Bond ETFs: Fixed Income Investing from Singapore

Learn how bond exchange-traded funds offer Singapore investors accessible,diversified fixed income exposure with competitive yields, daily liquidity, andtransparent pricing.

TL;DR: Bond ETFs (exchange-traded funds) offer Singapore investors a practical way to access diversified fixed income exposure through a single investment. With the higher-for-longer interest rate environment in 2026, bond ETFs combine steady income generation, daily liquidity, and transparent pricing, making them an accessible alternative to individual bonds or government securities.

Fixed income investing has gained renewed attention among Singapore investors as interest rates remain elevated. With the US Federal Reserve maintaining its policy band at 4.25 % to 4.5 %, bond ETFs have emerged as a compelling tool for generating income while managing portfolio volatility.

Bond exchange-traded funds provide access to diversified baskets of bonds through a single, tradable security. Unlike traditional bonds that require substantial capital and offer limited liquidity, bond ETFs trade on exchanges throughout market hours, offering flexibility that aligns with modern investment strategies.

This guide explores how bond ETFs work, their advantages and limitations, and practical considerations for Singapore investors looking to build fixed income exposure within their portfolios.

What Are Bond ETFs?

A bond ETF is an investment fund that holds a diversified portfolio of fixed income securities and trades on stock exchanges like individual stocks. These funds track specific bond indices, providing exposure to government bonds, corporate bonds, or other fixed income instruments through a single purchase.

Unlike individual bonds that have fixed maturity dates, bond ETFs maintain perpetual portfolios. As bonds within the fund mature, fund managers replace them with new securities that match the fund's investment criteria. This continuous rebalancing ensures the fund maintains its target duration and credit quality profile.

Singapore investors can access bond ETFs through MAS-licensed brokers. Longbridge provides access to a range of investment products, including ETFs listed on Singapore and US exchanges, enabling comprehensive portfolio construction across different markets.

Tip: Bond ETFs typically distribute income monthly or quarterly, providing more frequent cash flow compared to individual bonds that usually pay interest semi-annually.

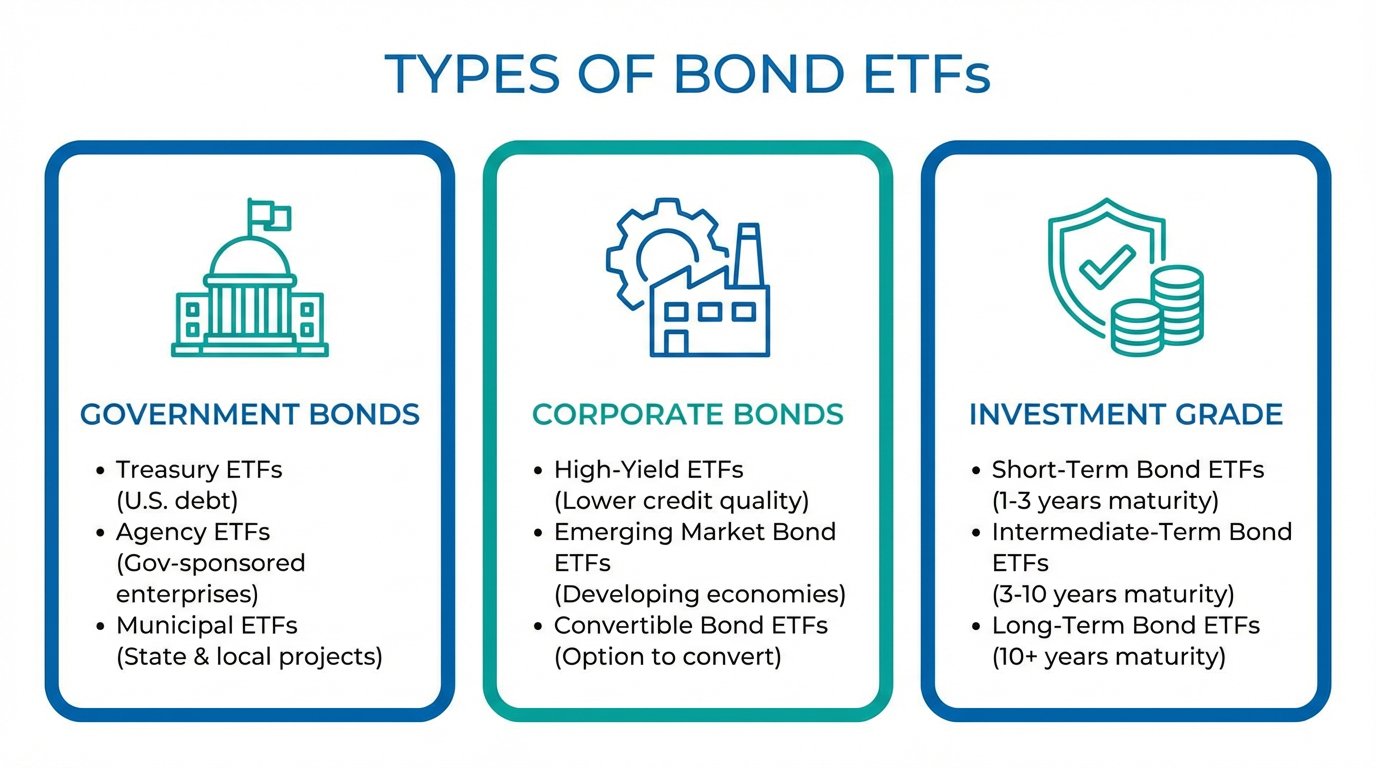

Understanding Different Types of Bond ETFs

Bond ETFs come in several categories, each serving different investment objectives and risk profiles.

Government Bond ETFs

Government bond ETFs invest in debt securities issued by national governments, offering lower credit risk suitable for conservative investors. In Singapore, the ABF Singapore Bond Index Fund provides exposure to Singapore Dollar-denominated government bonds and statutory board securities issued by entities such as the Housing and Development Board (HDB).

According to data from the Monetary Authority of Singapore (MAS), Singapore's bond market operates under robust regulatory oversight. This framework provides structural investor protections, including fund asset segregation and regular auditing. While government backing minimises default risk, these instruments typically offer lower yields compared to corporate alternatives.

Corporate Bond ETFs

Corporate bond ETFs hold debt securities issued by companies, typically focusing on investment grade bonds with credit ratings of BBB or higher. Corporate bonds generally offer higher yields than government securities to compensate investors for additional credit risk.

Regional and Duration-Specific ETFs

Bond ETFs also vary by geographic focus and duration targets. Short-term bond ETFs hold securities maturing in one to three years, offering lower interest rate sensitivity. Long-term bond ETFs extend beyond ten years, providing higher yields but exposing investors to greater price volatility when interest rates fluctuate.

Key Benefits of Bond ETFs

Bond ETFs offer several structural advantages that make them attractive for building fixed income exposure.

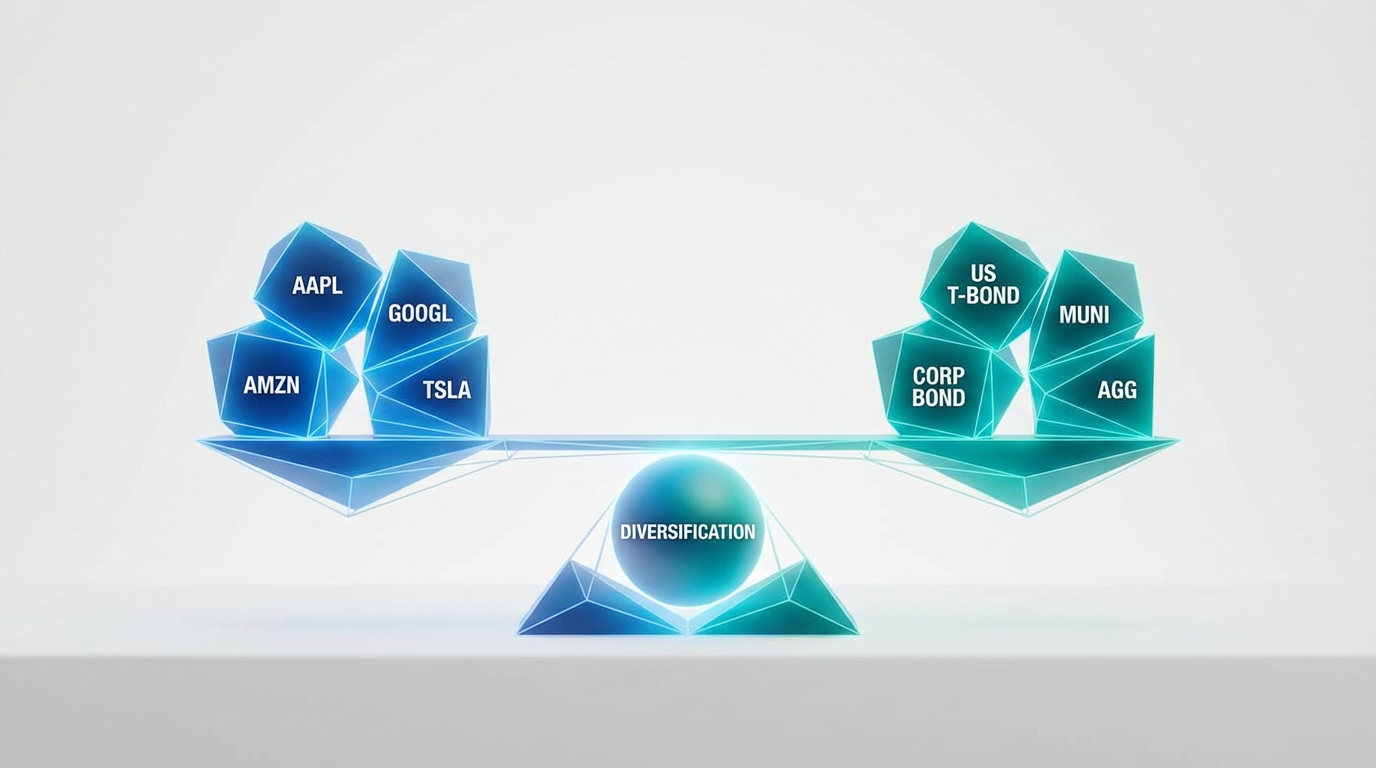

Diversification with Lower Capital Requirements

Building a diversified bond portfolio through direct purchases can require USD 250,000 or more. Bond ETFs provide access to dozens or hundreds of individual bonds through a single share purchase. According to research from Vanguard, a bond ETF could contain hundreds or thousands of bonds, making it less risky than owning a handful of individual bonds.

Enhanced Liquidity and Transparent Pricing

Bond markets often lack the continuous trading and transparent pricing available in equity markets. Bond ETFs trade on exchanges throughout market hours, providing continuous price discovery and the ability to enter or exit positions quickly.

Cost Efficiency

Bond ETFs typically carry significantly lower costs than actively managed mutual funds. According to industry data, bond ETF expense ratios average around 0.29 %, compared to 0.70 % for mutual funds. Singapore-listed bond ETFs have expense ratios ranging from 0.20 % to 0.50 %, making them a highly cost-effective vehicle for long term investors.

Important Risks to Consider

While bond ETFs offer numerous advantages, they also carry specific risks that investors must understand.

Interest Rate Risk

Interest rate risk represents the primary concern for bond investors. Duration measures a bond fund's sensitivity to interest rate changes. A bond ETF with a duration of 5 years will decline approximately 5 % in value if interest rates rise by 1 %. According to Vanguard's analysis, longer-dated bonds include additional interest rate risk, making them more sensitive to rate changes.

Credit Risk

Credit risk refers to the possibility that bond issuers will fail to make scheduled interest or principal payments. While diversification reduces the impact of any single default, bond ETFs remain exposed to broader deterioration in credit quality. Corporate bond ETFs carry higher credit risk than government bond funds.

No Guaranteed Maturity Value

Unlike individual bonds that return principal at maturity, bond ETFs never mature. This perpetual structure means investors cannot simply hold to a specific date to recover their initial capital, making bond ETFs less suitable for investors with specific future obligations requiring principal certainty.

Building a Diversified Portfolio with Bond ETFs

Bond ETFs serve multiple roles within comprehensive investment strategies, from generating income to providing ballast against equity market volatility.

Determining Appropriate Allocation

The appropriate bond allocation depends on individual circumstances including age, risk tolerance, investment timeframe, and income needs. Younger investors with longer time horizons typically allocate smaller percentages to bonds, while those approaching retirement often increase fixed income allocations to preserve capital and secure steady cash flow.

Combining Different Bond ETF Types

Rather than concentrating capital in a single bond ETF, investors often benefit from combining different fund types. A core bond allocation might include a broad investment grade fund, supplemented by shorter-duration holdings for stability.

Bond ETFs Compared to Alternative Fixed Income Options

Singapore investors can access fixed income exposure through several avenues beyond bond ETFs.

Bond ETFs vs Individual Bonds

Individual bonds provide direct ownership where investors know the issuer, coupon rate, and maturity date. Bond ETFs offer pooled exposure with diversification and liquidity but eliminate the principal certainty of holding bonds to fixed maturity date. The key trade-off is diversification and convenience versus control and certainty.

Bond ETFs vs Singapore Savings Bonds

Singapore Savings Bonds (SSB) offer flexible monthly redemption with no capital loss. According to MAS data, SSB yields averaged around 2.3 % annually (based on long-term holdings of up to 10 years). Bond ETFs typically offer higher yields of 2.5 % to 3.2 % annually, along with potential for capital appreciation if rates decline. However, bond ETFs carry price volatility and no redemption guarantee, subjecting investors to capital volatility.

Bond ETFs vs Treasury Bills

Singapore Treasury Bills (T-bills) are short-term government securities maturing in six months or one year. Bond ETFs provide longer duration exposure, capturing higher yields. The choice depends on investment timeframe and income needs.

How to Start Investing in Bond ETFs

Beginning with bond ETFs requires understanding selection, purchase, and ongoing monitoring.

Selecting Appropriate Bond ETFs

Start by identifying investment objectives. Review fund characteristics including credit quality, duration, geographic focus, and expense ratios. Review the fund's top holdings and sector allocations to understand actual exposure.

Opening an Investment Account

Bond ETF purchases require a brokerage account with access to relevant exchanges. Longbridge, as an MAS-licensed digital brokerage, provides access to ETFs across Singapore and US markets. The platform enables investors to track market performance and execute trades seamlessly across multiple exchanges.

Executing Initial Purchases

Consider using limit orders rather than market orders. Limit orders specify the maximum price you're willing to pay, protecting against price spikes. Start with a core position that aligns with your target allocation.

Frequently Asked Questions

Do bond ETFs mature like individual bonds?

Bond ETFs do not mature. Unlike individual bonds with fixed maturity dates, bond ETFs maintain perpetual portfolios by continuously replacing maturing bonds with new securities. This structure provides ongoing exposure but removes the certainty of receiving a defined principal repayment at a specific future date.

How do bond ETFs generate income?

Bond ETFs generate income from interest payments received on their underlying bond holdings. The fund aggregates these payments and distributes them to shareholders, typically monthly or quarterly. Distribution amounts vary based on the yields of bonds held within the fund.

Are bond ETFs suitable during rising interest rates?

Rising interest rates cause bond prices to decline, affecting bond ETF values. However, bond ETFs automatically reinvest proceeds from maturing bonds into new securities at higher prevailing yields, gradually improving the fund's income generation. Short-duration bond ETFs experience smaller price declines during rising rate environments.

How do bond ETF expense ratios affect returns?

Expense ratios represent the annual percentage of fund assets charged for management and operations. A bond ETF with a 0.30 percent expense ratio deducts USD 30 annually per USD 10,000 invested. Lower expenses directly increase the net yield received by investors.

Can I lose money investing in bond ETFs?

Bond ETFs can decline in value, resulting in capital losses. Interest rate increases, credit quality deterioration, or broader market stress can cause prices to fall below purchase levels. However, as long as you continue holding, the fund keeps generating income distributions.

How are bond ETF distributions taxed in Singapore?

Singapore does not tax capital gains or impose tax on distributions received from ETFs, whether they are dividend payments from equity ETFs or interest distributions from bond ETFs. However, investors should consult with tax professionals regarding their specific circumstances.

Conclusion

Bond ETFs have become essential tools for Singapore investors seeking diversified fixed income exposure without substantial capital requirements. These funds combine professional management, transparent pricing, and daily liquidity with access to diverse bond markets.

The current higher-for-longer interest rate environment makes bond ETFs particularly relevant, with yields meaningfully above recent historical levels offering attractive income generation and portfolio diversification benefits.

However, bond ETFs carry interest rate risk, credit risk, and lack the principal certainty of individual bonds or Singapore Savings Bonds. Understanding these trade-offs ensures investors select fixed income tools aligned with their objectives and risk tolerance.

For Singapore investors ready to incorporate bond ETFs into their portfolios, accessible platforms and transparent regulatory oversight create a favorable environment for building stable fixed income exposure.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.