ETF vs Mutual Fund: Key Differences Singapore Investors Should Understand

Understanding the differences between ETFs and mutual funds is essentialfor Singapore investors looking to diversify overseas. Learn about costs, tradingflexibility, and which option suits your goals.

TL;DR: Exchange-Traded Funds (ETFs) and mutual funds both offer portfolio diversification, but they differ significantly in trading flexibility, cost structure, and tax efficiency. ETFs trade like stocks throughout the day with generally lower fees, while mutual funds execute once daily at Net Asset Value (NAV) and may offer active management. Singapore investors should consider expense ratios, withholding taxes, and their investment timeline when choosing between these vehicles.

When Singapore investors look to diversify their portfolios beyond local markets, they encounter two primary investment vehicles: ETFs and mutual funds. Both offer access to overseas markets and built-in diversification, but understanding their differences can help investors evaluate these investment vehicles.

This guide breaks down the key differences between ETFs and mutual funds, helping you understand which option aligns with your investment objectives, risk tolerance, and trading preferences.

What Are ETFs and Mutual Funds?

Both ETFs and mutual funds are pooled investment vehicles that hold collections of stocks, bonds, or other securities. They provide individual investors access to diversified portfolios that would be difficult or expensive to replicate independently.

An Exchange-Traded Fund is an investment fund that trades on stock exchanges, similar to individual stocks. ETFs typically track specific market indices, sectors, or asset classes. According to research from Vanguard, ETFs can be purchased for the price of a single share. When you buy an ETF, you're purchasing a proportional stake in a basket of underlying securities.

Mutual funds are investment vehicles managed by professional fund managers who pool money from multiple investors. Unlike ETFs, mutual funds do not trade on exchanges. Investors buy or redeem shares directly from the fund company at the Net Asset Value calculated at the end of each trading day.

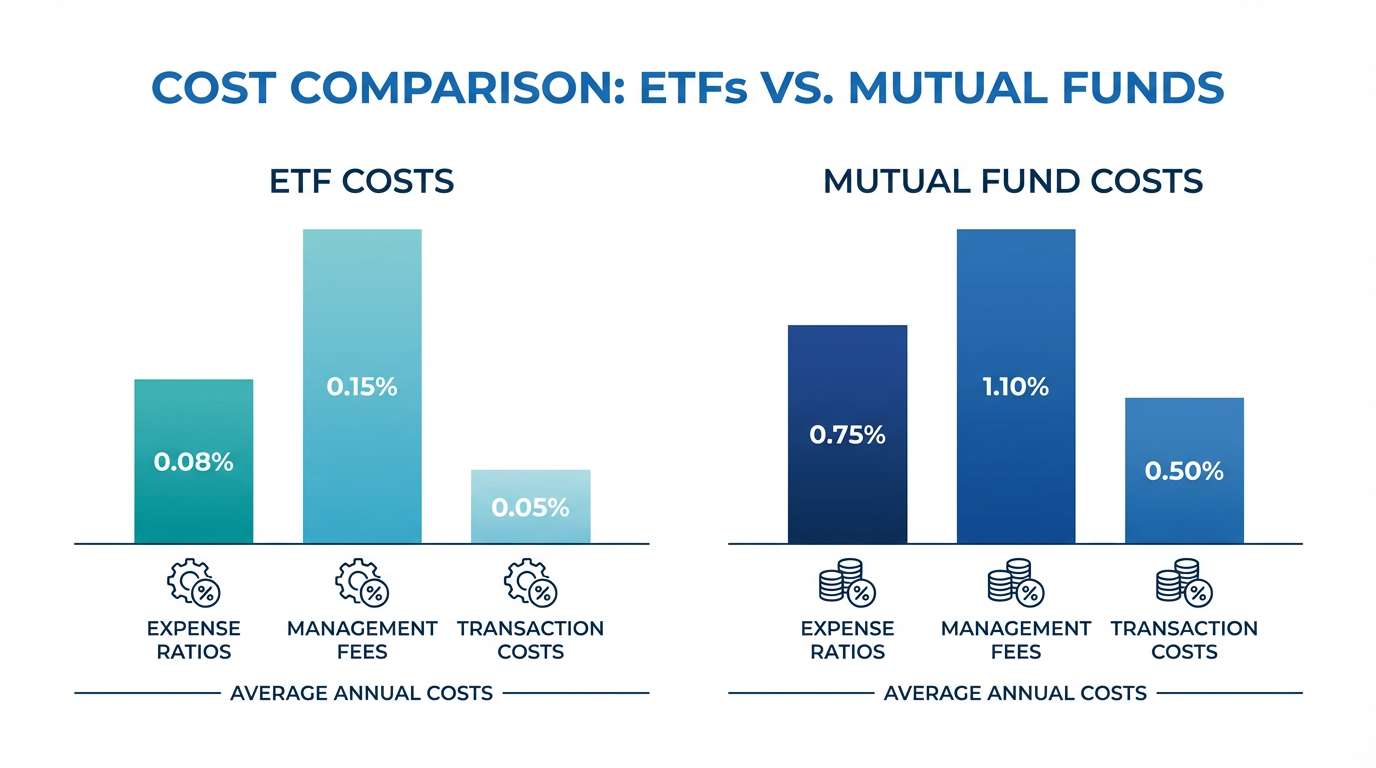

Cost Structure: Where Your Money Goes

Understanding the fee structure of each investment vehicle is essential for Singapore investors, as costs directly impact long-term returns.

Expense Ratios and Management Fees

ETFs generally carry lower expense ratios than mutual funds. Passively managed ETFs can have expense ratios as low as 0.03%, meaning investors pay just USD 0.30 annually for every USD 1,000 invested. In contrast, actively managed mutual funds typically charge expense ratios ranging from 1% to 2% per year.

This difference stems from the management approach. ETFs predominantly use passive index-tracking strategies requiring minimal ongoing management, while actively managed mutual funds employ teams of analysts and portfolio managers.

Transaction Costs

When trading ETFs, investors may incur brokerage commissions similar to stock trades. However, many brokers now offer commission-free ETF trading. ETFs also have bid-ask spreads, which represent the difference between the buying and selling price.

Mutual funds often charge sales loads, which are fees paid when buying or selling fund shares. Front-end loads are charged when purchasing shares, while back-end loads apply when redeeming shares. However, many mutual funds now offer no-load options that eliminate these sales charges.

Tip: For cost-conscious investors, comparing the total cost of ownership (including expense ratios, transaction fees, and potential sales loads) provides a clearer picture of true investment costs over time.

Trading Access and Execution

The way you buy and sell ETFs versus mutual funds differs fundamentally, affecting your flexibility and control over investment timing.

ETFs trade on stock exchanges throughout market hours, allowing investors to buy or sell shares at real-time market prices. This intraday trading capability provides several advantages: execute trades at specific price points using limit orders, respond quickly to market movements, implement trading strategies like stop-loss orders, and access real-time pricing information.

Singapore investors can access ETFs listed on local exchanges like SGX (Singapore Exchange), as well as international ETFs through overseas markets. Platforms that offer comprehensive market access enable investors to track real-time market performance across different exchanges.

Mutual funds operate differently. All buy and sell orders placed during a trading day execute at the same NAV price calculated after the market closes. All investors who place orders on the same day receive the same price, with no ability to time trades during market hours. This structure suits investors who prefer a consistent pricing mechanism and don't require trading flexibility. The investment products available through Longbridge include both ETFs and mutual funds.

Management Approach: Passive vs Active

The investment strategy employed by ETFs and mutual funds significantly impacts potential returns, risk levels, and costs.

Most ETFs use passive management strategies, tracking specific market indices like the S&P 500 or MSCI World. This approach offers lower management fees, transparent holdings, predictable performance relative to the benchmark, and reduced portfolio turnover.

Many mutual funds employ active management strategies where professional fund managers analyze securities and adjust portfolio allocations based on research and market outlook. Active management aims to outperform benchmark indices through strategic security selection. However, it involves higher fees to compensate portfolio managers and research teams.

Tip: Consider your investment philosophy when choosing between passive and active approaches. Passive strategies work well for investors who believe in market efficiency and want low-cost diversification, while active management may appeal to those seeking professional expertise.

Tax Efficiency for Singapore Investors

Tax implications can significantly affect investment returns, particularly for Singapore investors accessing overseas markets.

ETFs are generally considered more tax-efficient than mutual funds due to lower portfolio turnover, in-kind creation and redemption mechanisms that minimize taxable events, and investor control over when they realize capital gains.

However, Singapore investors should be aware of withholding taxes on overseas investments. For US-listed ETFs, a 30% withholding tax applies to dividends received by Singapore residents. For Irish-domiciled UCITS ETFs (Undertakings for Collective Investment in Transferable Securities), the withholding tax on US dividends is typically 15%, offering better tax efficiency.

Mutual funds may generate more taxable events due to higher portfolio turnover, capital gains distributions passed to shareholders, and fund rebalancing activities.

Singapore does not impose capital gains tax on investment profits, which benefits both vehicles. However, dividend income from overseas investments remains subject to foreign withholding taxes based on fund domicile.

Minimum Investment and Automation

Access barriers differ between ETFs and mutual funds, affecting which investors can participate in each vehicle.

ETFs require only the price of a single share as the minimum investment, ranging from a few dollars to several hundred dollars. This low entry point makes ETFs accessible to investors with limited capital.

Mutual funds traditionally impose minimum initial investment requirements, often ranging from USD 1,000 to USD 3,000 or more. According to Vanguard, their mutual funds typically require minimum investments around USD 3,000, though some mutual funds require minimum initial investments, which may range from approximately USD 1,000 to USD 3,000 depending on the fund provider.

Mutual funds excel in supporting automatic investment plans with dollar-cost averaging strategies. Traditional ETF investing presents challenges for automatic contributions because ETFs trade as whole shares, though some brokers now offer fractional share purchasing.

Which Investment Vehicle Suits Your Goals?

Choosing between ETFs and mutual funds depends on your specific investment objectives, trading preferences, and financial situation.

ETFs offer trading flexibility and real-time pricing,lower expense ratios and cost efficiency, tax efficiency and control over taxable events, have smaller amounts to invest initially, use technical analysis or tactical trading strategies, and seek transparency in portfolio holdings.

Mutual funds may be suitable if you prefer professional active management, want to establish automatic investment plans, value consistent daily pricing without intraday volatility, believe skilled managers can outperform passive indices, already have access to no-load low-cost mutual fund options, and prefer the simplicity of fractional share investing.

Important: Neither investment vehicle is inherently superior. The appropriate choice depends on your individual circumstances, investment timeline, and financial goals. Many investors successfully incorporate both ETFs and mutual funds within diversified portfolios.

Portfolio Diversification and Liquidity

Both investment vehicles provide essential diversification benefits, allowing you to gain exposure to hundreds or thousands of securities through a single transaction, reducing the impact of any single security's poor performance.

For Singapore investors seeking overseas market exposure, both vehicles provide access to US equity markets, international developed markets, emerging markets, fixed income securities, and sector-specific exposure.

ETFs offer high intraday liquidity, with settlement typically within two business days. Mutual fund redemptions process at the end-of-day NAV price, with proceeds available within one to two business days.

Frequently Asked Questions

Can I switch between ETFs and mutual funds easily?

Yes, you can sell positions in one investment vehicle and purchase the other, though this creates a taxable event if held in a taxable account. Singapore investors should consider transaction costs and potential tax implications when switching between investment types.

Do ETFs or mutual funds perform better over time?

Performance depends on the specific fund rather than the vehicle type. Passively managed ETFs tracking the same index as index mutual funds should deliver similar returns before fees. Actively managed mutual funds may outperform or underperform passive strategies depending on manager skill and market conditions.

Are ETFs or mutual funds safer investments?

Neither investment vehicle is inherently safer. Both carry market risk based on their underlying holdings. Safety depends on the fund's investment strategy, asset allocation, and risk management approach rather than whether it's structured as an ETF or mutual fund.

Can Singapore investors access both US and Singapore-listed ETFs and mutual funds?

Yes, Singapore investors can access both local and international markets through brokers licensed by the Monetary Authority of Singapore. Comprehensive trading platforms provide access to ETFs and mutual funds across multiple markets, enabling global portfolio diversification.

How do I start investing in ETFs or mutual funds?

Open a brokerage account with a licensed platform that provides access to your desired markets. Fund your account, research suitable ETFs or mutual funds aligned with your investment objectives, and execute your first trades.

Conclusion

Understanding the differences between ETFs and mutual funds empowers Singapore investors to make informed decisions when building diversified portfolios. ETFs offer trading flexibility, lower costs, and tax efficiency, making them attractive for cost-conscious investors who value intraday trading capabilities. Mutual funds provide professional active management, automatic investment options, and consistent pricing for investors who prefer these features.

Your choice should reflect your investment timeline, cost sensitivity, trading preferences, and belief in active versus passive management strategies. Many successful investors incorporate both vehicles within their portfolios, leveraging the strengths of each to achieve specific investment objectives.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.