Filing Taxes on U.S. Stock Investments: The Complete Guide to Form 1042-S

Confused by the Form 1042-S your broker sends each year? This article gives Hong Kong investors a clear guide to each field, dividend withholding tax mechanics, and key filing considerations.

TL;DR: Form 1042-S is a tax document that U.S. brokers issue each year to non-U.S. residents (including Hong Kong investors). It records U.S.-source income such as dividends and the taxes already withheld. After receiving Form 1042-S, Hong Kong investors generally do not need to file anything separately with the U.S. Internal Revenue Service (IRS) or Hong Kong’s Inland Revenue Department, because the broker has already withheld the tax before the dividend is credited.

Hong Kong investors who trade U.S. stocks may receive a Form 1042-S at the beginning of each year, either mailed by the broker or available for download on the platform. Many investors feel puzzled when they see this document for the first time: What is it? What should I do with it? Do I need to file anything?

Form 1042-S is a tax form in the U.S. tax reporting system specifically for non-U.S. residents. Its official name is “Foreign Person's U.S. Source Income Subject to Withholding.” For Hong Kong investors, understanding this form is not only part of understanding investment costs, but also helps evaluate the overall return of U.S. dividend investing.

Below, from the perspective of Hong Kong investors, we break down the structure of Form 1042-S, explain what each box means, and describe the withholding mechanisms for different types of income.

What is Form 1042-S, and why do Hong Kong investors receive it?

Form 1042-S is completed and issued by the broker that holds your U.S. stock account (i.e., the “withholding agent”). It records certain income you received from the United States in the prior tax year, as well as the amount of tax the broker withheld on behalf of the U.S. Internal Revenue Service (IRS).

Under U.S. tax law, certain types of investment income earned in the United States by non-U.S. residents (non-resident aliens, or “NRAs”) must be withheld at the time of payment. By March 15 each year, brokers must provide Form 1042-S to each non-U.S. resident investor as the official tax record.

Who is considered a “non-resident alien”?

People who hold Hong Kong status and invest in U.S. stocks through Hong Kong or overseas brokers are generally treated as non-resident aliens under U.S. tax law. The W-8BEN (Certificate of Foreign Status) you complete when opening the account is used to confirm this status. A W-8BEN is typically valid from the year it is signed through the end of the third subsequent calendar year; the broker will remind you to renew it before it expires.

If you have properly submitted a W-8BEN, the broker will withhold dividend tax at the applicable rate (typically 30%) and issue Form 1042-S at year-end to record it. If you have not submitted a W-8BEN, the broker may apply backup withholding—currently 24%—to more types of income (including gross proceeds from selling stocks), making the situation more complex.

If you want to learn about opening a U.S. stock account and how to complete the W-8BEN, please refer to the U.S. stock account opening and beginner’s guide.

A full picture of U.S. stock taxes for Hong Kong investors

Before interpreting Form 1042-S, it helps to understand the main taxes involved when Hong Kong investors invest in U.S. stocks, which in turn clarifies what the form means.

Capital gains tax: Exempt for Hong Kong investors

Profits from buying and selling U.S. stocks (capital gains) are generally exempt from U.S. federal tax for non-resident aliens. This means that, at the U.S. level, you do not need to pay tax on trading gains when you sell U.S. stocks. This is also why Form 1042-S does not cover capital gains—exempt income does not need withholding or reporting.

Dividend income: 30% withholding tax

Dividends received from U.S.-listed companies (including common stocks and some ETFs) are typically subject to 30% withholding for non-resident aliens. This tax is withheld by the broker before the dividend is credited, so the dividend you receive is the net amount after tax.

The core function of Form 1042-S is to record these dividend amounts and the corresponding 30% withholding.

Note: There is no comprehensive personal income tax treaty between Hong Kong and the United States. As a result, most Hong Kong investors cannot use a tax treaty to apply for a reduced dividend tax rate (the standard 30% withholding rate can only be reduced if an applicable treaty exists). Some investors enter treaty provisions on Form W-8BEN, but whether they apply depends on individual circumstances—consult a professional tax advisor for your specific situation.

Estate tax: A risk that should not be overlooked

The U.S. levies estate tax on U.S. assets (including U.S. stocks) held in the estates of non-residents. The exemption is only USD 60,000, and amounts above that may be taxed at higher rates. This is a tax risk worth noting for long-term U.S. stock investing, but estate tax is outside the scope of Form 1042-S.

Hong Kong local taxation: No filing required

Under Hong Kong’s “territorial source principle,” only income arising in or derived from Hong Kong is taxable. Dividends and capital gains from investing in U.S. stocks are offshore income and do not need to be reported to or taxed by Hong Kong’s Inland Revenue Department.

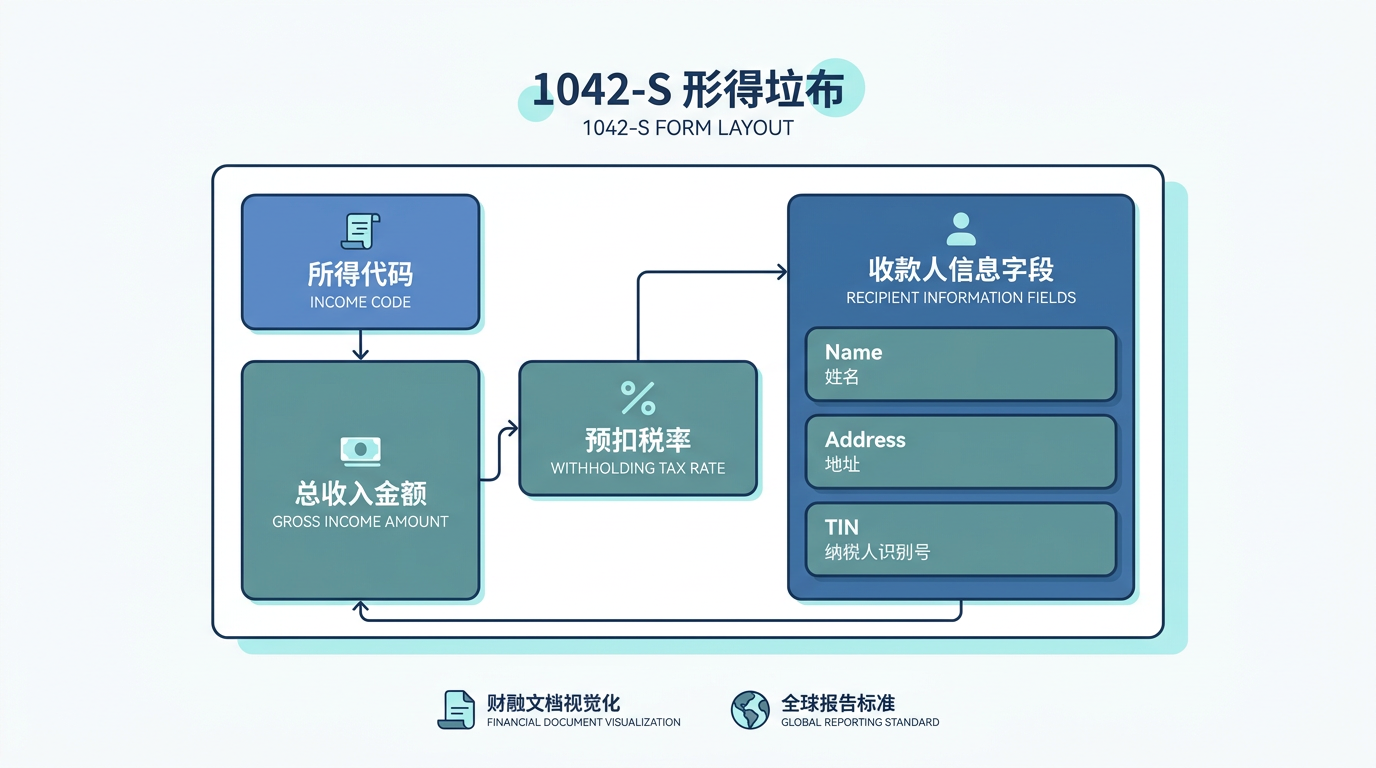

A box-by-box guide to Form 1042-S

With the tax background in mind, we can break down the main boxes on Form 1042-S.

Box 1: Income Code

The income code is a two-digit number used to identify the type of income. For U.S. stock investors, the most common codes include:

- Code 06: Dividends paid by U.S. corporations — most common when holding individual U.S. stocks

- Code 01: U.S.-source interest (Interest paid by U.S. obligor) — e.g., interest earned on cash balances in the account

- Code 37: Return of Capital — may appear in distributions from some ETFs

Tip: If Box 1 is blank or shows “00,” it indicates the form was completed incorrectly. You should contact your broker to request a correction; otherwise, your tax record may be incomplete.

Box 2: Gross Income

This is the total amount of income paid to you by the broker (before tax), in U.S. dollars. For example, if a quarterly dividend is USD 100, Box 2 will show 100.

This is the original record of your dividend income and helps you verify whether the year’s dividends match your broker’s monthly statements.

Box 3a / Box 3b: Chapter 3 exemption code and rate

Box 3a shows the applicable exemption code (if any), and Box 3b shows the actual withholding rate as a percentage. For most Hong Kong investors, Box 3b typically shows “30.00,” meaning the standard 30% withholding rate applies.

Box 4a / Box 4b: Chapter 4 (FATCA) exemption code and rate

These boxes relate to the reporting requirements under the U.S. Foreign Account Tax Compliance Act (FATCA). For most individual investors, they typically do not create any additional tax impact.

Box 7 to Box 11: Various withholding amounts

These boxes record amounts such as U.S. federal withholding (Federal Tax Withheld). The most important is Box 7 (Federal Tax Withheld), which shows the total tax withheld by the broker and remitted to the IRS. For a USD 100 dividend at a 30% rate, Box 7 should show 30.

Box 12 to Box 13: Withholding agent and recipient information

Box 12 includes the broker’s name, address, and Employer Identification Number (EIN). Box 13 records your (the recipient’s) personal details, including your name, address, and Taxpayer Identification Number (TIN, if any).

If any details in Box 13 are incorrect, contact your broker immediately to correct them to ensure accurate tax records.

Why might you receive multiple Forms 1042-S?

Many investors find that they receive multiple Forms 1042-S from the same broker for the same tax year. This is normal. Each Form 1042-S corresponds to one type of income (income code). For example, if you hold both individual U.S. stocks (Code 06 dividends) and a money market fund (Code 01 interest), you may receive two separate Forms 1042-S.

Each form should be kept, because together they make up your complete U.S. tax record.

How to download and reconcile Form 1042-S

Most U.S. brokers provide Form 1042-S electronically by March 15 each year (or the next business day if March 15 falls on a holiday). Based on publicly available information, the general steps are as follows:

Download steps (using a typical U.S. broker as an example)

Interfaces differ by broker, but you can usually find the Form 1042-S PDF under “Tax Documents” or “Statements & Documents” in your account. After downloading, it is recommended that you archive the document for your records.

What to check

After receiving Form 1042-S, it is recommended that you reconcile it against your monthly statements or transaction records, focusing on:

- Whether Box 2 (Gross Income) matches your total annual dividend distributions

- Whether Box 7 (Federal Tax Withheld) is approximately 30% of Box 2

- Whether your personal information in Box 13 is accurate

- Whether the income code matches the actual income type

If you find a material discrepancy, contact your broker as early as possible, because there are time limits for issuing a Corrected 1042-S.

After receiving Form 1042-S, what actions should Hong Kong investors take?

For most Hong Kong individual investors, after receiving Form 1042-S, you do not need to file any tax return with the IRS, nor do you need to file anything with Hong Kong’s Inland Revenue Department, because:

- Capital gains are exempt from U.S. tax

- Dividend tax is withheld at source by the broker

- Hong Kong does not tax offshore income

The main purpose of Form 1042-S is to serve as your tax record, confirming that the tax was withheld as required. It is recommended that you keep the form and the relevant monthly statements each year for future reference.

Tip: If your investment situation is more complex—for example, involving multiple account types, private funds, or trust investments—it is recommended that you consult a professional tax advisor with U.S. tax expertise to ensure your situation is handled properly.

For U.S. dividend investing strategies, please refer to related materials. When evaluating dividend-investing returns, you can include the impact of withholding tax in your calculations.

Frequently Asked Questions

What is the relationship between Form 1042-S and Form W-8BEN?

W-8BEN is the document you provide to your broker to declare that you are a non-U.S. resident, enabling the broker to confirm the applicable tax rate and treatment. Form 1042-S is the annual tax reporting form issued by the broker after year-end, recording actual income and withholding. They are complementary: W-8BEN establishes your status; 1042-S records the year’s tax outcome.

Do Hong Kong investors need to apply for a refund from the IRS?

In general, dividend withholding on U.S. stocks for Hong Kong individual investors is a final tax. There is no need—and typically no ability—to request a refund from the IRS for the 30% dividend withholding already withheld. Refund claims (via Form 1040NR) mainly apply in cases where treaty benefits were available but too much tax was withheld, or where tax was withheld in error on certain income. If in doubt, consult a tax professional.

If I had no dividend income, will I receive Form 1042-S?

If, during the entire tax year, you did not receive any U.S.-source income subject to withholding (for example, you only traded and did not hold positions through dividend dates), you generally will not receive Form 1042-S. Form 1042-S is issued only when there is income to report.

Will holding U.S.-listed ETFs also result in Form 1042-S?

Yes. If you hold U.S.-listed ETFs and receive distributions, you may also receive Form 1042-S. ETF distributions may include different types of income (such as dividends, interest, and return of capital), and the form will show the corresponding income codes. Some income types (such as return of capital, Code 37) may be subject to different rates or even be tax-exempt; the exact treatment depends on the ETF’s actual distribution composition.

Do the amounts on Form 1042-S need to be converted into HKD for reporting?

Because Hong Kong does not tax offshore income from U.S. stocks, you do not need to convert the U.S. dollar amounts on Form 1042-S into Hong Kong dollars for reporting to the Inland Revenue Department. Simply keep Form 1042-S as part of your personal financial records.

Conclusion

Form 1042-S may look complicated, but for Hong Kong investors, understanding its core function is not difficult: it is the U.S. tax record your broker provides each year, confirming that withholding tax on dividends and other income has been properly handled. In most cases, you do not need to take any additional filing action.

Understanding Form 1042-S helps you more clearly evaluate the actual net return of U.S. dividend investing, and incorporate tax factors into portfolio planning. Investment decisions involve your personal financial situation, risk tolerance, and market judgment; it is recommended that you make decisions only after fully understanding all relevant factors.

Which tools you choose depends on your investment objectives, risk tolerance, market outlook, and experience level. No matter which investment instruments you choose, you must fully understand how they work, their risk characteristics, and trading rules, and establish a sound risk management plan. You can learn more investment knowledge through Longbridge Academy or download the Longbridge App.