Interpreting the Cash Flow Statement: Tracking the Movement of Funds

The cash flow statement is vital for assessing financial health. This article analyzes operating, investing, and financing cash flows to help you track funds, identify risks, and make stronger investment decisions.

Have you ever seen a company’s income statement show strong profits, yet later discover it faces cash flow problems or even ends up bankrupt? This scenario is not uncommon. The core issue is that the income statement reflects accounting profit, not actual cash movement. To truly understand a company’s financial health, you need to master the skills of analyzing the Cash Flow Statement. The Cash Flow Statement records all actual cash inflows and outflows over a specific period, helping investors track the movement of funds and identify potential financial risks. This article will guide you through the fundamental concepts of the Cash Flow Statement and teach you how to use this tool to make wiser investment decisions.

What is a Cash Flow Statement?

The Cash Flow Statement is one of the three principal financial statements, standing alongside the Income Statement and Balance Sheet as a critical document for evaluating a company’s financial condition. Unlike the Income Statement, which uses accrual accounting, the Cash Flow Statement uses a cash basis—recording only transactions involving actual cash.

Simply put, the Cash Flow Statement shows the changes in a company’s cash position over a defined period (typically a quarter or a year). It answers a key question: Where does the company’s cash come from, and where does it go?

Why is the Cash Flow Statement so Important?

The importance of the Cash Flow Statement lies in its ability to reveal a company’s actual financial position. Net profit on the Income Statement may include accounts receivable not yet collected or expenses not yet paid, but the Cash Flow Statement reflects true cash flow. Even if a company seems profitable on paper, if cash flow remains negative, it could quickly run into liquidity problems.

Important Note: The figures in the Cash Flow Statement are generally harder to manipulate, since only actual cash movements are recorded—making it a more reliable indicator of financial health.

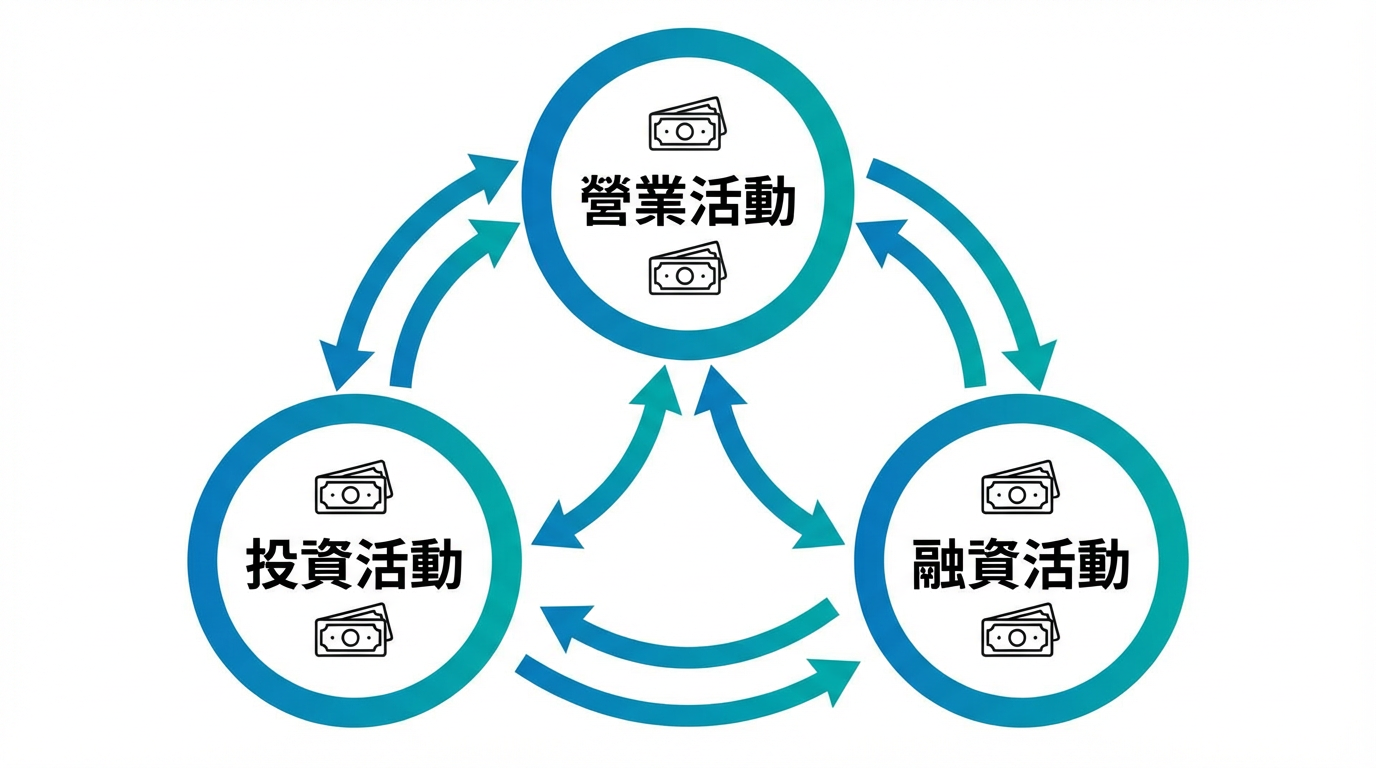

The Three Key Components of a Cash Flow Statement

The Cash Flow Statement consists of three main categories: cash flows from operating activities, investing activities, and financing activities. Together, these categories give a complete picture of enterprise cash movements.

Cash Flow from Operating Activities

Operating Cash Flow refers to cash flows generated from a company’s day-to-day business operations. This includes cash received from selling goods or services and payments for supplies, employee wages, rent, taxes, and other daily expenses.

Operating cash flow is a key measure of a company’s core business profitability. Ideally, this figure should be positive, meaning the company generates enough cash from its main business to support operations and repay debt. If operating cash flow is negative for an extended period—even if the income statement shows a profit—the company may still face liquidity risks.

Key items under operating activities include:

- Cash received from sales of goods or services

- Payments to suppliers

- Employee wages

- Operating expenses (rent, utilities, etc.)

- Taxes paid

- Interest received or paid

Cash Flow from Investing Activities

Investing Cash Flow captures investments and disposals involving long-term assets, such as purchasing or selling property, equipment, land, or making equity investments in other companies.

Investment cash flow is usually negative, which isn’t a bad thing—it typically indicates the company is expanding its operations and investing for growth. However, if investing cash flow suddenly turns positive, it might suggest the company is selling off assets to generate cash, warranting further investigation into its financial condition.

Main items under investing activities include:

- Purchase of fixed assets (property, equipment, land, etc.)

- Sale of fixed assets

- Purchase of equity or bonds in other companies

- Sale of investments

- Investment income received (dividends, interest)

Cash Flow from Financing Activities

Financing Cash Flow reflects how a company raises capital and returns funds to shareholders or repays debt. This covers activities like issuing shares, obtaining loans, repaying borrowings, and paying dividends.

A positive financing cash flow suggests the company is raising funds via loans or equity; a negative figure indicates repayments of debt or distributions to shareholders (dividends, share buybacks). Financially healthy companies generally support investment needs from operating cash flow, thus lessening dependency on external funding.

Main items under financing activities include:

- Issuing shares to raise capital

- Bank loans

- Loan principal repayments

- Dividends paid to shareholders

- Share buybacks

- Payment of financing expenses (interest, fees, etc.)

How to Interpret the Cash Flow Statement

When interpreting a Cash Flow Statement, the focus should be on the direction of cash flows, not just the absolute numbers. Misallocation of cash can be more harmful than low cash flow. Here are key principles to follow:

Interpreting Operating Cash Flow

Operating cash flow should usually be positive, and not deviate too far from net profit. If operating cash flow is negative for a long time, it may indicate:

- Difficulty collecting accounts receivable

- Excess inventory accumulation

- Weak core business profitability

Short-term negative operating cash flow isn’t always bad—for example, fast-growing companies might invest heavily in inventory or production expansion, temporarily creating negative figures. The key is to observe the trend; multiple consecutive quarters of negative figures should raise caution.

Investment Tip: If operating cash flow and net profit show a large gap, investigate further. Ideally, operating cash flow should be close to or higher than net profit, indicating that profits are translating into real cash inflow.

Interpreting Investing Cash Flow

Negative investing cash flow usually means the company is investing in its future, such as buying new equipment or expanding production—this is a positive sign for growth companies. However, if the negative figure is large and persistent, it may imply excessive capital expenditure, so pay attention to the return on investment.

If investing cash flow suddenly turns positive—especially by a large amount—it could mean the company is liquidating assets to replenish cash, which is often a warning signal. Investors should seek to understand the reasons behind these asset sales and whether the company is facing funding pressure.

Interpreting Financing Cash Flow

A positive financing cash flow shows the company is raising capital, either through loans or issuing shares. By itself, this is not bad, but it must be examined alongside operating cash flow:

- If operating cash flow is healthy and positive, fundraising could be to seize growth opportunities.

- If operating cash flow is negative, fundraising might be patching operational shortfalls—this is a warning sign.

A negative financing cash flow suggests the company is repaying debt or returning capital to shareholders. This is usually a sign of financial health, reflecting that the business has enough cash to support operations, repay debts, or buy back shares.

Key Metrics in the Cash Flow Statement

In addition to the three main types of cash flow, several derived indicators can help investors better assess a company’s financial standing.

Free Cash Flow

Free Cash Flow (FCF) is a critical metric for investors, calculated as:

Free Cash Flow = Operating Cash Flow + Investing Cash Flow

Or more precisely:

Free Cash Flow = Operating Cash Flow – Capital Expenditure

Free cash flow represents the cash remaining after maintaining or expanding operations, and is available for discretionary use. A positive FCF means the company has ample cash to repay debt, pay dividends, or make acquisitions; a negative FCF may suggest dependence on external financing.

Analysis Point: Consistently positive and growing free cash flow is characteristic of financially strong companies, which typically also show robust profitability and efficient capital use.

Net Cash Flow

Net Cash Flow is the sum of all three types of activity, reflecting the net change in cash and cash equivalents for the period.

Net Cash Flow = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow

A positive net cash flow indicates an increase in cash holdings; a negative one means a decrease. However, just looking at the net figure can be misleading—the details of each activity must be considered to accurately gauge financial health.

Cash Flow Ratios

Cash flow ratios help investors evaluate a company’s debt service capacity and financial flexibility. Common ratios include:

Operating Cash Flow to Debt Ratio = Operating Cash Flow ÷ Total Debt

This measures a company’s ability to service its debt with operating cash. A higher ratio means stronger debt service capability; generally, a ratio above 20% is considered sound.

Cash Reinvestment Ratio = (Operating Cash Flow – Dividends) ÷ (Fixed Assets + Long-term Investments + Other Assets + Working Capital)

This shows the company’s ability to reinvest cash into its business, which reflects its growth potential.

Common Pitfalls in the Cash Flow Statement

Although it is relatively difficult to manipulate a Cash Flow Statement, some companies may still use accounting tactics to embellish cash flow. Investors should watch for the following:

Delaying Payments to Suppliers

A company may postpone payments to suppliers to temporarily improve operating cash flow. While this can boost figures in the short term, over time it may harm supplier relationships and even disrupt supply chain stability.

Investors can identify this by watching for a sudden increase in accounts payable turnover days. If payable days spike rapidly along with improved operating cash flow, be cautious.

Accelerating Accounts Receivable Collection

A company might offer discounts or use factoring to speed up cash collection, temporarily increasing operating cash flow. This can sacrifice profit margin and isn’t generally sustainable.

Reducing Inventory Investment

Cutting back on stock purchases can temporarily improve cash flow, but if inventory levels drop too low, future sales capacity could suffer. Investors should look at inventory turnover in conjunction with sales growth trends.

Warning: If operating cash flow improves suddenly but net profit does not rise or even declines, it may signal the company is manipulating cash flow through accounting maneuvers.

How to Use the Cash Flow Statement in Investment Decisions

The Cash Flow Statement is a vital tool for investors in evaluating corporate health and investment value. Here are some practical strategies:

Seek Companies with Robust Cash Flow

Investors should target companies whose operating cash flows are stable, positive, and growing. Such companies generally have:

- Strong core business profitability

- Effective accounts receivable management

- Efficient capital utilization

These firms can fund expansion and deliver shareholder returns without constantly relying on external financing.

Assess Growth Potential

Reviewing a company’s investing cash flow and capital expenditure helps gauge its ambition and execution in pursuing growth. Growth companies often have higher capex, investing in new equipment, markets, or technology.

However, investors should also monitor investment returns—if the company keeps investing heavily without a corresponding rise in operating cash flow, efficiency may be lacking.

Identify Early Warning Signs of Financial Distress

The Cash Flow Statement helps investors spot trouble early:

- Persistent negative operating cash flow

- Long-term negative free cash flow

- Prolonged large positive financing cash flow (indicating continual fundraising to cover cash gaps)

These signals often appear before losses show up on the Income Statement, letting investors act before it is too late.

Analyze in Tandem With Other Financial Statements

Don’t look at the Cash Flow Statement in isolation—use it with the Income Statement and Balance Sheet:

- Compare the Income Statement and Cash Flow Statement: Assess quality of earnings. If net profit is high but operating cash flow is low, receivable collection or profit quality may be an issue.

- Compare the Balance Sheet and Cash Flow Statement: Evaluate financial structure and liquidity. Monitor changes in cash/equivalents alongside debt levels for a more complete picture.

How Longbridge Securities Helps You Track Cash Flow

As a new-generation digital brokerage, Longbridge Securities provides global stock trading and investment services, including the Hong Kong and US markets. The platform integrates comprehensive financial data and analysis tools to help investors monitor company cash flow statements and other critical financial indicators.

Longbridge Securities offers instant financial data so investors can:

- Quickly view company cash flow statements and all three major financial reports

- Compare the cash flow of different companies

In addition, Longbridge’s AI assistant PortAI is capable of analyzing corporate financial data and providing personalized investment insights, helping investors access more information efficiently.

Frequently Asked Questions

What is the difference between the Cash Flow Statement and the Income Statement?

The Cash Flow Statement uses a cash basis and records only cash transactions; the Income Statement uses an accrual basis, recording revenue and expenses that may not have resulted in cash movement yet. Thus, a company may appear profitable on the Income Statement but may not actually have cash on hand. The Cash Flow Statement offers a more accurate picture of true financial health.

Is negative operating cash flow always bad?

Not necessarily. Short-term negative operating cash flow can result from rapid expansion, heavy inventory investment, or seasonal behavior. However, if operating cash flow is negative for several consecutive quarters, watch out for underlying issues such as poor core profitability or trouble collecting receivables.

What is free cash flow and why is it important?

Free cash flow is what’s left after subtracting capital expenditures from operating cash flow. It represents the cash available to a company after sustaining or expanding operations. A positive and steadily increasing free cash flow signals strong profitability and financial flexibility, making it a key metric for evaluating investment value.

How do you judge whether a company’s cash flow is healthy?

Healthy cash flow is generally characterized by: consistently positive and growing operating cash flow; positive free cash flow; a small gap between operating cash flow and net profit; and no persistent large reliance on external financing (financing cash flow should not be long-term positive and substantial). Investors should also focus on trends, not just single-quarter data.

Is positive investing cash flow good or bad?

It depends on the context. Positive investing cash flow generally means the company is selling assets, perhaps optimizing asset allocation or facing funding pressure. Investors should understand the reasons and background for such sales. On the other hand, negative investing cash flow means the company is investing for the future (buying equipment, expanding operations)—a positive sign for a growth company.

How can you spot faked cash flow?

Although cash flow statements are harder to distort, be on guard for: a sudden jump in operating cash flow without profit growth; a sharp increase in accounts payable turnover days; a steep drop in accounts receivable days; or an abnormal fall in inventory levels. These may indicate working capital manipulation to embellish cash flow numbers.

Conclusion

The Cash Flow Statement is an essential tool for evaluating a company’s financial health, revealing the real movement of funds and helping you spot potential risks and promising investment targets. By thoroughly understanding operating, investing, and financing cash flows, you can better gauge a company’s earnings quality, growth prospects, and financial strength.

Remember: The key to interpreting the Cash Flow Statement lies in following the direction of funds, not just the size of the numbers. Even if a company looks profitable on paper, persistent negative cash flow can lead to liquidity problems. Conversely, companies with healthy cash flow can maintain competitiveness over the long term, even if short-term profits fluctuate.

Before making investment decisions, be sure to fully understand the workings, risk profile, and trading rules of each investment tool and build a sound risk management plan. You can learn more via the Longbridge Academy or by downloading the Longbridge App.