Singapore Savings Bonds: A Safe Investment Alternative

Singapore Savings Bonds offer a government-backed investment option with flexible redemption and no capital loss. Explore how SSBs compare to other low-risk alternatives.

TL;DR: Singapore Savings Bonds (SSBs) are government-backed securities offering capital preservation with very low risk of capital loss when held under normal conditions, flexible redemption without penalties, and step-up interest rates that reward longer holding periods. With a minimum investment of SGD 500 and Singapore's AAA credit rating, SSBs provide a low-risk alternative to fixed deposits.

When seeking safe investment options in Singapore, many investors prioritize capital preservation alongside reasonable returns. Singapore Savings Bonds have emerged as a compelling choice for conservative investors who value government-backed security and flexibility. Unlike traditional fixed deposits that lock funds for predetermined periods, Singapore savings bonds offer competitive interest rates with the freedom to redeem at any time without penalties.

This guide explores how Singapore Savings Bonds work, their distinctive step-up interest structure, and how they compare to other low-risk investment alternatives. Whether building an emergency fund, preserving capital, or seeking stable returns, understanding SSBs helps you make informed investment decisions aligned with your financial goals.

What Are Singapore Savings Bonds?

Singapore Savings Bonds are Singapore Government Securities issued by the Monetary Authority of Singapore specifically for individual investors. These bonds provide a low-risk investment option backed by the Singapore Government, which holds the highest AAA credit rating from major international credit rating agencies.

According to the Monetary Authority of Singapore, SSBs combine government security with accessible features for retail investors. Unlike conventional bonds that may fluctuate in value, singapore savings bonds protect your principal amount completely.

Key Features of SSBs

Government Backing and Capital Protection

The Singapore Government fully backs every Singapore Savings Bond, designed to preserve principal when redeemed according to terms. This government backing provides a high level of capital security compared to market-based investments where values fluctuate based on economic conditions.

Accessible Investment Amounts

Start investing in Singapore savings bonds with just SGD 500, making them accessible to beginning investors. The maximum holding limit stands at SGD 200,000 per individual investor.

Flexible Redemption Without Penalties

Redeem your bonds in any given month without facing early withdrawal penalties. This flexibility ensures you retain access to your funds if unexpected needs arise, without sacrificing earned interest.

Long-Term Investment Horizon

Singapore Savings Bonds offer tenure up to 10 years with interest payments every six months directly into your designated bank account. The longer you hold bonds, the higher your average return through the step-up interest structure.

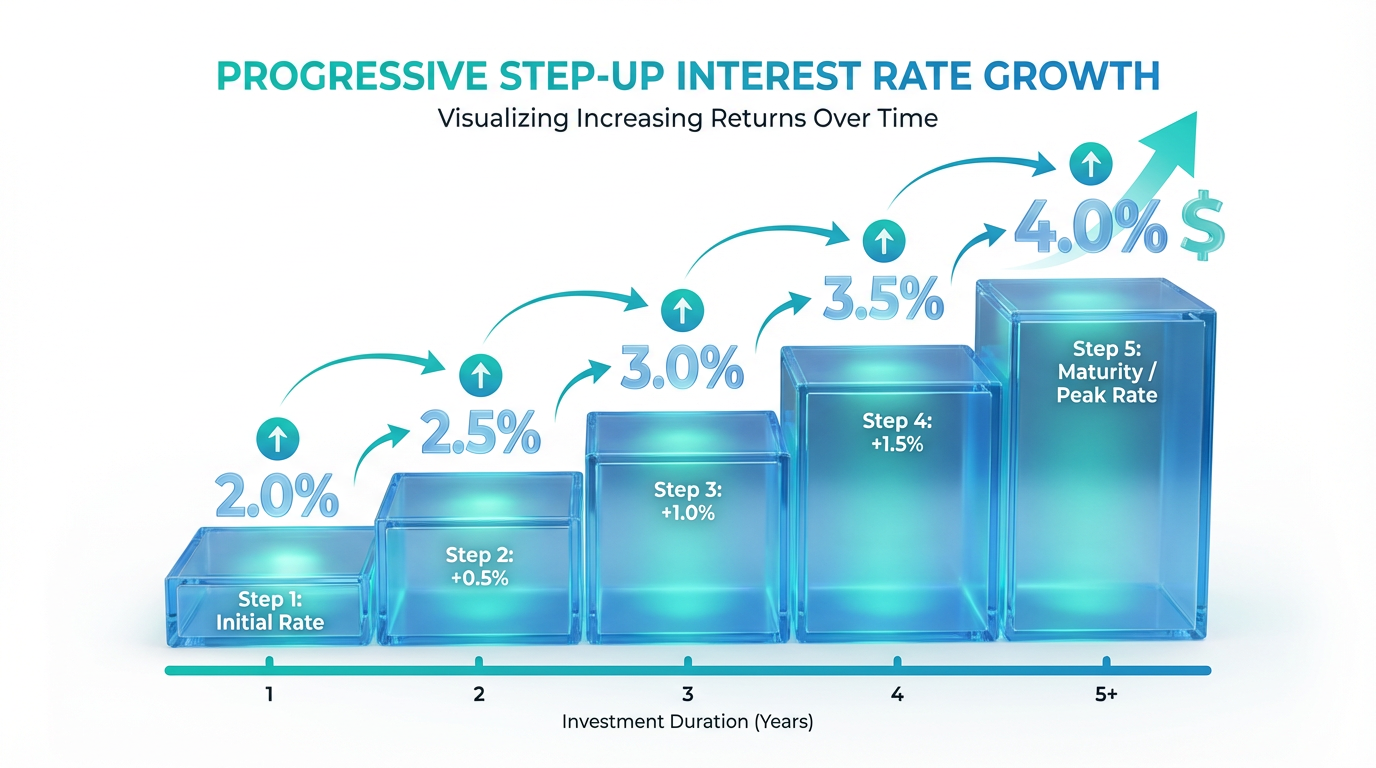

Understanding the Step-Up Interest Structure

The step-up interest structure represents one of the most distinctive characteristics of Singapore savings bonds. Rather than offering flat interest rates, SSBs provide progressively increasing returns the longer you maintain your investment.

How Step-Up Interest Works

When you purchase a Singapore Savings Bond, the interest rate starts lower in the first year and increases annually through the 10-year tenure. According to investment analysis research, this structure incentivizes long-term holding while providing flexibility for early redemption.

The Monetary Authority of Singapore announces the complete interest rate schedule for all 10 years when each new bond issue becomes available. These rates remain locked in once you subscribe, protecting you from future rate fluctuations.

Recent Rate Examples

For the January 2026 tranche (SBJAN26 GX26010A), investors secure a first-year interest rate of 1.35%. Holding the bond for the full 10-year period provides an average return of 2.25% per annum. The current SSB rates for 2026 show 10-year average returns ranging between 2.22% and 2.25% per annum.

The average interest you receive over your holding period matches what you would receive from purchasing Singapore Government Securities of equivalent tenure. The key difference is the payment structure: traditional SGS bonds pay consistent interest yearly, while Singapore savings bonds offer step-up rates that progressively increase annual interest payments.

How to Apply for Singapore Savings Bonds

Applying for Singapore savings bonds involves a straightforward digital process through participating banks. Understanding requirements and application timelines ensures smooth transactions.

Prerequisites for Application

Central Depository Account Requirements

Before applying, you must have an individual Central Depository account with Direct Crediting Service activated. According to Monetary Authority of Singapore guidelines, joint CDP Securities accounts are not accepted.

Your CDP Securities account must have a DCS bank account linked before submitting SSB applications. Participating DCS banks include Citibank, DBS/POSB, HSBC, Maybank, OCBC, Standard Chartered Bank, and UOB. You must be at least 18 years old to open an individual CDP Securities account.

Application Timeline and Process

A new Singapore Savings Bond issue becomes available monthly. The application period opens at 6:00 PM on the first business day of each month and closes at 9:00 PM on the fourth last business day of the same month.

Apply through DBS/POSB, OCBC, and UOB internet banking platforms or ATMs, and OCBC's mobile application. Have your CDP account number ready. Each application incurs a non-refundable SGD 2 transaction fee charged by the participating bank.

Comparing Singapore Savings Bonds with Other Investment Options

Understanding how Singapore savings bonds compare with alternative low-risk investments helps determine optimal capital preservation allocation.

Singapore Savings Bonds vs Fixed Deposits

Interest Rate Structure

Fixed deposits offer flat interest rates throughout the deposit tenure, typically one to three years. Recent fixed deposit rates in Singapore ranged around 1.21% to 1.40% per annum for 12-month tenures as of late 2025.

Singapore savings bonds provide step-up interest increasing annually, with recent 10-year average returns of approximately 2.25% per annum. While first-year SSB rates may be comparable to fixed deposit rates, long-term averages typically exceed fixed deposit returns.

Flexibility and Liquidity

Fixed deposits impose penalties for early withdrawals. Singapore Savings Bonds allow penalty-free redemption at any time, providing superior liquidity while maintaining competitive returns.

Minimum Investment Requirements

Most Singapore banks require minimum deposits of SGD 20,000 or higher for competitive fixed deposit rates. Singapore Savings Bonds start at just SGD 500.

Capital Protection

Fixed deposits enjoy Singapore Deposit Insurance Corporation protection up to SGD 100,000 per depositor. Singapore Savings Bonds carry full Singapore Government backing, supported by Singapore's AAA credit rating.

Singapore Savings Bonds vs Treasury Bills

Singapore Treasury Bills represent another government-backed investment option with six-month or one-year tenures. T-bills can offer higher yields than comparable-period SSB rates during certain market conditions, particularly in rising interest rate environments.

The key tradeoff involves predictability versus yield. SSBs provide certainty about returns for up to 10 years, while T-bills offer shorter commitment periods with yields responding more quickly to changing interest rate conditions.

Singapore Savings Bonds vs Singapore Government Securities Bonds

Traditional Singapore Government Securities bonds offer fixed-rate interest payments and tenures from 2 to 50 years with higher yields than SSBs. However, SGS bond prices fluctuate in the secondary market. Singapore Savings Bonds guarantee full principal return regardless of redemption timing.

Who Should Consider Singapore Savings Bonds?

Singapore Savings Bonds suit specific investor profiles and financial objectives.

Ideal Investor Profiles

Conservative Investors Prioritizing Capital Preservation

If your primary objective involves protecting capital while earning modest returns above inflation, Singapore savings bonds may be suitable for investors seeking capital preservation. Government backing and guaranteed principal return eliminate market risk.

Individuals Building Emergency Funds

The penalty-free redemption feature makes some investors use SSBs as part of their emergency fund allocation due to their liquidity features. Unlike fixed deposits that penalize early withdrawal, you can access your SSB investment quickly if unexpected expenses arise.

Long-Term Savers Seeking Flexibility

Investors planning for medium to long-term goals who value fund access without penalties find Singapore savings bonds may appeal to investors who value flexibility. The step-up interest structure rewards extended holding periods while maintaining liquidity.

Beginning Investors Testing Government Securities

The low SGD 500 minimum allows new investors to experience government bond investing without committing substantial capital.

When SSBs May Not Be Optimal

Singapore Savings Bonds may not suit investors seeking higher growth potential who can accept greater volatility. Short-term savers needing funds within six to 12 months might find higher yields from promotional fixed deposits or Treasury Bills.

Diversifying Beyond Singapore Savings Bonds

While Singapore savings bonds provide excellent capital preservation, a well-structured investment portfolio typically includes diversification across multiple asset classes aligned with your risk tolerance and time horizon.

For Singapore investors, combining the safety of SSBs with exposure to diverse investment products across Singapore, US, and Hong Kong markets may provide exposure to potential capital appreciation alongside preservation. Consider allocating portions to dividend-paying companies, Real Estate Investment Trusts, or Exchange Traded Funds offering diversified exposure.

Modern platforms provide market data and tracking tools that help monitor performance and make informed rebalancing decisions. For deeper understanding, educational resources available at Longbridge Academy offer insights into fundamental analysis and portfolio construction.

Frequently Asked Questions

What happens if I need to redeem my Singapore Savings Bonds before maturity?

You can redeem your Singapore savings bonds anytime without penalties. Submit your redemption request during the monthly redemption window, and receive your full principal plus accrued interest by the second business day of the following month. Interest payment is calculated based on the average rate for the actual period you held the bonds.

How do Singapore Savings Bonds interest payments work?

Interest on Singapore savings bonds is paid every six months directly into the bank account linked to your Central Depository account. The interest rate follows a step-up structure, increasing each year you hold the bond.

Can I hold multiple Singapore Savings Bonds from different issue months?

Yes, you can subscribe to multiple SSB issues from different months. However, total holdings across all issues cannot exceed SGD 200,000 per individual investor. This limit applies to the combined principal amount regardless of issue months held.

Are Singapore Savings Bonds subject to taxation?

Interest income from Singapore savings bonds is generally not subject to income tax for individual investors in Singapore. According to the Inland Revenue Authority of Singapore, interest from debt securities issued by the Singapore Government is tax-exempt. Consult with a tax professional for personalized guidance.

Conclusion

Singapore Savings Bonds represent a versatile tool for conservative investors seeking government-backed security combined with flexibility. The unique step-up interest structure rewards patient investors with increasing returns over time, while penalty-free redemption ensures you maintain capital access when circumstances change.

With minimum investments of just SGD 500 and full backing of Singapore's AAA-rated government, Singapore savings bonds provide an accessible entry point into fixed-income investing. Whether building an emergency fund, preserving capital during uncertain market conditions, or seeking stable returns as part of a diversified portfolio, SSBs offer a compelling combination of safety and practicality.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.