$SpaceX(SPCX.US)SpaceX's first week as a public company was a big trap:

$SpaceX(SPCX.US)

This article from Seeking Alpha analyst James Foord makes a very straightforward judgment: SpaceX's IPO this time is a ticking time bomb dug for retail investors, don't touch it in the short term.

First, the lock-up structure. Traditional IPOs have all insiders unlock after 180 days, everyone competing together. But SpaceX played a new trick: 20% unlocks after the Q2 earnings report, then another 7% each at 70, 90, 105, and 120 days, another wave in Q3, with the bulk only after 180 days. Musk himself has to wait a year to sell, but others can start selling as early as 70 days. Right now, it's small supply against big demand, with retail investors and institutions that missed the boat scrambling, but in 6 to 12 months, it will reverse—those who wanted to buy have already bought, and those who want to sell start queuing up. This staged unlocking isn't to protect retail investors; it's dispersing selling pressure into chronic bleeding, dropping a little each time, making you think you can buy the dip when it's actually boiling the frog slowly.

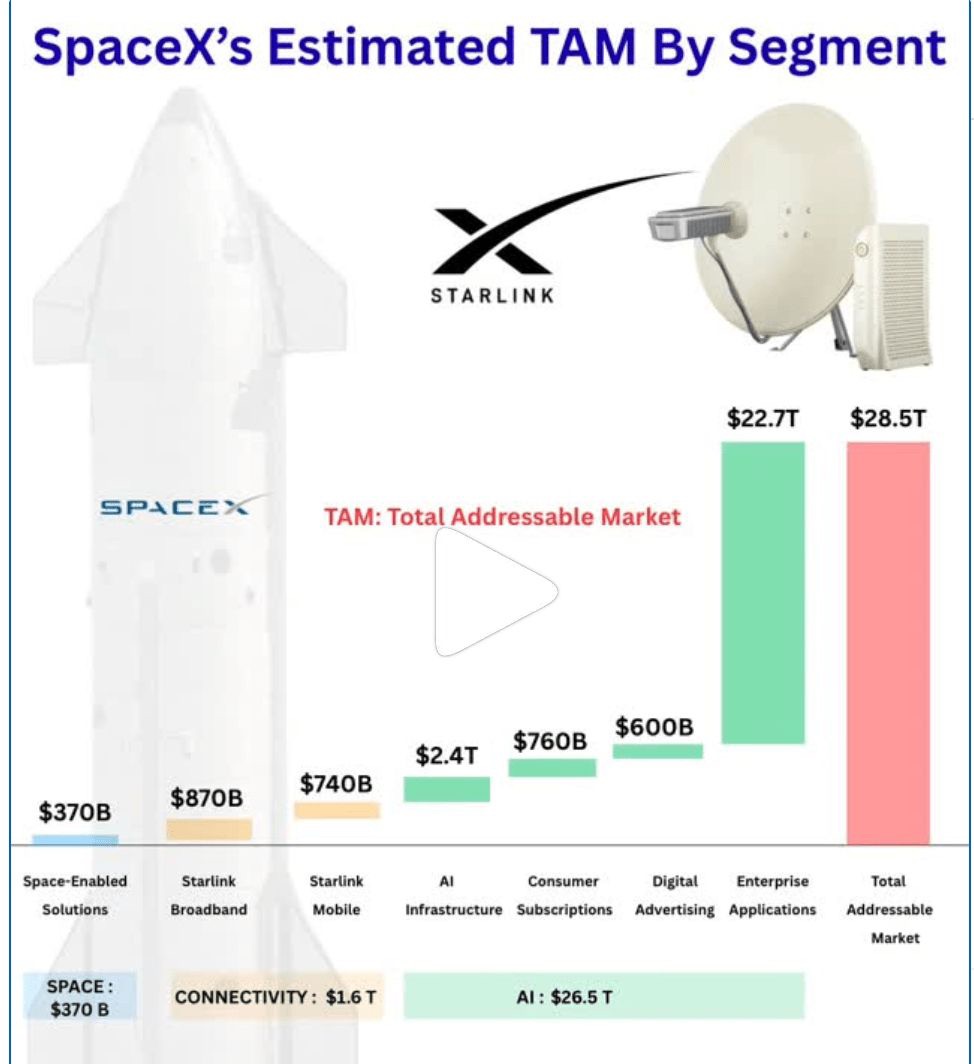

Then there's the AI pivot. SpaceX was originally a rocket and Starlink business, with technological moats but never profitable. Then last year, it acquired xAI, losing $2.47 billion in Q1, directly dragging the previously profitable SpaceX into the red. The TAM mentioned in the prospectus is $28.5 trillion, touted as the largest in human history, but 90% of that comes from AI. The problem is AI is the most crowded and cash-burning sector, and SpaceX has little competitive advantage here, having to go head-to-head with old players like Google and cloud giants. The author believes xAI is not a company that can dominate the market, and stuffing it into SpaceX will only muddy the financials further. Later, it acquired Cursor, which the author says precisely proves SpaceX lacks an edge in AI, having to buy to fill gaps.

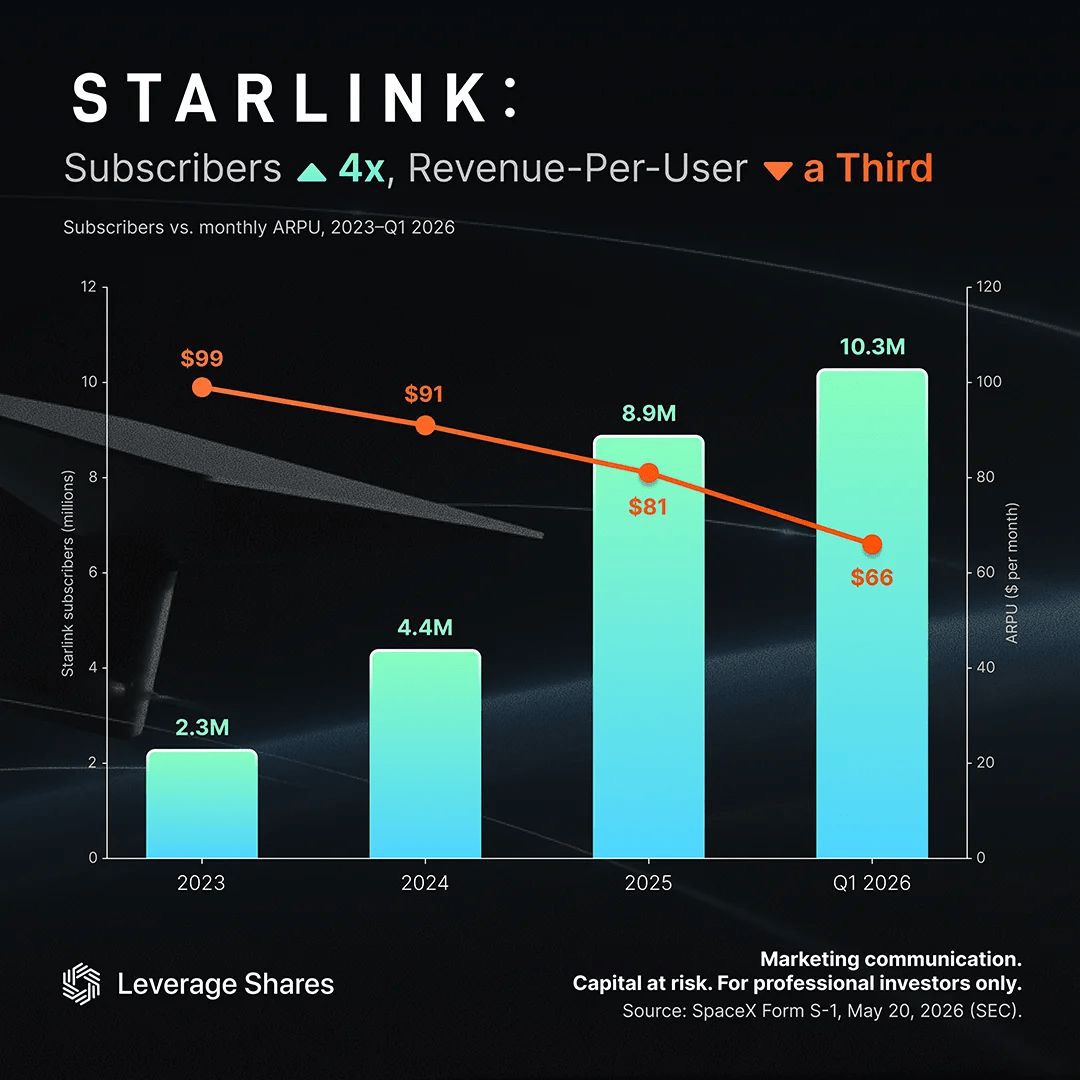

The valuation is even more outrageous. SpaceX's current P/E ratio is over 100x. Starlink had 10.3 million active users as of the end of March, which is growing, but ARPU is declining. The article mentions that the space industry is inherently a capital-intensive sector requiring government and public funding support, with profitability always an issue. SpaceX is already preparing to raise over $100 billion in the bond market, which makes the author even more bearish.

The author also mentions the bull case. SpaceX holds a 51% share of the commercial launch market, and reusable rocket technology does have a moat. Starlink accounts for 54% of the world's in-orbit satellites. If Starship can truly significantly reduce launch costs, it might open up new markets, like orbital computing, Mars transport, etc. While the AI layout lacks advantages, SpaceX has strong fundraising capabilities. If the money is used correctly, it could theoretically succeed.

But the author's conclusion is clear: these long-term stories are already priced in now, and there are too many factors unfavorable to retail investors in the short term. He won't touch it himself, but would consider buying if the price comes down in the future.

My personal view is similar. This IPO structure is cleverly designed to let early shareholders cash out in batches, stretching out the time for retail investors to take the bag. The AI pivot seems more like storytelling, with xAI's loss figure right there and the Cursor acquisition also showing they lack confidence in AI. A 100x PS valuation in the current market environment has a terrible risk-reward ratio unless you truly believe it can dominate AI. The rocket and Starlink businesses have value, but not at this price. Wait for the lock-up expiration pressure to release and for the valuation to return to a reasonable range.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.