Mutual Funds Singapore: Complete Investment Guide

Learn how mutual funds in Singapore offer professionally managed, diversified investments. Complete guide covering fund types, selection strategies, and practical steps to start.

TL;DR: Mutual funds in Singapore offer professionally managed, diversified investment options ideal for beginners and busy professionals. This guide covers fund types, selection criteria, tax benefits, and practical steps to start investing—all while maintaining a balanced understanding of benefits and risks.

Investing can feel overwhelming, especially when you're faced with countless options and complex financial jargon. If you're a Singaporean looking to grow your wealth without spending hours analysing individual stocks, mutual funds might be the solution you need. These pooled investment vehicles combine professional management with instant diversification, making them accessible even if you're starting with just a few hundred dollars.

This comprehensive guide will walk you through everything you need to know—from the basics of how these funds work to practical strategies for choosing the right ones for your financial goals.

What Are Mutual Funds and How Do They Work?

Mutual funds, often called unit trusts in Singapore, are investment products that pool money from multiple investors to purchase a diversified portfolio of assets. When you invest in a mutual fund, you're buying units that represent your share of the fund's total holdings.

A professional fund manager makes investment decisions on behalf of all unitholders, researching markets and selecting securities based on the fund's objectives. This structure offers practical advantages: access to professional expertise, diversification across dozens or hundreds of securities, and the ability to start with small amounts—many funds accept initial investments of just one hundred dollars per month.

You purchase units at the fund's Net Asset Value (NAV), calculated daily by dividing the total value of holdings by the number of outstanding units. As underlying securities change in value, your units follow accordingly.

Regulatory Framework

In Singapore, mutual funds marketed to retail investors must be authorised or recognised by the Monetary Authority of Singapore (MAS). According to MAS regulations, fund providers must issue a prospectus and Product Highlights Sheet that outline the fund's investment strategy, risks, fees, and past performance. This regulatory oversight provides protection for investors—always review these documents before investing.

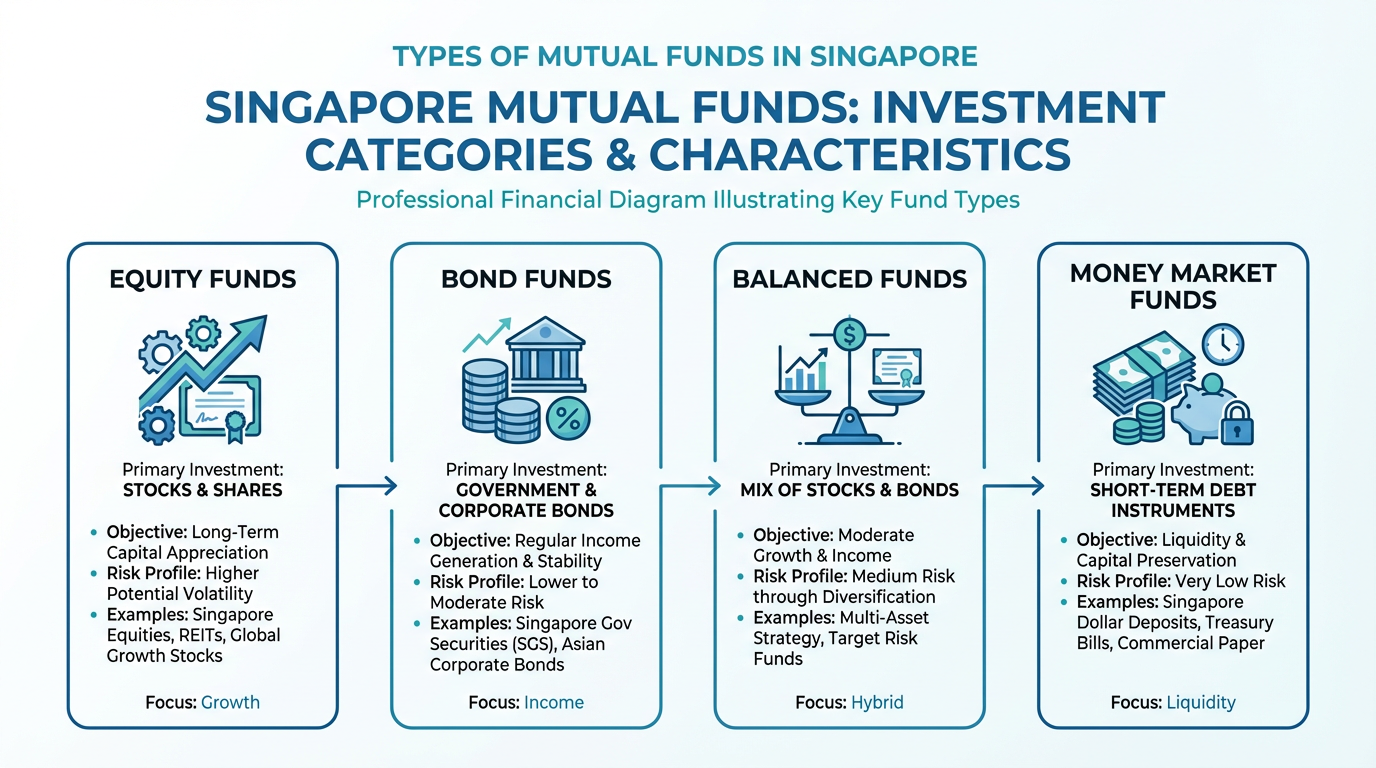

Types of Mutual Funds in Singapore

Understanding the main categories helps you match investment options to your financial objectives and risk tolerance.

Equity Funds

Equity funds invest primarily in stocks, aiming for long-term capital growth. These funds carry higher risk but historically have delivered stronger gains over extended periods. Within equity funds, you'll find growth funds targeting rapidly expanding companies, value funds seeking undervalued stocks, sector funds concentrating on specific industries, and dividend-focused funds prioritising companies with strong payout histories.

Bond and Fixed Income Funds

Bond funds invest in government and corporate debt securities, offering more stability than equity funds while typically delivering higher yields than savings accounts. Government bond funds are generally the most conservative option, while corporate bond funds offer higher potential yields but come with credit risk. Note that bond funds are sensitive to interest rate changes—when rates rise, existing bond prices typically fall.

Balanced and Multi-Asset Funds

Balanced funds offer a convenient all-in-one solution by combining equities and bonds in a single portfolio. Fund managers actively adjust the allocation based on market conditions. This approach simplifies portfolio construction, particularly for investors who prefer not to manage multiple holdings themselves.

Money Market Funds

Money market funds invest in short-term, high-quality debt instruments such as Treasury bills and certificates of deposit. These funds prioritise capital preservation and liquidity rather than high gains. They're suitable for parking emergency funds or short-term savings you'll need within the next year or two.

How to Choose the Right Mutual Funds

Selecting appropriate mutual funds requires evaluating several key factors beyond past performance.

Assess Your Investment Objectives

Start by clarifying what you're trying to achieve. Are you building long-term wealth for retirement, saving for a home down payment, or generating income? Your time horizon and financial goals should guide your fund selection. Longer time horizons allow you to accept more volatility in exchange for potentially higher gains.

Understand Fund Fees and Expenses

Fees significantly impact your gains over time. Even a one percentage point difference in annual fees can reduce your portfolio value by tens of thousands of dollars over several decades.

Look for the Total Expense Ratio (TER) in the fund factsheet—this represents the percentage of fund assets used for management fees and operating expenses annually. Actively managed funds typically charge between one and two percent, while passive index funds often cost less than half a percent.

Evaluate Track Record and Consistency

While past performance doesn't guarantee future outcomes, a fund's history provides useful context. Look beyond short-term gains and examine how the fund has performed over multiple market cycles—ideally five to ten years. Consistency matters more than occasional spectacular years. Pay attention to downside protection: how much did the fund decline during market corrections compared to similar funds?

Research the Management Team

The fund manager's experience and investment approach directly influence outcomes. Review how long the current manager has been in charge—leadership changes can alter a fund's strategy and performance characteristics.

Tax Considerations for Singapore Investors

Understanding the tax treatment of mutual fund investments helps you keep more of what you earn.

Capital Gains and Dividends

Singapore does not impose capital gains tax on individuals, meaning any profit you realise when selling fund units is tax-free. This represents a significant advantage compared to many other countries. However, distributions from funds may be subject to withholding taxes depending on the fund's domicile and income sources.

Using Your Supplementary Retirement Scheme

The Supplementary Retirement Scheme (SRS) is a voluntary programme that provides tax relief on contributions while allowing you to invest in approved mutual funds. Contributions reduce your taxable income in the year they're made, potentially saving thousands of dollars in taxes.

According to the Inland Revenue Authority of Singapore (IRAS), you can contribute up to $15,300 dollars annually if you're a Singapore Citizen or Permanent Resident. When you withdraw funds after the minimum retirement age, only fifty percent of withdrawals are taxable, while early withdrawals before prescribed retirement age face penalties.

Where to Invest in Mutual Funds in Singapore

Several channels offer access to mutual funds, each with distinct advantages.

Online Brokerage Platforms

Digital platforms like Longbridge offer Singaporeans access to different investment products. These platforms typically offer lower transaction costs than traditional banks, user-friendly interfaces, and comprehensive market data.

Longbridge, licensed by the Monetary Authority of Singapore (MAS), provides access to diverse investment products including stocks, Exchange Traded Funds (ETFs), and Real Estate Investment Trusts (REITs). Account opening via MyInfo or SingPass integration allows you to start investing.

Banks and Fund Platforms

Traditional banks provide another route to mutual fund investment through their wealth management divisions. However, bank-distributed funds frequently come with higher fees. Specialised fund platforms aggregate products from multiple fund houses, offering broader selection and often competitive pricing.

Getting Started: Practical Steps

Ready to begin investing in mutual funds Singapore? Follow these steps.

Step 1: Define Your Financial Goals. Be specific about what you're saving for and when you'll need the money. Clear goals drive better investment decisions.

Step 2: Determine Your Risk Tolerance. Honestly assess how you'd react if your investment declined by twenty or thirty percent. Your risk tolerance should reflect both emotional comfort and financial capacity.

Step 3: Open an Investment Account. Choose a platform that matches your needs. Longbridge users can open an account entirely online using SingPass credentials.

Step 4: Research and Select Funds. Use the criteria discussed earlier to evaluate funds.

Step 5: Start Investing Consistently. Dollar-cost averaging—investing a fixed amount regularly—reduces the impact of volatility. Even modest monthly contributions compound significantly over decades.

Step 6: Monitor and Rebalance Periodically. Review your portfolio every six to twelve months. Check performance against benchmarks and ensure your allocation matches your goals.

Common Mistakes to Avoid

Chasing Past Performance: The fund that delivered thirty percent gains last year may perform very differently this year. Focus on consistent long-term performance rather than chasing hot funds.

Ignoring Fees: Small percentage differences compound dramatically. A fund charging two percent annually versus one charging half a percent might seem minor, but over thirty years, that extra one and a half percent can reduce your final portfolio value by more than thirty percent.

Emotional Decision-Making: Market volatility triggers powerful emotions. The impulse to sell during declines—locking in losses—or buy aggressively after gains often leads to poor outcomes. Successful investors maintain discipline through market cycles.

Frequently Asked Questions

Are mutual funds a good investment in Singapore?

Mutual funds can be suitable for many Singapore investors, offering professional management and diversification with relatively low minimum investments. However, suitability depends on your specific financial situation, goals, and risk tolerance. Higher fees compared to Exchange Traded Funds (ETFs) mean you should carefully evaluate whether the active management justifies the cost.

What is the minimum amount needed to start investing in mutual funds?

Many mutual funds in Singapore accept initial investments as low as one hundred dollars for regular savings plans, though lump-sum minimums may be higher—typically one thousand to five thousand dollars. Online platforms often have lower entry requirements than traditional banks.

How are mutual funds taxed in Singapore?

Singapore does not impose capital gains tax on individuals, so profits from selling fund units are tax-free. Distributions may face withholding taxes depending on the fund's domicile. If you invest through the Supplementary Retirement Scheme (SRS), contributions are tax-deductible, but withdrawals are partially taxable according to IRAS regulations.

What is the difference between mutual funds and ETFs?

Both offer diversified portfolios, but they differ in structure and trading. Mutual funds are priced once daily at their Net Asset Value and purchased through platforms. ETFs trade on exchanges throughout the day like stocks, typically have lower expense ratios, and often track indexes passively. Mutual funds may be preferable if you value professional active management.

Conclusion

Mutual funds in Singapore provide an accessible pathway to building diversified investment portfolios with professional management. By understanding fund types, evaluating fees and performance, and maintaining a disciplined approach, you can work toward your financial goals while managing risk appropriately.

Successful investing is about starting early, investing consistently, and staying committed through market cycles. Begin with clear objectives, choose funds that align with your risk tolerance, and adjust as circumstances evolve. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.