Options Premium: How Pricing Works for Beginners

Discover how options premiums are priced, from intrinsic and extrinsic value to time decay and volatility. A comprehensive guide for beginner options traders.

TL;DR: The options premium is the price investors pay to buy an options contract. It consists of two parts: intrinsic value (how much the option is already in-the-money) and extrinsic value (time value and volatility). Understanding how these components work together helps investors make informed trading decisions.

Options trading offers flexibility and strategic opportunities, but understanding how options are priced can feel overwhelming for beginners. The options premium, which is the upfront cost investors pay to purchase an options contract, are influenced by multiple factors that interact in complex ways. Whether considering call options or put options, grasping the fundamentals of premium pricing will help investors evaluate whether an option represents the pricing structure and cost of an option.

This guide breaks down the essential concepts behind options premium pricing, from the basic components that make up the price to the market forces that cause premiums to fluctuate.

What Is an Options Premium?

An options premium is the market price investors pay to acquire an options contract. When buying an option, investors pay this premium upfront to the seller in exchange for the right (but not the obligation) to buy or sell the underlying asset at a predetermined strike price before or at expiration.

The premium is quoted on a per-share basis, but since each standard options contract represents 100 shares, investors multiply the quoted premium by 100 to determine the total cost. For example, if an option is quoted at a premium of USD 2.50, investors would pay USD 250 to purchase one contract.

This payment is non-refundable. Once investors purchase the option, the premium belongs to the seller regardless of whether investors eventually exercise the option or let it expire worthless. For options sellers, the premium represents income they collect in exchange for taking on the obligation to fulfil the contract if the buyer chooses to exercise it.

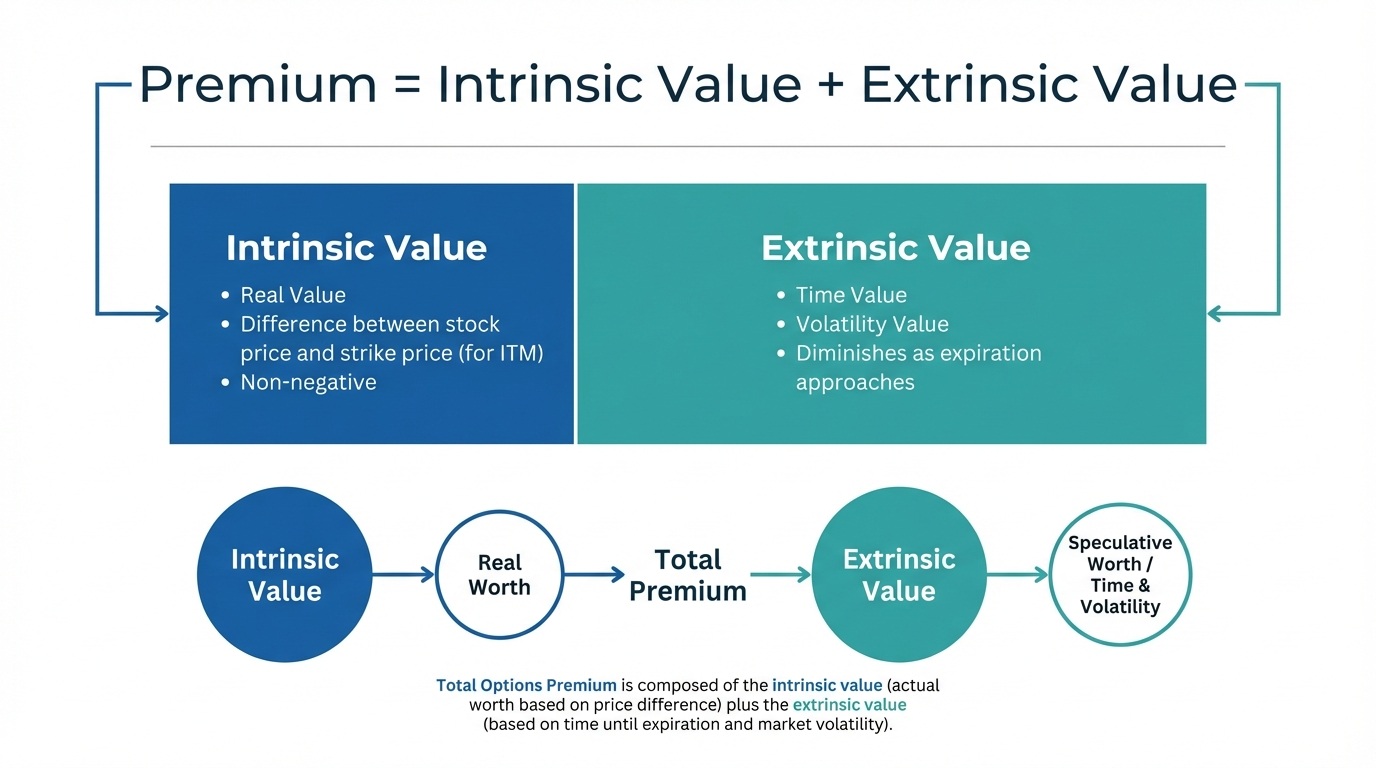

The Two Components of Options Premium

Every options premium can be broken down into two distinct parts: intrinsic value and extrinsic value. Understanding these components is essential for evaluating the pricing structure of an option.

Intrinsic Value

Intrinsic value represents the mathematical value that exists if the option were exercised immediately the. It reflects the tangible value of the option based purely on the relationship between the strike price and the current price of the underlying asset.

For call options, intrinsic value is calculated as:

Current Stock Price - Strike Price = Intrinsic Value

For an investor holding a call option with a USD 50 strike price and the stock is trading at USD 55, the intrinsic value is USD 5. For put options, the calculation reverses:

Strike Price - Current Stock Price = Intrinsic Value

Crucially, intrinsic value can never be negative. Options that are out-of-the-money have zero intrinsic value because exercising them would not generate any profit. Only in-the-money options possess intrinsic value.

Extrinsic Value (Time Value)

Extrinsic value, often called time value, represents the portion of the premium beyond intrinsic value. It reflects the option's potential to gain additional value before expiration, driven primarily by time remaining and market volatility.

The formula is straightforward:

Options Premium - Intrinsic Value = Extrinsic Value

Consider an option with a total premium of USD 6 and intrinsic value of USD 4. The remaining USD 2 represents extrinsic value—what traders are willing to pay for the possibility that the option could become more profitable before expiration.

All options carry some extrinsic value as long as time remains until expiration. Extrinsic value gradually diminishes as expiration approaches, a phenomenon known as time decay.

Key Factors That Affect Options Premium

Several interconnected factors influence how options are priced. Understanding these variables helps investors anticipate how premium values might change under different market conditions.

Underlying Asset Price Movement

The price of the underlying asset is the most direct influence on options premium. For call options, rising stock prices increase intrinsic value. Put options behave in the opposite manner—declining stock prices increase put option premiums, while rising prices reduce them.

Time Until Expiration

Time is a valuable asset in options trading. Options with longer expiration periods command higher premiums because they provide more opportunities for profitable price movements. A six-month option will typically cost more than a one-month option with the same strike price.

As expiration approaches, time value erodes. This time decay accelerates in the final weeks before expiration, particularly for at-the-money and out-of-the-money options.

Implied Volatility

Implied volatility measures the market's expectation of how much the underlying asset's price might fluctuate in the future. Higher implied volatility translates to higher options premiums across both calls and puts.

When traders expect significant price swings—perhaps due to an upcoming earnings announcement or economic event—implied volatility rises. This increases premiums because greater price movement creates more potential for options to increase in value.

Strike Price Proximity

The relationship between the strike price and the current stock price, known as "moneyness," strongly influences premium pricing. In-the-money options command higher premiums than at-the-money or out-of-the-money options. At-the-money options typically have the highest extrinsic value and are typically most sensitive to changes in time and volatility.

Understanding Time Decay (Theta)

Time decay, represented by the Greek letter theta, measures how much value an option loses each day as expiration approaches, assuming all other factors remain constant.

Theta is always negative for options buyers because time works against long positions. Every day that passes without favourable price movement results in lost premium value. This is particularly pronounced in the final 30 days before expiration, when time decay accelerates dramatically.

For options sellers, theta is positive. Sellers benefit from time decay because the premiums they collected diminish in value over time. Different options experience time decay at different rates—at-the-money options typically have the highest theta, meaning they lose time value most rapidly.

How to Calculate Options Premium

While sophisticated pricing models like Black-Scholes are used by professional traders, beginners can understand premium pricing through a simpler framework.

The basic formula remains:

Options Premium = Intrinsic Value + Extrinsic Value

To calculate intrinsic value, compare the strike price to the current stock price:

For calls: Intrinsic Value = Stock Price - Strike Price (if positive, otherwise zero)

For puts: Intrinsic Value = Strike Price - Stock Price (if positive, otherwise zero)

Practical Example

Suppose Stock A is trading at USD 100. Consider a call option with a USD 95 strike price that expires in three months. The option is quoted at a USD 7 premium.

Intrinsic value = USD 100 (current price) - USD 95 (strike price) = USD 5

Since the total premium is USD 7 and intrinsic value is USD 5, the extrinsic value = USD 7 - USD 5 = USD 2

If an investor purchase this option, your total cost would be USD 700 (USD 7 × 100 shares). To profit at expiration, Stock A would need to rise above USD 102 (the USD 95 strike price plus the USD 7 premium paid).

The Role of Options Greeks in Premium Pricing

Options Greeks are metrics that quantify how various factors affect options prices.

Delta measures how much an option's price changes when the underlying stock moves by USD 1. Theta represents time decay. Vega measures sensitivity to implied volatility changes. Gamma shows how much delta changes when the stock price moves.

Many trading platforms display Greeks alongside option quotes, making this information readily accessible.

Common Misconceptions About Options Premium

Higher premiums do not always mean better value. An expensive premium might reflect high intrinsic value or excessive extrinsic value that will quickly erode. Evaluate premiums in context of the option's components and the intended trading strategy.

Time decay does not affect all options equally. At-the-money options experience the fastest time decay, while deep in-the-money or far out-of-the-money options decay more slowly.

Investors may not recover the premium if investors sell the option later. There is no guarantee investors will recover the initial premium due to time decay, unfavourable price movement, or volatility changes.

Practical Considerations for Singapore Investors

When trading options from Singapore, currency fluctuations between Singapore dollars and United States dollars can impact the returns on US options.

Longbridge provides options trading access to US markets, allowing Singapore investors to participate in deep liquidity and diverse option chains. Since US options trade during American market hours (overnight in Singapore), platforms with reliable mobile access are essential for managing positions.

Strategies for Managing Premium Costs

Effect of expiration dates. Longer-dated options cost more but provide more time for the thesis to play out. Shorter-dated options are cheaper but require precise timing.

Strike price trade-offs. In-the-money options provide more intrinsic value but cost more. Out-of-the-money options are cheaper but require larger price movements to profit.

Implied volatility considerations. Avoid purchases when implied volatility is unusually high, as inflated premiums may work against investors if volatility normalizes.

Spread strategies mechanics. Vertical spreads involve simultaneously buying and selling options at different strike prices, reducing the net premium cost.

Frequently Asked Questions

What happens to the options premium if I do not exercise my option?

If investors choose not to exercise the option before expiration, investors lose the premium they paid. Options that expire out-of-the-money become worthless, and investors forfeit the entire premium.

Can options premium be higher than the stock price?

Yes, particularly for put options. If a stock is trading at USD 5, a put option with a USD 50 strike price could have a premium exceeding USD 45, reflecting substantial intrinsic value plus time value.

Why do some options have zero premium?

Options trade at or near zero when they are far out-of-the-money with little time remaining. If there is virtually no probability the option will finish in-the-money, market participants assign minimal value.

How do dividends affect options premium?

Expected dividend payments decrease call option premiums and increase put option premiums. This occurs because stock prices typically drop by the dividend amount on the ex-dividend date.

Conclusion

Understanding options premium pricing empowers you to make informed trading decisions. By recognizing how intrinsic value and extrinsic value combine to create total premium, you can evaluate whether an option's price reflects fair value.

The key factors—underlying price, time to expiration, implied volatility, and strike price—work together in dynamic ways. As you gain experience, you will develop intuition for what premium levels represent attractive opportunities for your strategy.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.