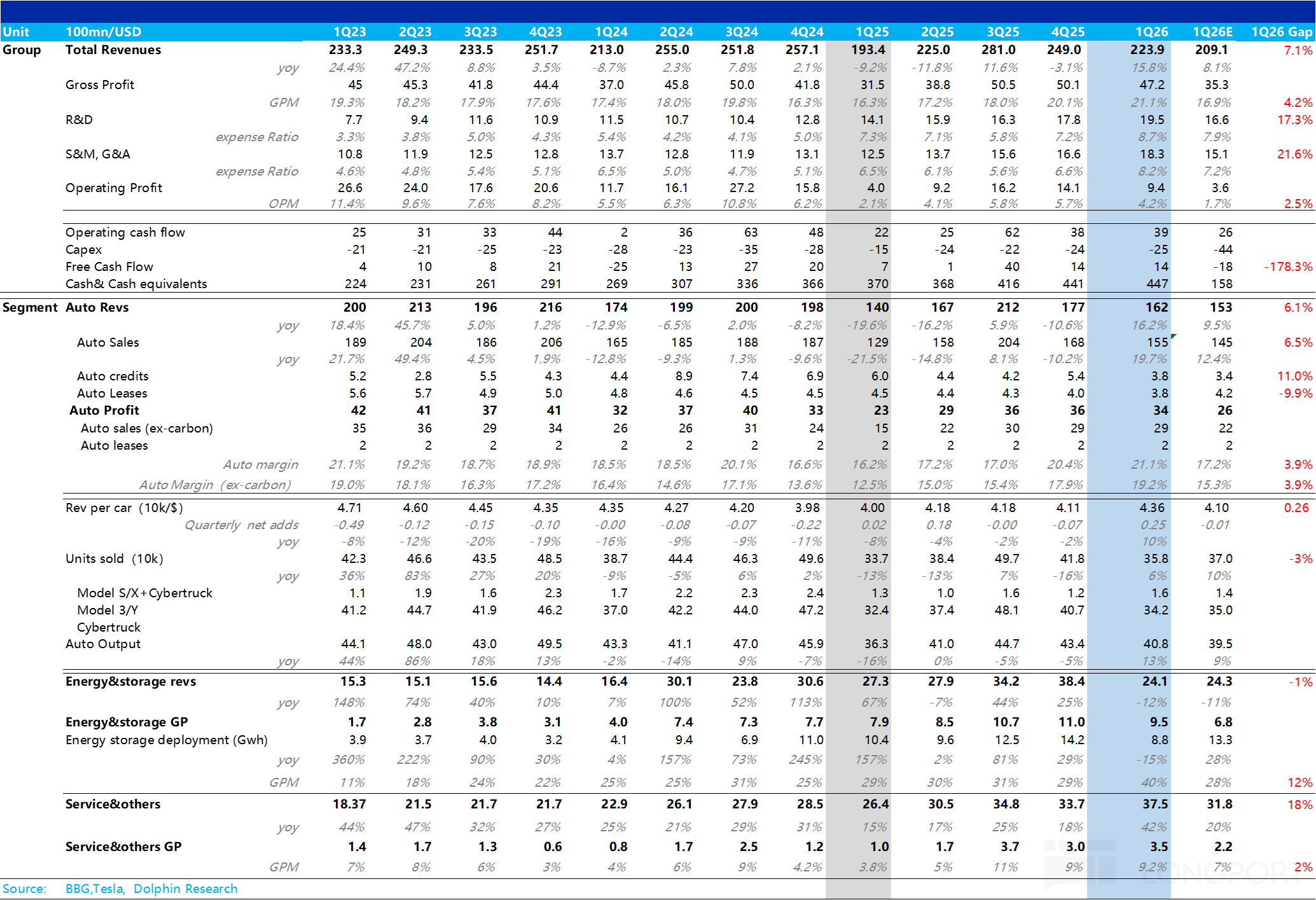

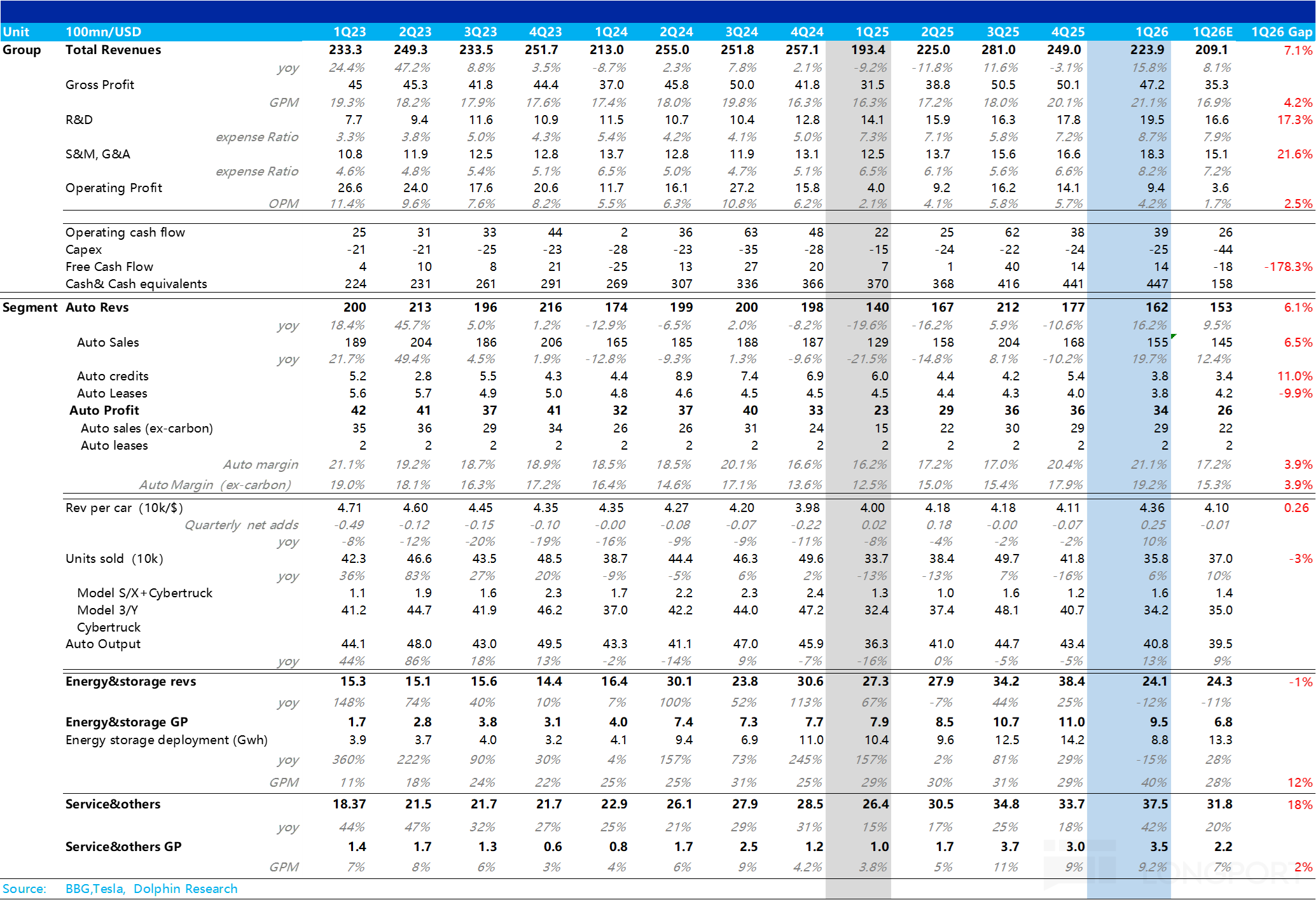

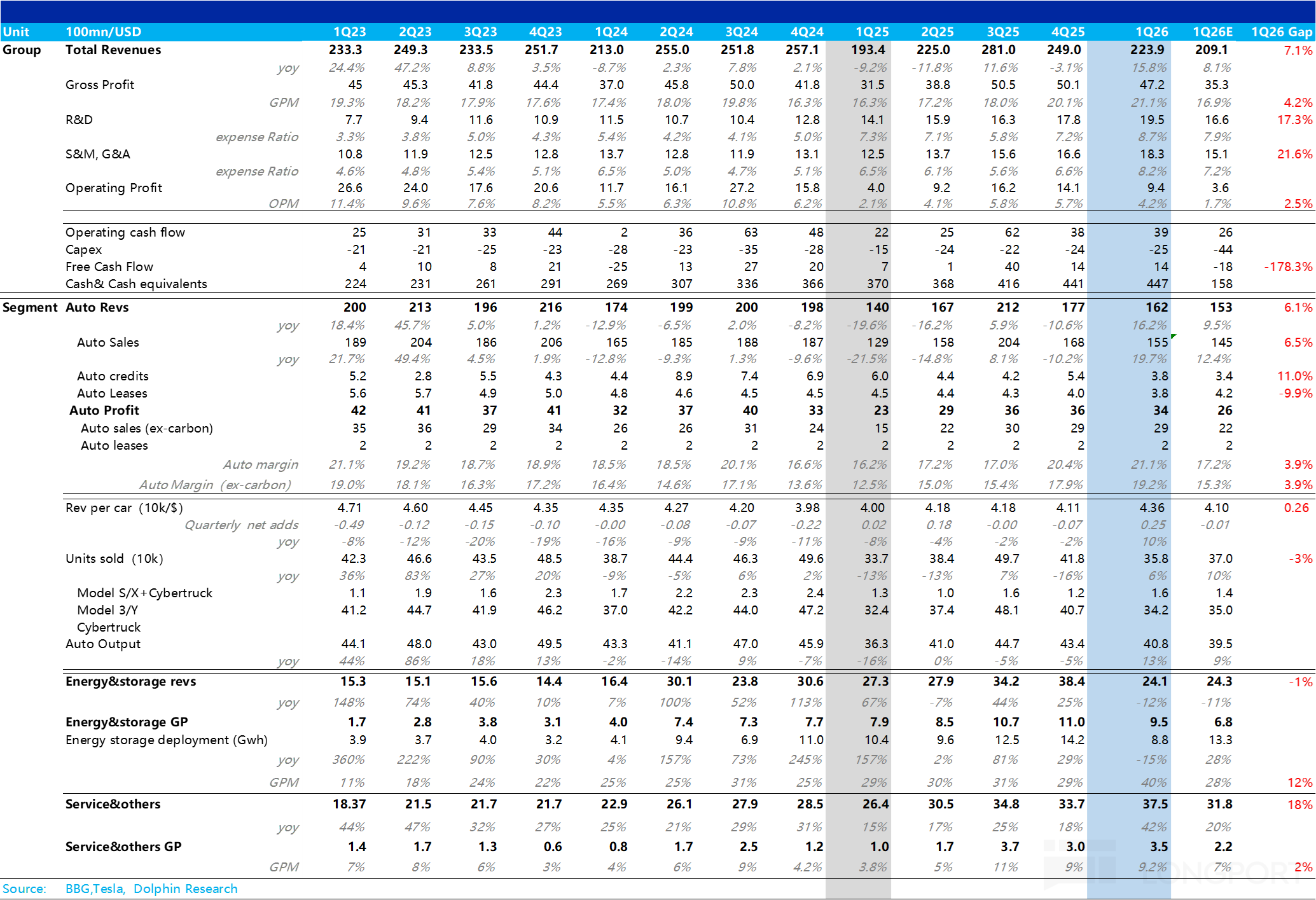

FY26 CapEx is expected to exceed $25bn. The company is in a heavy investment cycle that is likely to last several years.

TeslaConference Minutes

FY26 CapEx is expected to exceed $25bn. The company is in a heavy investment cycle that is likely to last several years.

Is the monetization timeline for the big AI push slipping again?

+17

+17CyberCab's long-term annual production target will exceed the company's current aggregate output of all legacy models. In other words, it aims to produce more than all traditional models combined.

The auto sales business has not slipped into a vicious cycle where soft volumes drag down earnings. Results remain resilient despite volume pressure.

+21

+21TSLA at $1.5tn: priced for the future, or still undervalued as an AI crown jewel?

+16

+16Can Robotaxis turn ride-hailing from a low-margin business into a cash cow?

+23

+23The following are the minutes of the FY25Q3 earnings call for $Tesla(TSLA.US) organized by Dolphin Research. For earnings interpretation, please refer to "Tesla: Relying on the Stars and the Sea, It's Time to Pay for Faith Again." Summary of Tesla Minutes: 1. Automotive Business: Existing capacity will reach an annualized production rate of 3 million units within 24 months (possibly sooner), with the core increment coming from the Cybercab model, which will be launched in the second quarter of 2026. This model is optimized for full autonomous driving, with no steering wheel or pedals, focusing on minimizing operational costs. On the demand side, no additional stimulus is needed...

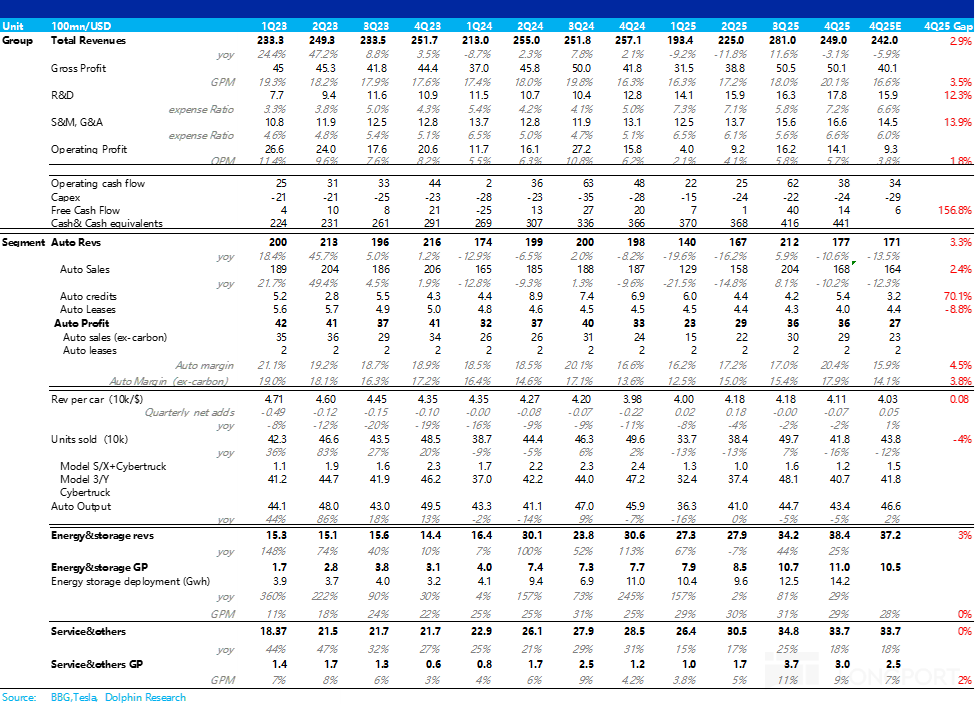

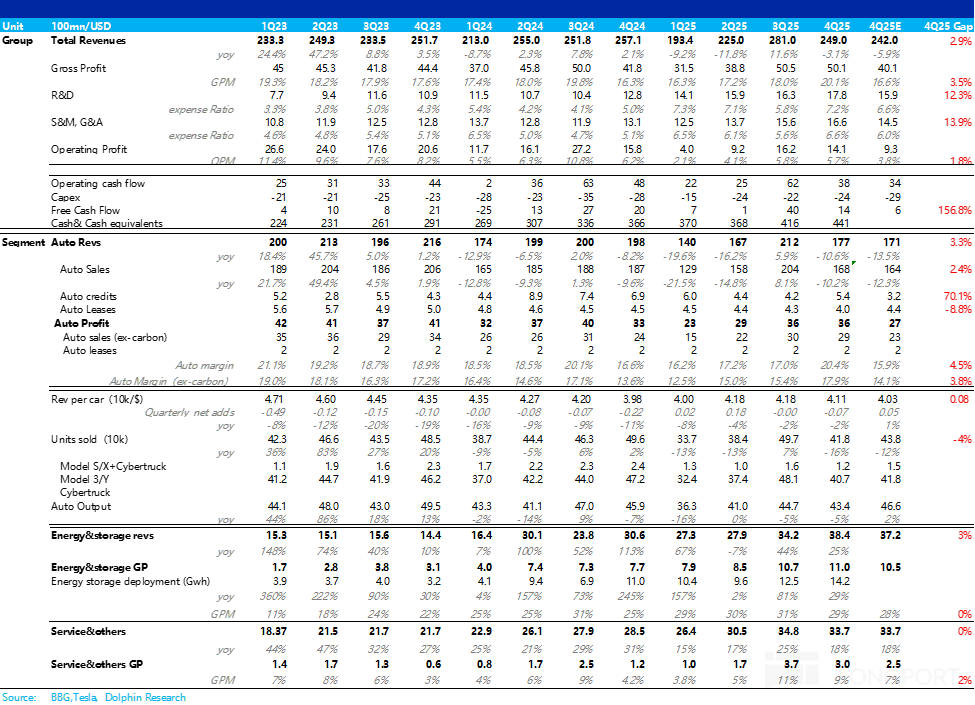

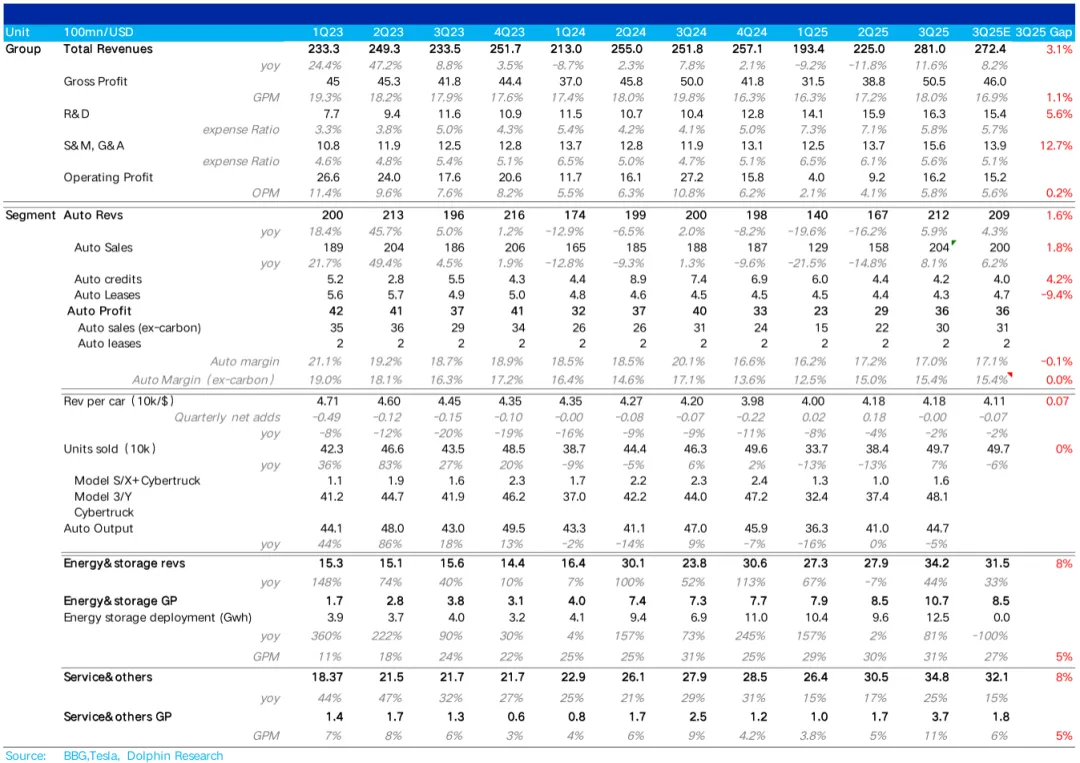

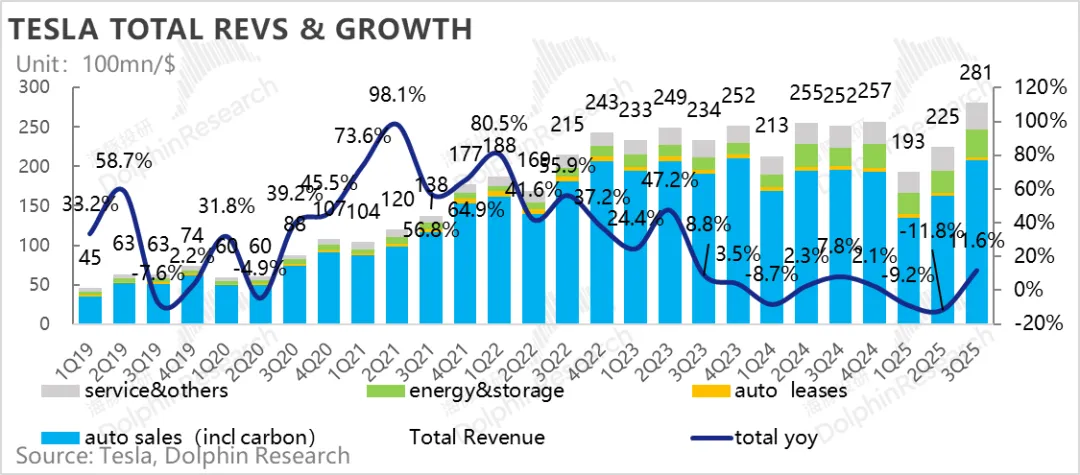

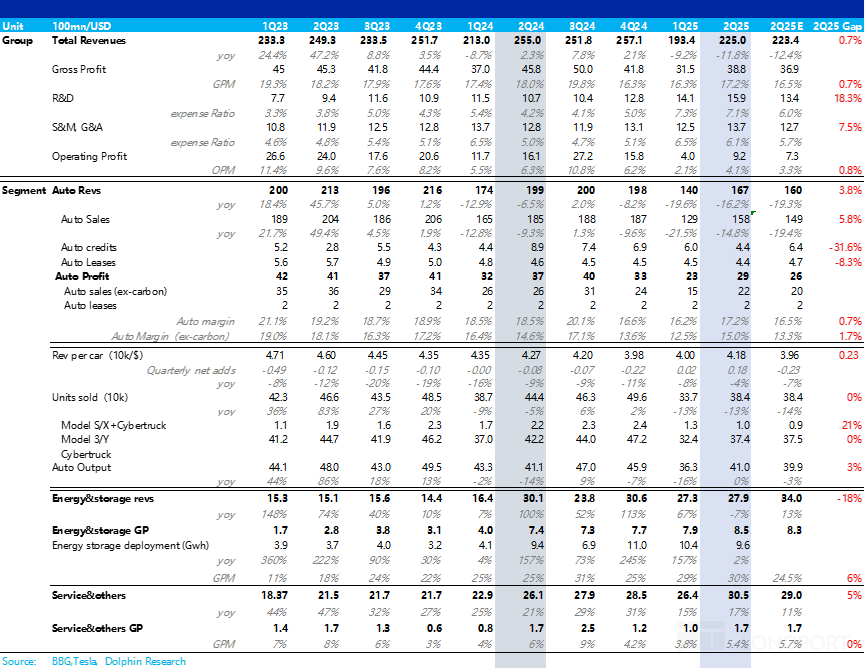

$Tesla(TSLA.US) released its Q3 2025 earnings report after the U.S. stock market closed on October 23rd, Beijing time. In summary, the third-quarter performance was decent, but Tesla is inherently a stock priced for the future, especially at the current relatively high price of $439. However, Tesla's guidance on several key business expectations is not optimistic. Here are the core details: 1. Total revenue performed well: This quarter's total revenue was $28.1 billion, exceeding the market expectation of $27.2 billion. Revenue from energy storage and service businesses both increased quarter-on-quarter, while the most critical car sales revenue...

+13

+13In the near term, fundamentals are still expected to remain under pressure, but Tesla continues to make solid progress on its visionary initiatives such as Optimus and the Robotaxi/FSD businesses

$Tesla(TSLA.US) Tesla(TSLA.O) released its Q2 2025 earnings report after the U.S. stock market closed on July 23rd, Beijing time. In summary, the second-quarter performance was decent, but Tesla is inherently a stock priced for the future, especially at the current relatively high price of 330. High stock price and low expectations mean that exceeding expectations is not worth celebrating. Here are the key points: 1. Total revenue performed well: This quarter's total revenue was $22.5 billion, exceeding market expectations by about $200-300 million...

+17

+17