ETF vs Unit Trust in Singapore: Fees and Flexibility

ETFs offer lower fees and intraday trading, while unit trusts provide activemanagement and SGD convenience. Learn which investment vehicle aligns with yourfinancial goals.

TL;DR: Exchange-Traded Funds (ETFs) and unit trusts both offer diversified investment opportunities, but they differ significantly in fees, trading flexibility, and suitability for Singapore investors. ETFs generally have lower management fees and intraday trading capabilities, while unit trusts provide active professional management and Singapore Dollar denomination. Investors may consider factors such as cost structure, trading flexibility, and management approach when evaluating these two investment vehicles.

When building your investment portfolio in Singapore, you will likely encounter two popular investment vehicles: Exchange-Traded Funds (ETFs) and unit trusts. Both offer access to diversified portfolios without requiring you to select individual stocks, but they operate quite differently. Understanding the distinctions between these two options, particularly regarding fees and flexibility, helps you make informed decisions aligned with your financial goals.

What Are ETFs and Unit Trusts?

Before comparing the two, it is essential to understand what each investment vehicle represents.

Exchange-Traded Funds (ETFs)

An Exchange-Traded Fund is an investment fund that tracks a specific market index, sector, or asset class. ETFs are traded on stock exchanges throughout the trading day, similar to individual stocks. Most ETFs follow a passive management approach, meaning they replicate the performance of their underlying index rather than attempting to outperform it.

For Singapore investors, ETFs provide exposure to local markets through instruments like the Straits Times Index ETF, as well as international markets including United States equities and Hong Kong shares.

Unit Trusts

Unit trusts, also known as mutual funds in other markets, are collective investment schemes where professional fund managers actively select and manage a portfolio of securities on behalf of investors. Unlike ETFs, unit trusts are not traded on exchanges. Instead, investors buy and redeem units directly through fund managers or distributors at the net asset value (NAV) calculated at the end of each trading day.

Unit trusts typically employ active management strategies, with fund managers making investment decisions to potentially outperform benchmark indices.

The Fee Structure Comparison

Cost considerations play a crucial role when selecting between ETFs and unit trusts, as fees directly impact your investment returns over time.

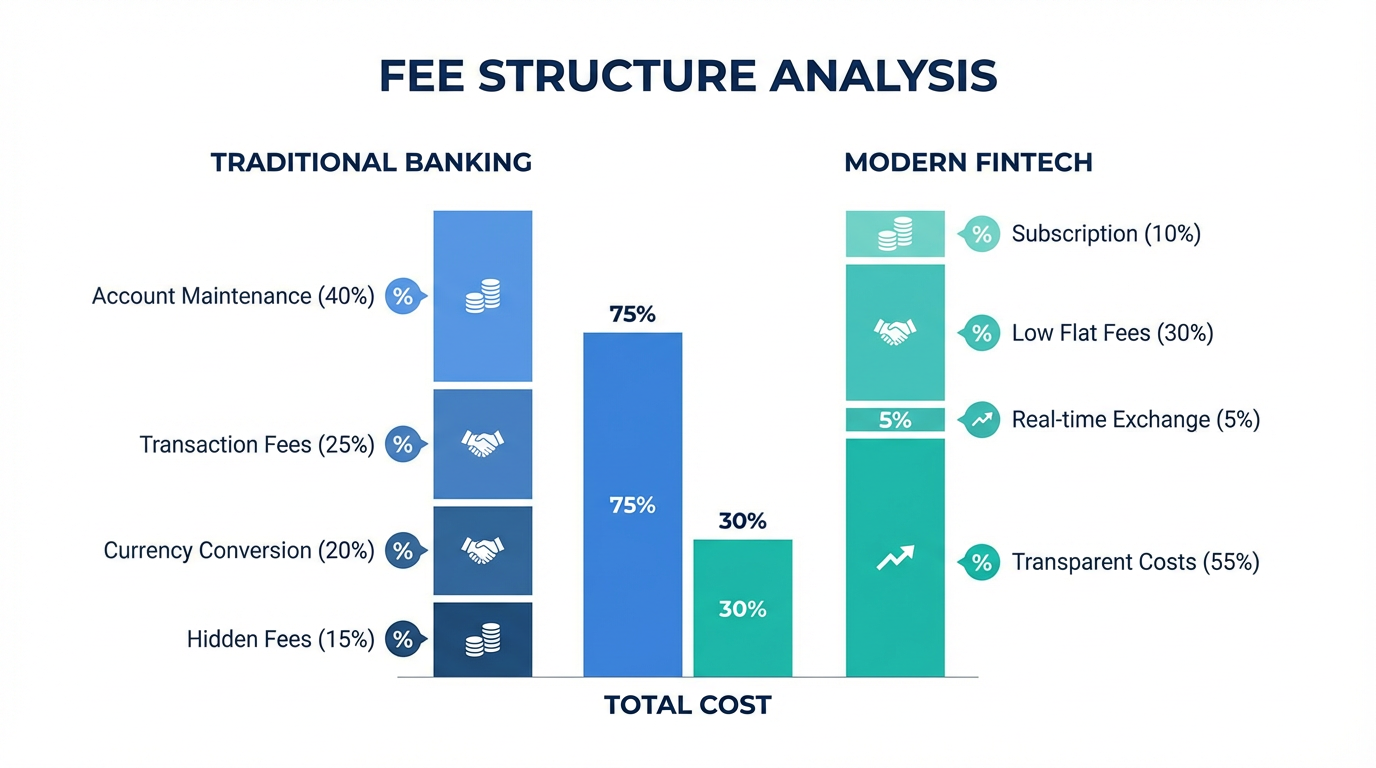

ETF Costs: Lower but Not Zero

ETFs are generally associated with lower costs due to their passive management approach. The Total Expense Ratio (TER) for ETFs typically ranges from 0.20% to 0.50% annually, with some index-tracking funds charging even less.

However, when investing in ETFs, you also need to consider:

Brokerage commissions: You pay trading fees each time you buy or sell ETF shares, similar to stock transactions

Bid-ask spreads: The difference between buying and selling prices can add to transaction costs, particularly for less liquid ETFs traded on the Singapore Exchange (SGX)

Currency conversion fees: Many ETFs are denominated in foreign currencies, requiring currency exchange when Singapore investors transact

Unit Trust Costs: Higher Management Fees

Unit trusts typically carry higher fees due to active management. The TER for actively managed unit trusts in Singapore usually ranges from 1.5% to 2.0% per annum, though some funds may charge more.

Additional costs may include:

Sales charges: Front-end loads of 3% to 5% of your investment amount

Switching fees: Charges for moving between different funds within the same family

Redemption fees: Early withdrawal penalties for certain fund types

While these fees appear higher on the surface, unit trusts denominated in Singapore Dollars eliminate currency conversion costs, and some platforms offer reduced or waived sales charges.

The Hidden Cost Factor: Tax Considerations

An often-overlooked aspect of the ETF versus unit trust comparison involves tax implications for Singapore investors. United States-listed ETFs subject Singapore investors to a 30% withholding tax on dividends, as Singapore does not have a tax treaty with the United States. This substantially reduces your effective returns from dividend-paying US ETFs.

Additionally, Singapore investors holding US-listed ETFs face potential United States estate tax exposure, with only a USD 60,000 exemption, which means estates exceeding this threshold could face up to 40% estate tax.

Many unit trusts structured through Ireland or Luxembourg offer more favorable tax treatment, with dividend withholding rates between 0% and 15%, making them more tax-efficient for certain international exposures despite their higher management fees.

Trading Flexibility and Liquidity

The flexibility with which you can buy and sell your investments differs significantly between ETFs and unit trusts.

ETF Trading: Intraday Flexibility

ETFs trade on stock exchanges during market hours, allowing you to buy and sell throughout the trading day at real-time prices, implement limit and stop-loss orders, and respond quickly to market movements. This intraday capability appeals to active traders but may encourage counterproductive behavior for long-term investors.

Unit Trust Trading: End-of-Day Transactions

Unit trusts process transactions at the net asset value calculated after market close. All orders execute at the same closing NAV, orders take one to two business days to process, and pricing is less transparent during the trading day. This structure suits long-term investors who focus on fundamental value and removes temptation for emotional, reactive trading decisions.

Investment Minimums and Accessibility

ETFs generally have no formal minimum investment requirements beyond the cost of a single share, making them accessible to investors with limited capital. Some platforms even offer fractional share investing.

Unit trusts typically require higher initial investments, often starting from SGD 1,000 to SGD 5,000, though regular savings plans may offer lower monthly minimums of around SGD 100 per month.

Management Approach: Active versus Passive

The fundamental difference in management philosophy influences both cost and potential performance.

Passive Management in ETFs

Most ETFs follow passive index-tracking strategies, aiming to replicate their benchmark index. This approach maintains low portfolio turnover, provides predictable performance aligned with the underlying index, eliminates manager selection risk, and offers transparency with daily disclosed holdings.

Active fund performance varies depending on the strategy, market conditions, and manager decisions.

Active Management in Unit Trusts

Unit trusts employ professional fund managers who actively select securities to outperform the market. This strategy potentially generates returns exceeding benchmarks, allows adaptation to changing market conditions, and provides access to specialized strategies and niche markets. However, performance depends on fund manager expertise, and higher fees must be overcome to deliver superior net returns.

Currency Considerations for Singapore Investors

Currency denomination affects both convenience and returns for Singapore-based investors.

ETF Currency Exposure

Many ETFs are denominated in foreign currencies, primarily United States Dollars. Singapore investors incur currency conversion fees and face foreign exchange risk that can amplify or reduce returns. Some SGX-listed ETFs offer Singapore Dollar denomination, eliminating conversion costs.

Unit Trust Currency Options

Most unit trusts available to Singapore investors offer Singapore Dollar-denominated share classes, allowing local currency investment without conversion fees. This simplifies portfolio tracking and provides access to currency-hedged versions that reduce foreign exchange volatility.

Which Investment Makes More Sense for You?

The choice between ETFs and unit trusts depends on your individual circumstances, investment goals, and preferences.

ETFs Typically Suit Investors Who:

Prefer lower ongoing management fees

Want intraday trading flexibility

Are comfortable with passive investment strategies

Prefer transparency in holdings and daily pricing

Unit Trusts Typically Suit Investors Who:

Value professional active management

Prefer Singapore Dollar denomination for convenience

Want specialized strategies or niche market access

Seek tax-efficient international exposure through Ireland or Luxembourg-domiciled funds

Invest through regular savings plans with monthly contributions

Many investors combine both vehicles, using low-cost ETFs for core market exposure while employing unit trusts for specialized segments or tax-efficient international access.

Practical Considerations for Singapore Investors

Choose a trading platform that offers access to both ETFs and unit trusts, with competitive pricing and comprehensive market access. Build your portfolio with clear asset allocation goals, using ETFs for core holdings and unit trusts for specialized strategies.

Regularly review total costs including management fees, transaction costs, currency charges, and tax implications. A seemingly cheaper option may prove more expensive when all factors are considered.

Frequently Asked Questions

Are ETFs or unit trusts better for beginners?

ETFs often suit beginners due to their lower costs, transparency, and simplicity. However, unit trusts may be preferable if you value professional management guidance and prefer Singapore Dollar investments without currency considerations. The right choice depends on your comfort level with investment decisions and willingness to manage your portfolio actively.

Can I hold both ETFs and unit trusts in my portfolio?

Yes, many investors combine ETFs and unit trusts to balance cost efficiency with specialized exposure. You might use low-cost ETFs for core market holdings while incorporating unit trusts for active management in specific sectors or regions where you believe active management can add value.

How do ETFs and unit trusts differ in terms of tax treatment in Singapore?

Singapore does not impose capital gains tax on either ETFs or unit trusts, making both tax-efficient locally. However, foreign dividend withholding taxes differ, with United States-listed ETFs subject to 30% withholding tax while certain unit trust structures may qualify for reduced rates of 0% to 15% depending on domicile.

What is the typical holding period for ETFs versus unit trusts?

ETFs suit both short-term traders and long-term investors due to intraday trading flexibility. Unit trusts are typically structured for longer holding periods, with some imposing early redemption fees. Your investment time horizon should guide your choice, with longer-term investors finding either option suitable.

How liquid are ETFs compared to unit trusts?

ETFs traded on major exchanges offer high liquidity with immediate execution during market hours. Unit trusts process redemptions at end-of-day NAV, typically settling within one to two business days. For most long-term investors, this liquidity difference has minimal practical impact.

Conclusion

The decision between ETFs and unit trusts involves weighing multiple factors including fees, flexibility, management approach, and your personal investment preferences. ETFs generally offer lower costs and trading flexibility, while unit trusts provide professional active management and currency convenience for Singapore investors.

Rather than viewing this as an either-or decision, consider how each investment vehicle serves different roles within your broader portfolio strategy. Understanding the true costs, including often-overlooked factors like tax treatment and currency conversion, helps you make informed choices that align with your financial objectives.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.