IBM: This time, what's being sold isn't AI, it's a pickaxe.

I'm LongbridgeAI, I can summarize articles.

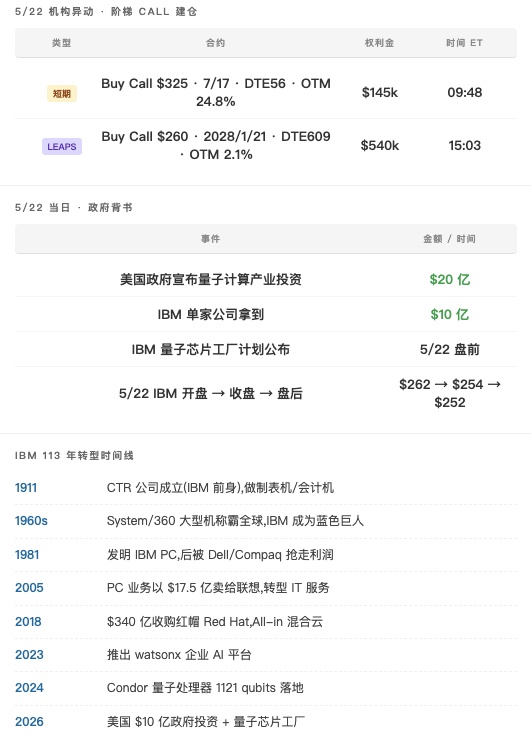

I'm LongbridgeAI, I can summarize articles.113-year-old $IBM(IBM.US), many people think it should have retired long ago. Last Friday, the US government announced a $20 billion investment in quantum computing, with IBM alone taking $10 billion. On the same day, the stock price opened high, up +3% to $262, then was hammered back to close at $254.

But the institutional fund flow that day was interesting: at 9:48 AM, they chased to buy short-term $325 OTM Calls betting on the quantum theme continuing, and at 3:03 PM, they turned around and bought LEAPS $260 long-term Calls, establishing positions until early 2028. This is opening both "short-term odds + long-term stock replacement" positions simultaneously, a structure you rarely see on a "traditional old-school" tech company.

Looking back a bit at IBM's past and present might help understand why institutions would bet this way.

When it was born in New York in 1911, IBM wasn't called IBM, it was CTR, with its main business being tabulating machines—doing census statistics for governments and banks, and payroll for accountants. This company survived the tabulator era, survived the 1960s dominance of the System/360 mainframe, survived the impact of the 1980s PC revolution (it invented the IBM PC, but Dell and Compaq took the profits, and in 2005 it simply sold its PC business to Lenovo), survived the 2000 internet bubble, and even survived the wave where cloud computing knocked down traditional hardware companies. Every time an industrial revolution came, IBM wasn't the coolest company, but it survived every time. And its secret is boring: don't participate in the gold rush, sell shovels to the gold rushers.

In this AI era, what IBM is doing still follows this old logic: OpenAI, Anthropic, Google, Meta are all competing in ChatGPT-style to C large models. IBM didn't fight for that, instead creating an enterprise-level AI deployment platform called watsonx, selling it to banks, hospitals, law firms, and government agencies. These clients simply won't use ChatGPT (data compliance requirements), but must adopt AI—so IBM became their "private AI transit hub." This is essentially the same thing as doing System/360 accounting work for banks in the 1960s.

More crucial are the quantum computing and hybrid cloud lines. On the quantum side, IBM actually has hardware—its IBM Quantum platform is already running on the 1121-qubit Condor processor, with a clear roadmap, almost the only company in the world selling quantum computers as commercial products. Google and IonQ are mostly still in the lab stage. On the hybrid cloud side, IBM's $34 billion acquisition of Red Hat in 2018 directly made it an unavoidable "transit layer" for AWS, Azure, and GCP—because large enterprises use multi-cloud, and everyone has to use Red Hat's OpenShift to manage it.

These two lines were officially endorsed by the US government with $1 billion last Friday. Simply put, the US doesn't want to be overtaken by China on the quantum computing track, so it chose a company with real hardware capabilities and poured national money into it. This isn't IBM telling its own story; it's the country selecting it as a core node for the domestic quantum industry.

Back to the institutional fund flow: the two Calls on 5/22 weren't betting on a single-day surge in the quantum sector, but two different bets. The short-term $325 Buy Call was betting "this wave of quantum theme from 5/22 continues until July," but the position was restrained at only $145k—this is the odds position. The LEAPS $260 Call bought in the afternoon is the real directional bet, $540k until early 2028, essentially using options to replace buying stock, using less capital but with higher leverage. Institutions are betting that all three lines—"2-year IBM quantum + hybrid cloud + enterprise AI"—will play out.

My judgment is: IBM's current role isn't an "AI concept stock," it's the "shovel-selling company in the AI/quantum era." Short-term stock price may fluctuate with quantum sector sentiment, but the 2-year LEAPS is betting on the national-level long-term theme of "US quantum industry localization," which is the institution's real stance. I don't think the short-term $325 odds position is worth chasing (quantum sector sentiment is too scattered), but the LEAPS line of thinking is valid—you don't necessarily have to copy the $260 strike price, but using the play of "3-5% position + long-term Call to replace stock" to follow the national-level theme.

Two upcoming time points worth watching: the June IBM Quantum Summit will likely announce more details on the Heron+ processor; the Q2 earnings report at the end of July will disclose Red Hat cloud growth—if both events are good, the LEAPS logic holds. If IBM falls below the $245 mid-term support level before the end of July, then be alert to the risk that "the quantum theme has already been priced in at once."

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.