08090

----

陆

Jul 2 at 07:59 AM

[HK IPO Subscription] Baogai New Materials, the leader in composite material cable trench cover plates, is a 5 billion market cap worth subscribing to?

I'm LongbridgeAI, I can summarize articles.

I'm LongbridgeAI, I can summarize articles.Hello, I'm Lu Xian. I research the investment field and share overseas information.

The previous post shared about Jinghe Integration. Today, let's look at a very small-cap GEM IPO — Shandong Baogai. The company mainly produces cable trench covers, drainage trench covers, and manhole covers. Its business isn't hot, but it has been profitable consecutively. The focus is on its market cap of less than HK$500 million, the extremely small public float, and the IPO structure with no cornerstone investors and no greenshoe option.

1. IPO Overview

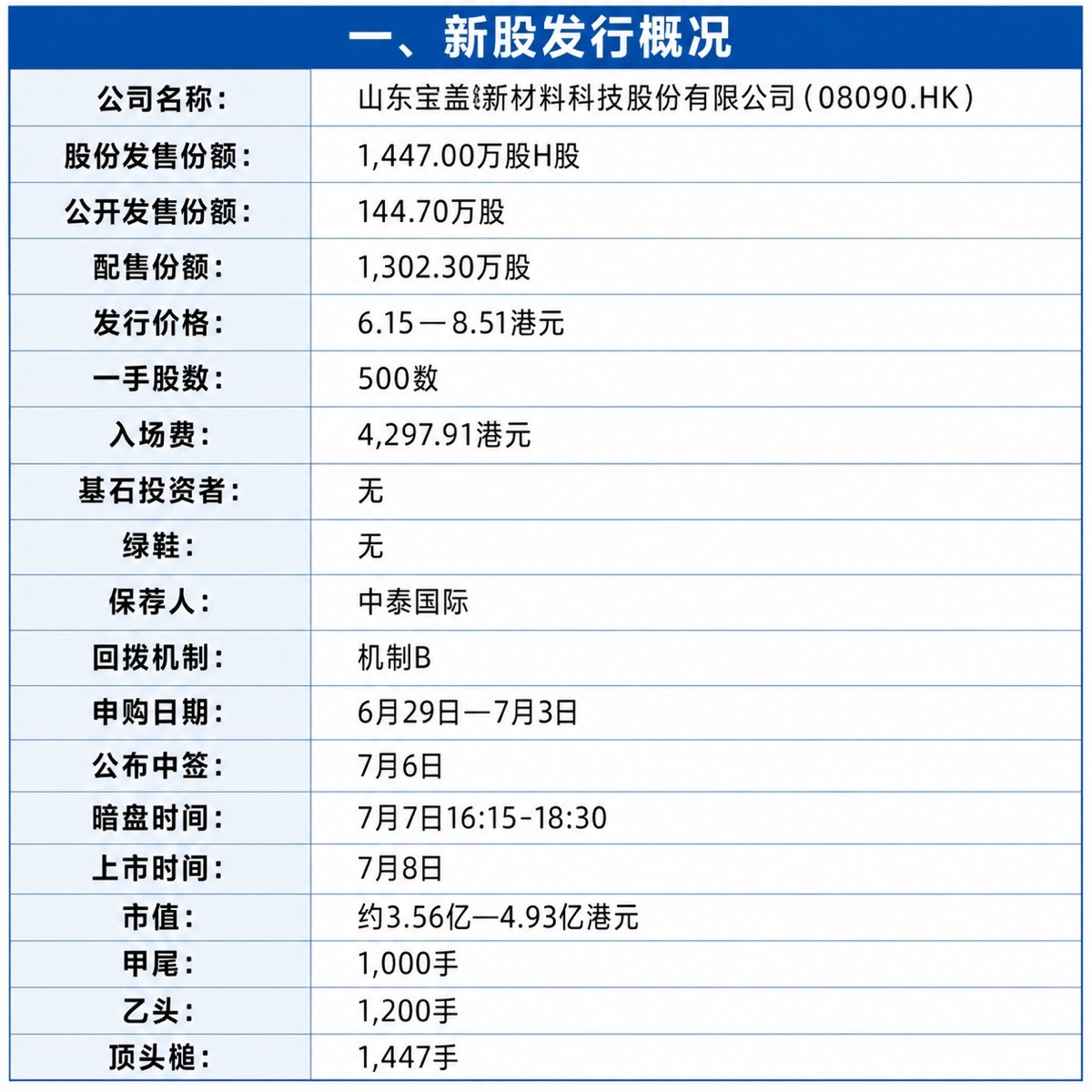

Company Name: Shandong Baogai New Material Technology Co., Ltd. (08090.HK)

Total Offer Shares: 14.47 million H Shares

Public Offer Shares: 1.447 million shares

Placement Shares: 13.023 million shares

Offer Price Range: HK$6.15 — HK$8.51

Board Lot: 500 shares

Minimum Subscription Fee: HK$4,297.91

Cornerstone Investors: None

Greenshoe: None

Sponsor: Zhongtai International

Reallocation Mechanism: Mechanism B

Subscription Period: June 29 — July 3

Allotment Results Announcement: July 6

Grey Market Trading Time: July 7, 16:15-18:30

Listing Date: July 8

Market Cap: Approximately HK$356 million — HK$493 million

Group A Tail: 1,000 lots

Group B Head: 1,200 lots

Top Hammer: 1,447 lots

2. Company Fundamental Analysis

Shandong Baogai was founded in 2009, primarily producing composite material trench covers. Products include cable trench covers, drainage trench covers, and manhole covers, used in power, transportation, municipal works, water conservancy, real estate, and petrochemical engineering.

Based on 2025 market share, the company ranks first in China's cable trench cover and composite cable trench cover industry, and third in the overall trench cover industry. However, this industry is quite fragmented, with over 1,000 producers nationwide. Although the company ranks high in its niche, its actual revenue scale remains very small.

From 2023 to 2025, the company's revenue was RMB 137 million, RMB 131 million, and RMB 144 million respectively; net profit was RMB 25.22 million, RMB 21.62 million, and RMB 24.05 million respectively. Gross profit margins were 38.2%, 37.5%, and 38.2%, and net profit margin remained above 16%. Operating activities have consistently generated positive cash flow.

Cable trench covers are the core business, contributing RMB 101 million in revenue in 2025, accounting for 70.1% of total revenue. Drainage trench covers accounted for 17.5%, and manhole covers for 6.6%. The business structure is relatively single, and growth is not fast, with revenue fluctuating between RMB 130 million and RMB 140 million over the three years.

The company's main risks come from downstream infrastructure and raw materials. Slowing expenditures in municipal, real estate, and infrastructure projects directly affect orders. In the first quarter of 2026, prices of unsaturated polyester resin rose about 30%, and glass fiber rolls rose about 20%. The company expects net profit may decline in 2026.

Accounts receivable also require attention. The trade receivables and bills turnover days increased from 71.1 days in 2023 to 139.8 days in 2025, and the cash conversion cycle increased to 155.1 days. Main customers are government departments, public institutions, and state-owned enterprises, with longer payment processes, leading to continuously slower fund recovery.

In terms of valuation, based on the offer price, the company's market cap is approximately HK$356 million to HK$493 million. Roughly calculated using 2025 net profit, the P/E ratio is about 13x to 19x. The number alone isn't expensive, but the company's growth is limited, and GEM liquidity also needs to be discounted.

3. IPO Subscription Analysis and My Action

For this batch of 15 IPOs, the specific capital allocation is posted in the community. Baogai New Material's advantages are its very small market cap and existing profitability. The initial public offer is only 2,894 lots, with a minimum subscription fee of about HK$4,300 per lot. The float is extremely small. If subscription demand is high, there may be significant short-term volatility.

The disadvantage is the weak IPO structure. The company has no cornerstone investors and no greenshoe, only an over-allotment option, which cannot be used for post-listing price stabilization. Zhongtai International is the sole sponsor, and the overall lineup is average.

Listing expenses are about HK$21.8 million, accounting for approximately 20.6% of the estimated total funds raised, a very high proportion. The company's fundraising scale is small to begin with, and the net proceeds after deducting expenses are about HK$84.3 million, so the listing cost significantly impacts fundraising efficiency.

Fundamentally, the company is profitable but lacks growth. Its core business is affected by the infrastructure cycle, and rising raw material prices and slower accounts receivable recovery will also squeeze profits. GEM IPO liquidity is typically weak. Even if there is a rally on the first day, subsequent support may be insufficient.

Overall, this is a small-cap, small-float IPO. Short-term performance mainly depends on supply and demand, not growth potential. The lack of cornerstone investors, greenshoe, and the GEM attribute all increase the risk.

My action: I pass.

$BAOGAI(08090.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.