SRS Investment Options: Tax-Advantaged Funds Guide

Learn how to maximize your Supplementary Retirement Scheme savings through strategic investment in stocks, ETFs, bonds and REITs while enjoying significant tax advantages.

TL;DR: The Supplementary Retirement Scheme (SRS) offers Singapore investors tax-related features combined with flexible investment options. You can invest SRS funds in stocks, Exchange-Traded Funds (ETFs), Real Estate Investment Trusts (REITs), bonds, and unit trusts to grow your retirement savings. With uninvested SRS cash earning only 0.05% per annum, investing may help improve long-term outcomes to preserve purchasing power and build long-term wealth.

The Supplementary Retirement Scheme is one of several retirement savings options for Singaporeans, complementing the Central Provident Fund (CPF) with voluntary contributions that deliver immediate tax relief. However, many account holders miss a crucial opportunity by leaving their SRS funds uninvested. According to recent data from Singapore’s Ministry of Finance, approximately 19% of the SGD 20.58 billion in total SRS contributions remains uninvested, earning minimal returns while inflation erodes purchasing power.

Understanding your SRS investment options allows you to transform this tax-advantaged account into a strategic retirement portfolio. Whether you seek steady income through bonds and REITs or long-term growth through equities and ETFs, the scheme accommodates diverse investment strategies while providing tax-free growth until withdrawal.

Understanding the SRS Investment Framework

The Supplementary Retirement Scheme operates as a voluntary savings plan with tax incentives. Singapore Citizens and Permanent Residents can contribute up to SGD 15,300 annually, while foreigners enjoy a higher cap of SGD 35,700. These contributions provide dollar-for-dollar tax relief, reducing your taxable income by the contribution amount.

Investment returns, including dividends, interest, and capital gains, grow tax-free within your SRS account. According to IRAS, only 50% of withdrawals made at or after the statutory retirement age (currently 63, increasing to 64 from July 2026) become taxable income.

Why Active Investment Matters

Uninvested SRS funds earn only 0.05% interest per annum, falling significantly below inflation. Active SRS investment can be used as part of a long-term investment approach, with tax-free growth compounding over decades.

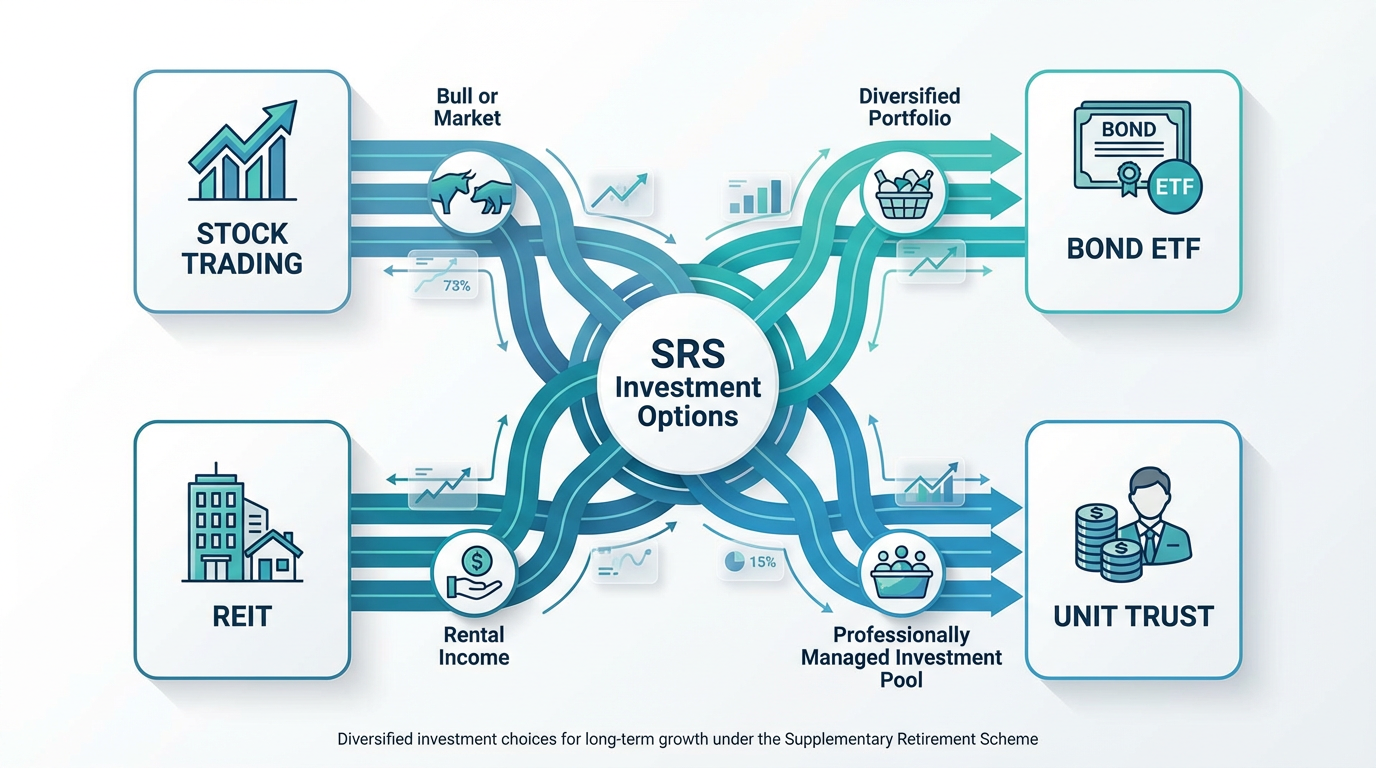

Main SRS Investment Options

The scheme permits investment across a broad range of financial instruments, though direct property purchases remain prohibited. You can invest through your SRS operator (DBS, OCBC, or UOB) or choose from other financial institutions offering SRS-compatible products.

Stocks and ETFs

Securities listed on the Singapore Exchange (SGX) represent popular SRS investment choices. You can invest in individual stocks ranging from blue-chip companies with established dividend records to growth-oriented businesses. This category accounted for approximately 24% of all SRS investments as of recent data.

Exchange-Traded Funds provide diversified market exposure through a single investment. Most SGX-listed ETFs qualify for SRS investment, particularly those denominated in Singapore dollars or offering Singapore dollar trading currency. The investment products available at Longbridge include stocks and ETFs across Singapore and United States markets, giving you comprehensive market access for your retirement portfolio.

Popular ETF choices include index-tracking funds that follow the Straits Times Index (STI), such as the SPDR STI ETF and Nikko AM Singapore STI ETF. These provide broad market exposure without requiring individual stock selection.

Bonds and Fixed Income

Bond investments offer conservative growth with regular income. Singapore Government Securities (SGS), including SGS Bonds, Treasury Bills, and Singapore Savings Bonds (SSB), provide government-backed stability. Bond ETFs like the ABF Singapore Bond Index Fund and Amova SGD Investment Grade Corporate Bond Index ETF offer diversified fixed-income exposure with varying yield profiles.

Real Estate Investment Trusts

Approximately 40 REITs trade on the SGX, providing exposure to income-generating real estate across various sectors including retail, industrial, hospitality, and healthcare properties. REITs typically distribute higher yields compared to many other investment categories, making them attractive for income-focused investors.

An important consideration: REIT distributions from SRS investments flow back into your SRS account rather than providing liquid cash. This characteristic makes REITs suitable for long-term accumulation strategies where reinvesting distributions enhances compounding effects.

Unit Trusts and Managed Funds

Unit trusts provide professional fund management across various asset classes, allowing access to specialized investment approaches without extensive market knowledge. Insurance-linked investment products combine growth potential with protection features but require careful evaluation of fees and commitment periods.

Tax Benefits of SRS Investment

The tax advantages inherent in SRS accounts may enhance long-term returns compared to taxable investment accounts. Understanding these benefits helps you maximize the scheme's value.

Contribution Tax Relief

SRS contributions reduce your taxable income dollar-for-dollar, up to the annual contribution limits. For example, someone in the 11.5% tax bracket contributing the maximum SGD 15,300, this translates to SGD 1,759.50 in immediate tax savings. Higher earners in the 22% bracket would save SGD 3,366 annually.

To claim tax relief for the Year of Assessment 2026, you must make contributions by 31 December 2025. The relief appears automatically when you file your income tax return, subject to the overall personal relief cap of SGD 80,000 that applies to all combined tax reliefs.

Tax-Free Growth

Investment returns within your SRS account accumulate without annual tax obligations. Dividends, interest, and capital gains compound tax-free, which may provide advantages compared to taxable accounts where annual taxes reduce reinvestment amounts.

Withdrawal Taxation

At statutory retirement age or later, only 50% of your SRS withdrawals become taxable at your prevailing income tax rate. This favorable treatment effectively halves your tax obligation on retirement distributions.

You can withdraw SRS funds penalty-free over a 10-year period starting from your first withdrawal after reaching the statutory retirement age. Strategic withdrawal planning, such as spreading distributions across multiple years to manage tax brackets, can further minimize tax obligations.

Early withdrawals before the statutory retirement age face less favorable treatment. The full withdrawal amount becomes taxable, plus you incur a 5% penalty on the withdrawn amount. Certain exceptions apply for circumstances like terminal illness, bankruptcy, or death, where penalty-free early withdrawal is permitted.

Building Your SRS Investment Strategy

Effective SRS investing requires a strategic approach aligned with your retirement timeline, risk tolerance, and overall financial plan.

Asset Allocation Considerations

Your SRS account functions as one component within your broader retirement portfolio. Asset allocation approaches vary depending on individual circumstances such as investment horizon and risk tolerance, where younger investors might typically emphasize growth through equity ETFs and stocks, whereas those approaching retirement might typically benefit from conservative allocations with bonds and dividend-paying securities. The locked-in nature makes SRS suitable for higher-return strategies compared to liquid savings.

Diversification Across Asset Classes

Diversification reduces portfolio risk by spreading investments across different asset categories that respond differently to economic conditions. A balanced SRS portfolio might include:

-

Equity exposure through index ETFs or selected individual stocks for growth potential

-

Fixed income via bond ETFs or Singapore Savings Bonds for stability and regular income

-

Real estate through REITs providing property exposure and dividend income

-

International diversification through global or regional ETFs to reduce Singapore-specific risks

The specific allocation depends on your personal circumstances, but diversification principles apply regardless of your risk profile.

Regular Contribution and Investment

Consistent annual contributions maximize tax relief benefits while implementing dollar-cost averaging. Many investors contribute in December to claim tax relief, then deploy funds strategically over subsequent months.

Monitoring and Rebalancing

Your SRS investments require periodic review to ensure your allocation remains aligned with your objectives. Market movements cause portfolio drift, where some positions grow larger while others shrink relative to your target allocation.

Annual or semi-annual reviews allow you to track market performance and make necessary adjustments. Rebalancing involves selling portions of overweight positions and adding to underweight ones, maintaining your intended risk-return profile.

Practical Implementation Steps

Opening and Funding Your SRS Account

Open an SRS account with DBS, OCBC, or UOB using basic personal information and identification. Singapore Citizens and Permanent Residents can use SingPass for streamlined opening. Contribute anytime throughout the year via electronic transfer, though contributions must clear by 31 December for that year's tax relief.

Selecting Investment Products

After funding your account, evaluate investment products based on cost structure, historical performance, risk characteristics, and strategy alignment. Your SRS operator provides investment access, while third-party brokers may offer broader product ranges.

Avoiding Common Mistakes

Avoid leaving funds uninvested at 0.05% interest. Compare fees carefully, as costs compound over time. Maintain long-term perspective during market volatility, and diversify across asset classes to reduce concentration risk.

Frequently Asked Questions

What investment products qualify for SRS?

You can invest SRS funds in stocks listed on SGX, ETFs, REITs, bonds, Singapore Savings Bonds, Treasury Bills, unit trusts, insurance products, and fixed deposits. Direct property investment is not permitted. Check with your SRS operator or investment platform for their specific product offerings, as availability varies across providers.

Can I lose money in my SRS account?

Yes. Market-based investments fluctuate in value, and losses can occur especially over shorter periods. Diversification, appropriate asset allocation, and long-term perspective aligned with your retirement timeline help manage these risks.

How do I withdraw from my SRS account?

You can make penalty-free withdrawals starting at the statutory retirement age applicable when you made your first SRS contribution. The current statutory retirement age is 63, increasing to 64 from July 2026. Early withdrawals before this age incur a 5% penalty and full taxation on the withdrawn amount, except in cases of terminal illness, bankruptcy, or death. Penalty-free withdrawals occur over a 10-year period starting from your first withdrawal.

What happens to SRS investments if I leave Singapore?

You can withdraw SRS funds after account closure, though early withdrawal penalties and full taxation apply unless you have reached statutory retirement age. Tax treatment depends on your residency status at withdrawal.

Should I max out CPF or SRS first?

CPF provides guaranteed returns and housing benefits with limited investment choices, while SRS offers broader options with investment risk. Many investors contribute to both, using CPF for foundational savings and SRS for additional tax-advantaged investing.

Conclusion

The Supplementary Retirement Scheme provides Singapore investors with powerful tools for building retirement wealth through tax-advantaged investing. With annual contribution caps of SGD 15,300 for Citizens and Permanent Residents or SGD 35,700 for foreigners, the scheme delivers immediate tax relief while allowing investment returns to compound tax-free over decades.

Some investors choose to complement contributions with investment decisions. Strategic deployment across stocks, ETFs, bonds, and REITs transforms your account into a genuine retirement portfolio. The key lies in taking action: opening an account, making regular contributions, and actively investing those funds rather than leaving them idle at 0.05% interest.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.