Leveraged ETFs: High-Risk Amplified Returns Explained

Leveraged ETFs offer amplified market exposure through 2x or 3x daily returns,but come with significant risks including volatility decay and compounding effectsthat make them unsuitable for long-term holding.

TL;DR: Leveraged Exchange-Traded Funds (ETFs) amplify daily market returns through 2x or 3x exposure using derivatives. While they may offer potential for substantial short-term gains, they carry significant risks including volatility decay, amplified losses, and compounding effects that erode long-term value. These products are designed exclusively for experienced, short-term traders who understand the daily reset mechanism.

Leveraged ETFs represent one of the most powerful and misunderstood instruments in modern financial markets. These specialized funds promise to multiply the daily returns of underlying indices, offering traders the allure of amplified gains without the complexity of margin accounts or derivatives trading. However, this amplification cuts both ways, magnifying losses just as effectively as profits.

According to recent market data, there are currently 284 US-listed leveraged ETFs managing approximately USD 114 billion in assets. Despite their growing popularity, these instruments remain fundamentally different from traditional ETFs and require a thorough understanding of their mechanics, risks, and appropriate use cases. This guide explains how leveraged ETFs work, why they behave unexpectedly over time, and when they might fit into a disciplined trading strategy.

What Are Leveraged ETFs?

A leveraged ETF is an exchange-traded fund designed to deliver a multiple of the daily performance of an underlying index or asset. The most common leverage ratios are 2x (double) and 3x (triple), though some funds offer different multiples or inverse exposure.

Unlike traditional Exchange-Traded Funds (ETFs) that hold the actual securities in an index, leveraged ETFs typically use financial derivatives such as total return swaps and futures contracts to achieve their stated leverage ratio. These derivative positions require daily adjustment to maintain the target exposure.

The key distinction lies in the "daily" aspect of their objective. If an index rises 1% today, a 2x leveraged ETF aims to rise approximately 2% today. If the same index falls 1% tomorrow, the leveraged ETF aims to fall approximately 2% tomorrow. This daily reset mechanism has profound implications for longer holding periods.

Leveraged ETFs employ swap agreements with investment banks. For example, a 2x leveraged ETF tracking the S&P 500 might enter into swap agreements worth 200% of its net asset value. If the fund has USD 100 million in assets, it would hold swap positions providing exposure to USD 200 million worth of S&P 500 returns. The fund also maintains collateral to support these positions and protect against counterparty risk.

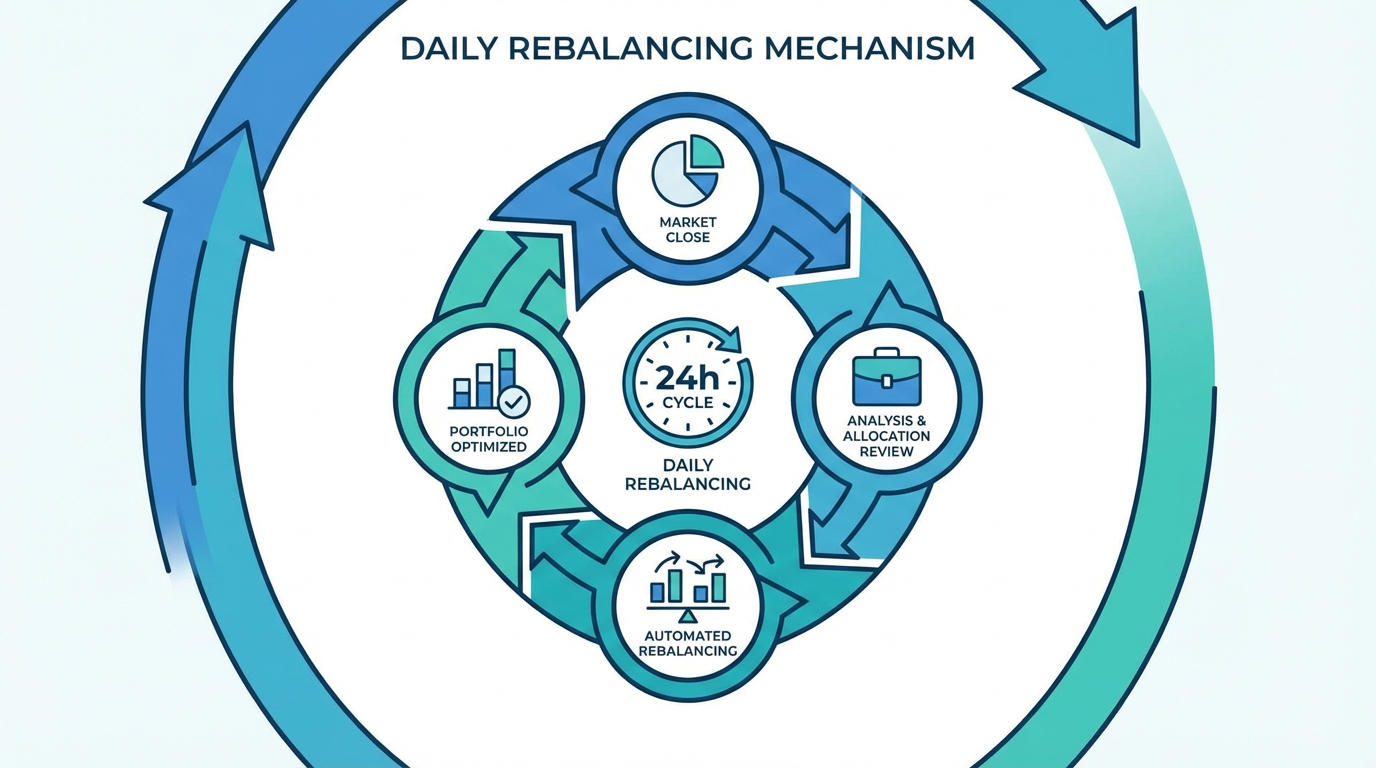

How Daily Rebalancing Works

The daily rebalancing process is the defining characteristic of leveraged ETFs and the source of their most significant risks. Each trading day, the fund resets its exposure to achieve the target leverage ratio based on the current net asset value.

Consider a simplified example with a 2x leveraged ETF starting with USD 100 million in net asset value (NAV). On day one, the fund establishes derivative positions providing USD 200 million in index exposure. If the index rises 5% that day, the fund gains USD 10 million, bringing its NAV to USD 110 million.

At the close of day one, the fund must rebalance. To maintain 2x leverage on the new USD 110 million NAV, it needs USD 220 million in total exposure. It must increase its derivative positions to reach the new target. This process repeats every single trading day.

This daily reset means the fund is essentially marked to market every night and starts fresh the next day. The mathematics of this process creates path dependency, where the sequence and magnitude of daily returns matter just as much as the cumulative change in the underlying index. In trending markets, daily rebalancing can enhance returns beyond the stated multiple. However, in volatile or sideways markets, this mechanism works against investors through volatility decay.

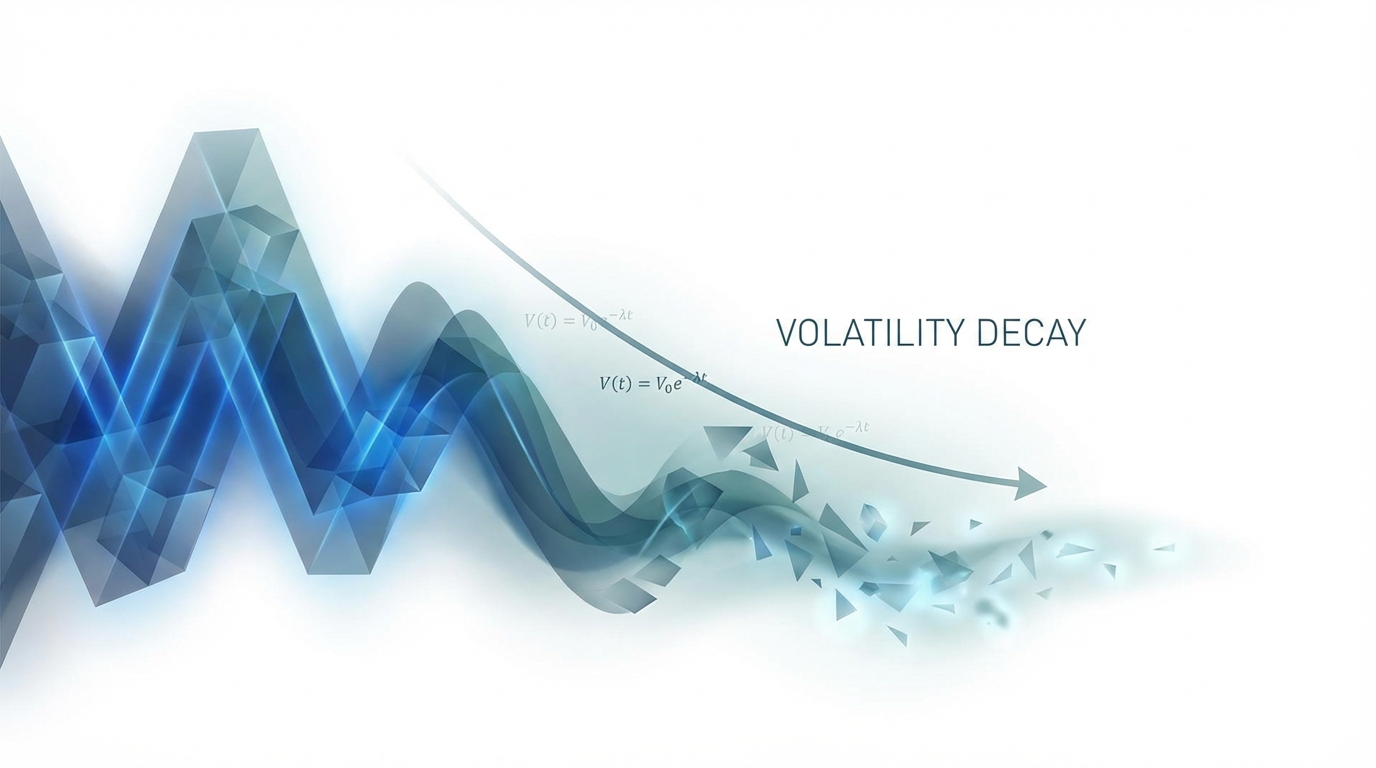

Understanding Volatility Decay

Volatility decay, also called beta slippage or leverage decay, represents one of the most misunderstood aspects of leveraged ETFs. This phenomenon occurs when daily compounding in volatile markets causes the leveraged ETF to underperform its expected multiple of the index return over time.

Here is a concrete example. Assume an index starts at 100 and experiences these daily moves:

Day 1: Falls 10% to 90

Day 2: Rises 11.11% back to 100

The index returns to its starting value with no net change. However, a 2x leveraged ETF would experience:

Day 1: Falls 20% (2x the 10% decline)

Day 2: Rises 22.22% (2x the 11.11% gain)

Starting at 100, the leveraged ETF would fall to 80 after day one. On day two, it would rise to 97.78 (80 × 1.2222). Despite the underlying index being unchanged, the leveraged ETF has lost 2.22% of its value.

The impact of daily rebalancing varies based on market conditions. Steady uptrends with low volatility may boost returns beyond the simple multiple. Steady downtrends cause rapid losses but may not lose quite as much as expected due to the shrinking base. Volatile sideways markets can result in repeated movements that may lead to erosion of value. This mathematical reality is a key factor in how leveraged ETFs are structured, with performance calculated on a daily basis. As a result, these ETFs are generally intended for short-term or daily trading rather than long-term holding.

Key Risks of Leveraged ETFs

Understanding the comprehensive risk profile is essential for anyone considering these instruments.

Amplified Losses

Losses are magnified by the same factor as gains. For example, if you hold a 3x leveraged ETF and the underlying index falls 10% in a single day, your position would decline by approximately 30%. In extreme market conditions, some leveraged ETFs have historically experienced declines of 90% or more.

Path Dependency

Two different return sequences that result in the same ending index value will produce different outcomes for a leveraged ETF holder. Research has shown that in most historical market conditions, holding leveraged ETFs for extended periods results in returns that significantly underperform the stated multiple of the index return.

Higher Costs

Leveraged ETFs often have higher expense ratios than broad-market index ETFs. In the market, leveraged ETFs are commonly observed to carry annual expense ratios in the range of approximately 0.75% to 1.00% or higher, while many passive index ETFs have expense ratios that are typically below 0.20%. These higher fees reflect the costs of maintaining derivative positions, daily rebalancing, and counterparty payments.

Counterparty and Liquidity Risks

Because leveraged ETFs rely on derivative contracts with financial institutions, they carry counterparty risk. Additionally, during extreme market stress, these ETFs may experience tracking errors or trade at significant premiums or discounts to net asset value.

When to Consider Leveraged ETFs

Given their characteristics, leveraged ETFs are appropriate only in specific situations for certain types of traders.

Leveraged ETFs are designed for experienced traders who understand the daily reset mechanism, have strong short-term market views, can actively monitor market performance throughout the trading day, accept substantial losses, and plan to hold positions for days or weeks at most.

Appropriate scenarios include clear directional trades when analysis suggests significant near-term movement, short-term momentum trading in trending markets, event-driven strategies around Federal Reserve announcements or earnings seasons, and intraday trading positions held only during a single session.

Strategic Benefits

Despite their risks, leveraged ETFs serve legitimate purposes. They provide amplified short-term exposure without the complexity of options or futures. A trader anticipating positive technology sector performance might use a 2x or 3x sector ETF to maximize potential gains over a few weeks.

Leveraged ETFs may also offer capital efficiency. For example, instead of investing USD 10,000 for USD 10,000 of exposure, you could invest USD 5,000 in a 2x leveraged ETF while keeping USD 5,000 available for other opportunities. Inverse leveraged ETFs may serve as short-term portfolio hedges during expected downturns without selling long-term holdings.

Frequently Asked Questions

Can you hold leveraged ETFs long-term?

While technically possible, it is strongly discouraged. Due to daily rebalancing and volatility decay, leveraged ETFs typically underperform their expected multiple over weeks, months, or years. Historical data consistently shows that long-term holding results in returns that significantly diverge from expectations.

How much can you lose with a leveraged ETF?

You can lose your entire investment. In extreme scenarios with multiple consecutive days of severe declines, a 3x leveraged ETF could theoretically approach zero value. The amplified exposure means losses accumulate much faster than with traditional investments.

Are leveraged ETFs good for beginners?

No. They require thorough understanding of daily rebalancing mechanics, compounding effects, volatility decay, and active risk management. The amplified losses can be financially devastating for those who do not fully understand how these products work.

Do leveraged ETFs pay dividends?

Some leveraged ETFs distribute dividends, but amounts are typically modest and highly variable. Dividends from underlying securities are incorporated into the daily net asset value calculation. However, investors should consider not relying on leveraged ETFs for dividend income.

What happens to leveraged ETFs in a market crash?

During market crashes, leveraged ETFs experience amplified losses that can be severe. A 3x leveraged ETF could lose 30% or more in a single day if the underlying index falls 10%. Multiple consecutive down days compound these losses rapidly.

Regulatory and Tax Considerations

In the United States, leveraged ETFs are regulated by the Securities and Exchange Commission (SEC), which has expressed concerns about their complexity and risks for retail investors. Some brokerage firms impose restrictions requiring investors to acknowledge risk disclosures before allowing purchases.

Leveraged ETFs are taxed as equity securities, with capital gains and losses following standard rules based on holding period. Distributions may include ordinary dividends, qualified dividends, and capital gains distributions, each with different tax treatment.

Conclusion

Leveraged ETFs represent powerful but specialized trading instruments that amplify both opportunities and risks. Their daily reset mechanism and compounding effects create behavior that diverges significantly from simple multiples of index returns. Volatility decay erodes value in choppy markets, while high expense ratios and counterparty risks add complexity.

These products serve a legitimate purpose for experienced, short-term traders who understand their mechanics and actively manage positions. However, they are fundamentally unsuitable for long-term investing, passive strategies, or investors lacking the knowledge to manage their unique risks.

Before trading leveraged ETFs, ensure you thoroughly understand daily rebalancing, compounding effects, and volatility decay. Start with small position sizes, maintain strict stop-loss disciplines, and plan to hold positions for days or weeks at most. Monitor your positions actively and be prepared for substantial volatility.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.