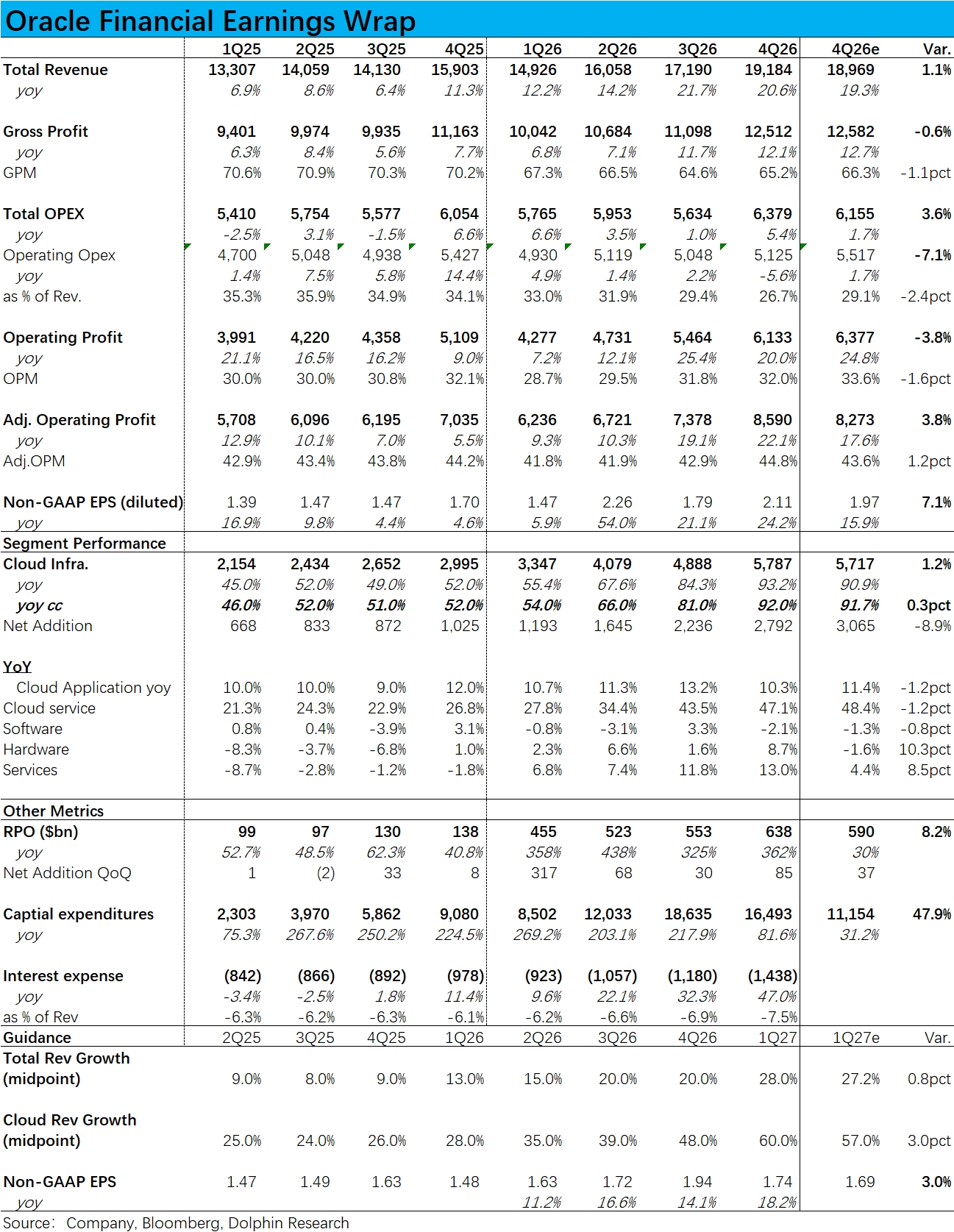

Oracle 4Q26 First Take: the company reported results for the quarter ended May this morning; overall muted, with few bright spots.

1) On growth, the key metric—OCI revenue—rose 92% in constant currency. It accelerated QoQ as expected, but landed squarely in line with the Street with no upside surprise.

By contrast, SaaS and on‑prem software revenue grew 10% and fell 2%, respectively. Growth kept slowing and came in slightly below expectations, underscoring pressure on the legacy franchise.Hardware and services both beat. However, combined they account for just a bit over 10% of mix, so the impact was limited.Total revenue was about 19.2bn, up 20.6% YoY. Growth ticked up modestly on OCI strength, or roughly +200bps ex‑FX, and came in slightly above consensus.

2) On new orders, RPO increased by 85bn QoQ to 638bn. With no chatter about fresh megadeals ahead of earnings, the Street was looking for about 590bn.

We suspect the recently disclosed cooperation with the U.S. Gov. is a likely source of new wins. In addition, contracts requiring customer prepayment or customer‑provided hardware now total 75bn, likely signed over the past two quarters.3) GPM missed again at 65%. It improved QoQ and shows signs of bottoming, but trailed the ~66% Street view.

By segment, cloud and software posted GPM of 68.8%, up from 68.2% in the prior quarter. The YoY decline remains notable; whether this is a blip or a trend inflection bears watching.4) Capex was roughly 16.5bn, down from 18.6bn in the prior quarter. Back‑solving from management’s prior full‑year capex guide of 50bn, the market had penciled in only about 11bn for the quarter, but a sharp pullback would be inconsistent with accelerating OCI demand.

On financing, management said it completed 43bn in bonds and 5bn in equity raises in FY26. For FY27, it plans another 20bn each in debt and equity (already disclosed), effectively securing most of next year’s capex.

5) Guidance: for next quarter, cloud (IaaS+SaaS) growth midpoint is 60%, signaling further acceleration. That is modestly ahead of the ~57% Street.

Non‑GAAP EPS midpoint is 1.74, implying +18% YoY and ~3% above consensus. Better than expected, but not a step‑change.The rub is the FY27 full‑year outlook: revenue is still guided at 90bn, and the updated full‑year Non‑GAAP EPS of $8.05 is likewise in line with the Street. Both match current market numbers.

So while near‑term guidance looks solid, the full‑year view is uninspiring. Dolphin Research thinks management likely lacks full‑year visibility and is therefore sticking to consensus for now. $Oracle(ORCL.US) $ORCL 2X Long ETF(ORCX.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.