SKHY

----

熊

2 days ago, 09:39 PM

In the era of AI hardware, the landscape has changed.

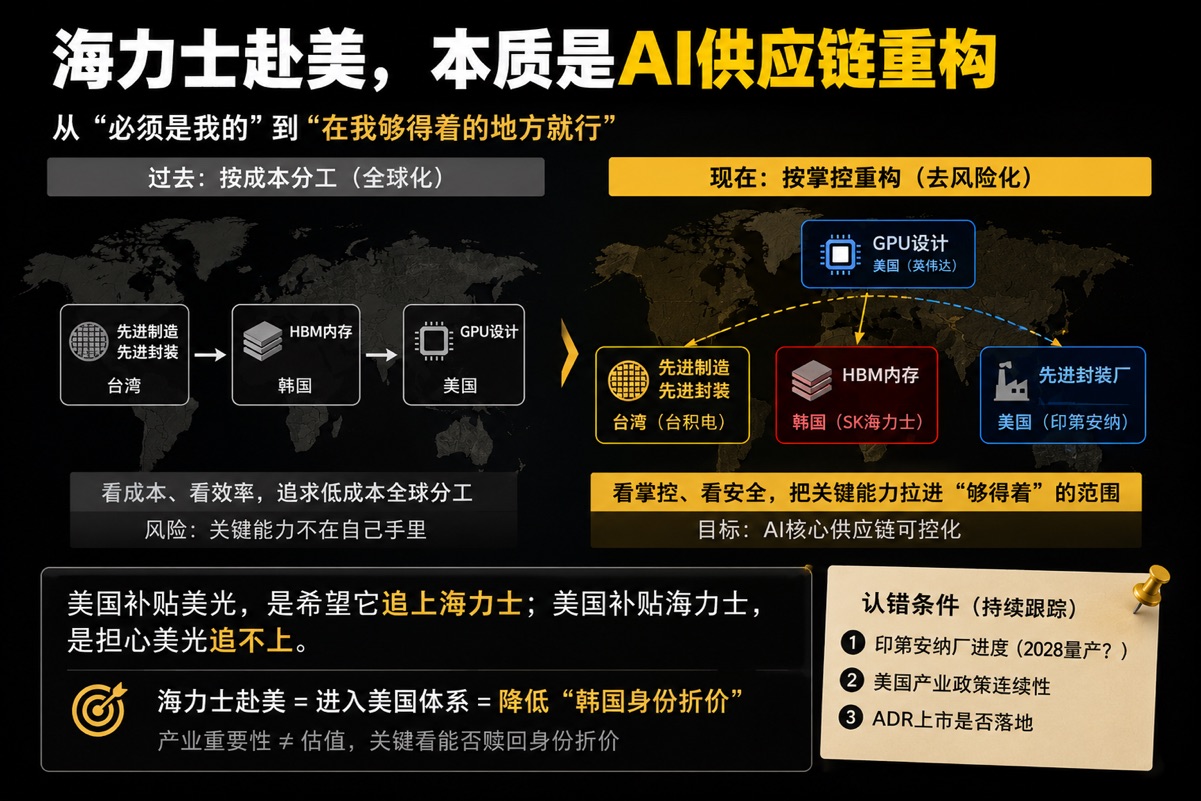

The "brain" of AI—the GPU—is America's NVIDIA. But its "body parts" are scattered across the globe: the strongest HBM is with South Korea's SK Hynix, the most advanced chip manufacturing and packaging is with Taiwan's TSMC, and even the lithography machines that make the chips are with the Netherlands' ASML.

The US holds the brain of AI, but cannot build a complete body for AI.

This is the real reason behind the US subsidies for SK Hynix. In the HBM segment, relying on Micron alone is not enough to catch up—SK Hynix holds 57% of the global HBM market share, while Micron only has 24%; SK Hynix has long been the king of HBM, while Micron is still struggling to catch up on its transformation path (this is exactly what the previous article discussed). The US can use money to help Micron build factories, but "being able to build factories" and "being able to produce the most cutting-edge HBM" are two different things. The latter requires the decade-accumulated technical foundation of SK Hynix, which money cannot buy and cannot be quickly caught up with.

$SK Hynix(SKHY.US)$Micron Tech(MU.US)$SK Hynix - WI(SKHYV.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.