Collar Strategy: Protecting Portfolios

Discover how the collar strategy combines protective puts and covered calls to shield your stock portfolio from losses while preserving growth potential.

TL;DR: The options collar strategy protects your stock portfolio by combining a protective put (downside protection) with a covered call (premium income). It creates a defined risk-reward range, limiting losses below the put strike while capping gains above the call strike—ideal for Singapore investors protecting unrealized gains during market volatility.

When you hold significant gains in a stock position, market volatility can threaten to erase those profits. Selling triggers tax implications and removes upside exposure. Doing nothing leaves you vulnerable. The options collar strategy offers a middle path, providing downside protection while maintaining stock ownership and preserving some upside potential.

For Singapore investors trading through platforms offering options on US markets, understanding the collar strategy adds valuable risk management capability. This approach combines protective puts and covered calls into a single position that limits both downside risk and upside potential within a defined range.

What Is an Options Collar?

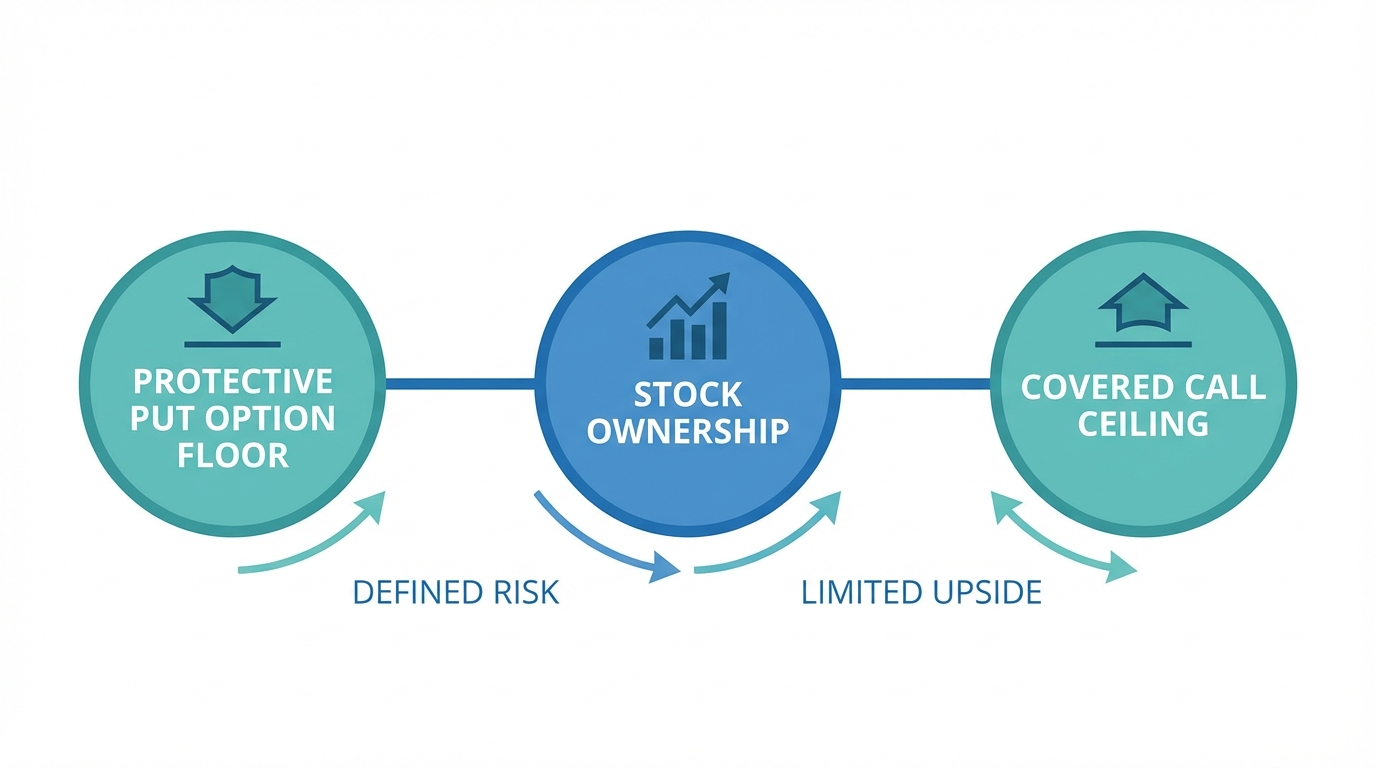

An options collar, also known as a hedge wrapper, consists of three components: owning shares of an underlying stock, buying an out-of-the-money (OTM) protective put option, and simultaneously selling an OTM covered call option. All positions are established on the same underlying stock, typically with options sharing the same expiration date.

The protective put creates a floor beneath your stock position, establishing a minimum sale price if the market moves against you. The covered call generates premium income that offsets the put cost, but establishes a ceiling capping potential gains if the stock rallies strongly.

The Zero-Cost Collar

A particularly attractive version is the zero-cost collar, where premium collected from selling the call exactly offsets the cost of buying the put. This establishes protection without upfront net cost, though you sacrifice upside potential above the call strike.

While achieving perfect zero cost requires precise strike selection, many investors accept a small net debit or credit to establish their desired protection and upside levels.

How the Collar Strategy Works

Understanding the mechanics helps you implement collars effectively. The strategy operates through three interacting components, each defining your overall risk-reward profile.

Building the Position

First, own shares of the underlying stock—typically in 100-share blocks since standard options contracts cover 100 shares. If you own 300 shares, construct three collar positions (buy three puts, sell three calls).

Next, buy OTM put options at a strike below your current stock price. This establishes downside protection. If your stock trades at $100, you might buy $95 strike puts, protecting against losses below that level (minus the collar's net cost).

Finally, sell OTM call options at a strike above current price. This generates premium but caps upside. Using the same example, you might sell $110 calls, giving up gains above that level while collecting premium reducing overall cost.

Example Scenario

Suppose you own US technology stock purchased at $80 that rallied to $120. You could implement a collar by:

Current stock price: $120

Buy protective put at $110 strike (protection floor)

Sell covered call at $135 strike (upside cap)

This collar ensures you can sell shares for at least $110, protecting most gains. If the stock rallies above $135, you must sell at that price.

Understanding the Risk-Reward Profile

The collar transforms your position from unlimited potential into a defined outcome range. This defined risk-reward profile is both the primary benefit and key tradeoff.

Maximum Risk and Reward

Maximum downside occurs if the stock falls below your protective put strike. You exercise the put and sell at the strike price, limiting loss. Actual loss equals the difference between current price and put strike, plus any net debit paid.

Maximum upside is capped at the covered call strike. If the stock rallies above that level, you must sell shares at the call strike through assignment. Profit equals the difference between current price and call strike, minus net debit (or plus net credit).

The range between these points represents where actual profit or loss falls at expiration, regardless of stock movement magnitude.

When to Use a Collar Strategy

The collar works for specific situations and market outlooks. Understanding alignment with your goals helps deploy it effectively.

Ideal Conditions

Collars work well when you hold concentrated positions with substantial unrealized gains and anticipate short to medium-term volatility. You want to maintain long-term positions but protect against near-term downside while markets stabilize.

This strategy makes sense when you cannot or do not want to sell due to tax considerations, company restrictions, or strong long-term conviction despite short-term concerns.

Unsuitable Situations

Avoid collars if you expect strong directional movement—capped upside means missing significant appreciation. The strategy makes little sense for small positions where options premiums and transaction costs consume too much potential return.

If strongly bearish, selling outright or buying protective puts without selling calls provides better alignment. The collar is fundamentally neutral to slightly bullish with defensive characteristics.

Implementing Collars for Singapore Investors

Singapore investors accessing US options markets through licensed brokers can implement collar strategies with attention to several operational details.

Strike Price Selection

Strike prices directly impact protection level, upside potential, and net cost. Wider collars (puts further OTM, calls closer) cost less but provide less protection and cap upside sooner. Tighter collars (puts closer to current price, calls further out) offer better protection and more upside room but cost more.

Common approaches involve selecting put strikes protecting original cost basis or preserving minimum acceptable profit. For calls, choose strikes representing target exit prices or levels where you would be comfortable selling anyway.

Expiration Timelines

Most collars use one to three-month expirations, balancing premium costs against desired protection periods. Shorter expirations require more frequent rolling but allow strike adjustments. Longer-dated collars reduce adjustment frequency but lock you into specific risk-reward ranges for extended periods.

Singapore Context

Singapore investors should note that capital gains from stock and options trading are generally not taxed for individuals, making collars attractive for protecting gains without immediate tax consequences. However, assignment on covered calls constitutes a sale event.

Advantages and Limitations

Every strategy involves tradeoffs. Understanding benefits and drawbacks helps you make informed decisions.

Key Benefits

The collar provides defined risk parameters from establishment. You know maximum downside and upside before entering, eliminating uncertainty from holding unhedged positions during volatility.

Premium income from covered calls helps offset or eliminate protective put costs, making downside protection affordable or generating net income in some configurations. This cost efficiency distinguishes collars from buying protective puts alone.

Maintaining share ownership means you continue receiving dividends during the collar period and can participate in upside moves within your defined range while deferring tax consequences from selling.

Notable Drawbacks

The most significant limitation is capped upside. If your stock experiences strong rallies, you miss gains above call strike price. This opportunity cost can be substantial in trending markets.

Transaction costs deserve consideration for Singapore investors trading US options. You establish two options positions and eventually close them or allow assignment, creating multiple transaction events.

Frequently Asked Questions

What is a collar in options trading?

A collar combines owning stock, buying a protective put option, and selling a covered call option. The put establishes a price floor protecting against losses, while the call generates income but caps upside potential above a certain level.

When should I use a collar strategy?

Use a collar when you hold significant unrealized gains and want short-term downside protection during uncertain markets. This works particularly well when you want to maintain ownership for tax or long-term reasons but need temporary risk management.

What is a zero-cost collar?

A zero-cost collar occurs when premium received from selling the covered call exactly equals the cost of buying the protective put, resulting in no upfront net cost. This is achieved by selecting strike prices where call premium offsets put cost.

Can I lose money with a collar strategy?

Yes, but losses are limited. If the stock declines below your protective put strike, maximum loss is the difference between entry price and put strike (plus any net cost to establish the collar). The collar prevents losses beyond this defined level.

How do I choose strike prices for a collar?

Select put strikes protecting your acceptable loss level—often original cost basis or minimum profit level. Choose call strikes representing target sale prices or upside levels you are willing to sacrifice. Balancing these determines protection cost and remaining upside.

What happens if my stock is called away?

If your stock rises above the call strike and you are assigned, you must sell shares at the strike price. This represents maximum profit from the collar. You realize gains up to the call strike but miss appreciation beyond that level.

Conclusion

The collar strategy provides structured portfolio protection during uncertainty while maintaining share ownership. By combining protective puts with covered calls, you create defined risk-reward parameters limiting downside exposure while preserving moderate upside potential.

This approach works for investors holding concentrated positions with significant unrealized gains who want temporary protection without triggering tax events or permanently exiting positions. Zero-cost or low-cost collars are particularly attractive when premium income substantially offsets protective put costs.

However, collars are not universally appropriate. Capped upside means underperformance in strong bull markets, and transaction costs can impact smaller position returns. Understanding when collar strategies align with your circumstances and outlook is essential.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.