Canaan Technology 4000-word in-depth research report

$Canaan(CAN.US)$比特大陆(BTDLL.HK) $SAIMO(02571.HK) Reviewed Canaan Technology's (CAN.US) research report, the key finding is that this leading Bitcoin mining machine manufacturer's performance fluctuates sharply with industry cycles, but Q2 2025 shows significant marginal financial improvement signals.

🎯Core Logic

- Main business: Bitcoin mining machine ASIC chip design and sales, asset-light Fabless model (no own wafer fab).

- Industry characteristics: Strong cyclicality (mining machine demand correlates over 80% with Bitcoin price); Fast tech iteration (miner lifespan 1.5-2 years); CR3 over 70% oligopoly competition.

- Expansion: Self-mining (hashrate ~10% of total sales), AI edge chips (e.g. K230), non-mining revenue <5%.

📈Financial Highlights

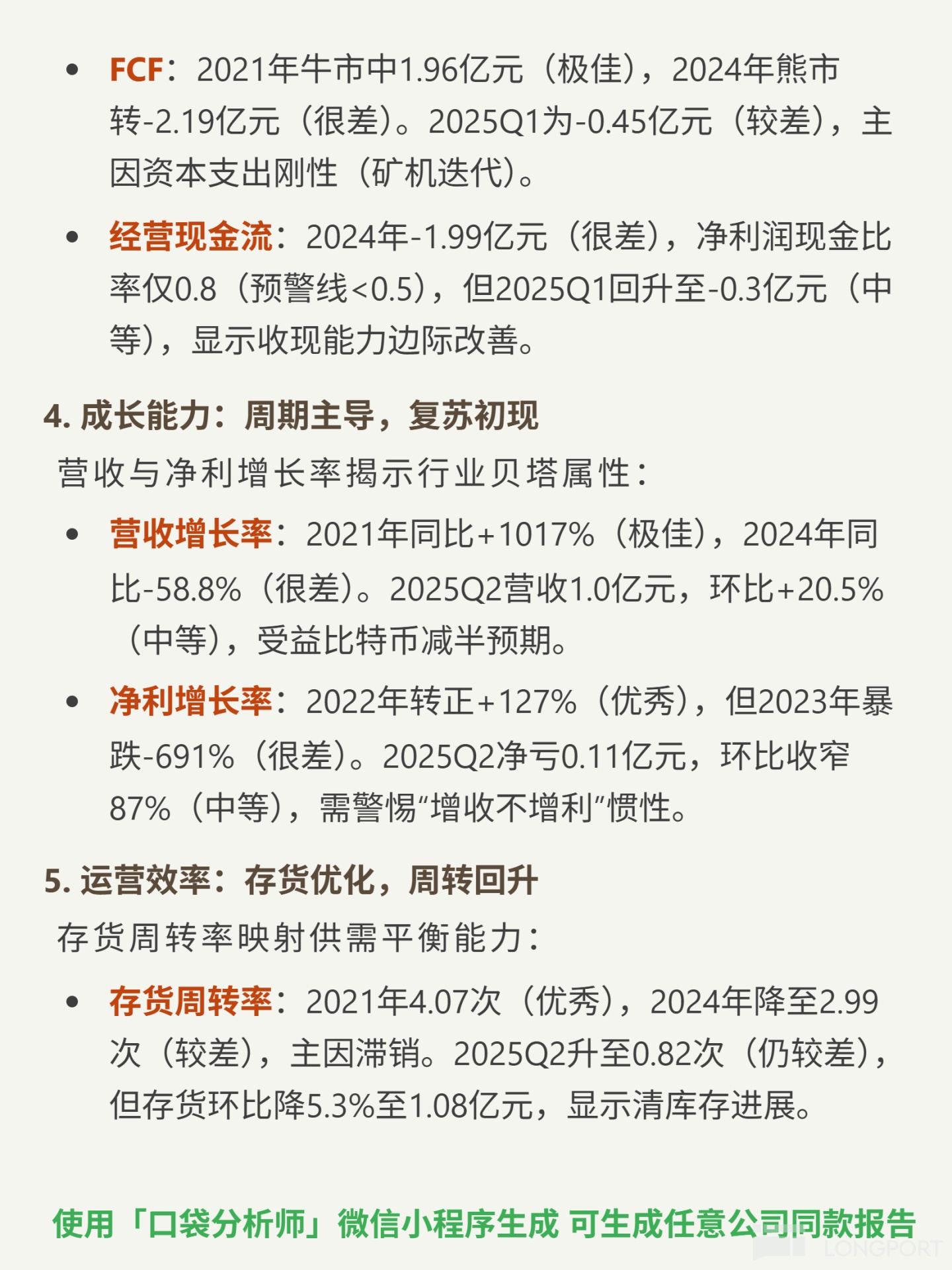

- Q2 2025 revenue: ¥100M, +20.5% QoQ (benefiting from Bitcoin halving expectations); Net loss ¥11M, -87% QoQ.

- Gross margin rebounded to 9.29%, ending negative streak; Debt ratio 45.35% (normal range), current ratio 1.78 (no liquidity crisis).

- Inventory -5.3% QoQ to ¥108M (clearance progress), but turnover still low (0.82x).

- Operating cash flow negative for 8 quarters, but financing covers, no imminent crash risk.

🔍Key Risks

- ROE still -3.89% (Q2 2025), profitability not fundamentally repaired;

- Non-mining business too small to form second growth curve.

(~420 words)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.