Protective Put Strategy: How to Insure Your Stock Portfolio

Discover how the protective put strategy acts as portfolio insurance, limitingyour downside risk while preserving unlimited upside potential when investing instocks.

TL;DR: A protective put strategy combines owning stock with buying a put option to limit downside risk while maintaining participation in potential stock gains. It functions like portfolio insurance, setting a floor price for your shares during periods of uncertainty.

Investing in stocks offers significant growth potential, but market volatility can expose your portfolio to unexpected losses. For investors who want to maintain their stock positions while managing downside risk, the protective put strategy offers a practical solution. This options-based approach acts as insurance for your holdings, allowing you to participate in potential gains while capping your maximum loss. Understanding how protective puts work can help you make more informed decisions about managing risk in your investment portfolio.

What Is a Protective Put Strategy

A protective put strategy involves holding a long position in a stock while simultaneously purchasing a put option on that same stock. The put option gives you the right, but not the obligation, to sell your shares at a predetermined price (the strike price) before the option expires.

Think of it like car insurance. You pay a premium to protect against potential damage, hoping you never need to use it. Similarly, with a protective put, you pay an option premium to establish a minimum selling price for your stock. If the stock price falls below the strike price, your put option gains value, offsetting your stock losses.

How the Mechanics Work

When you buy a put option, you enter a contract that allows you to sell 100 shares of stock at the strike price until the expiration date. Each options contract typically represents 100 shares, so one put option protects 100 shares of stock.

For example, if you own 100 shares of a stock trading at USD 100 and purchase a put option with a USD 95 strike price for USD 3 per share (USD 300 total), you establish a floor for your investment. If the stock drops to USD 80, you can exercise your put and sell at USD 95, limiting your loss rather than suffering the full decline.

Protective Put Versus Married Put

You may encounter the term "married put" when researching this strategy. The married put and protective put are essentially identical, differing only in timing. A married put refers to buying stock and put options simultaneously, while a protective put typically describes adding put protection to shares you already own. The risk management principle remains the same for both approaches.

Risk and Reward Profile

Understanding the profit and loss characteristics of protective puts helps you evaluate whether this strategy aligns with your investment goals.

Maximum Profit Potential

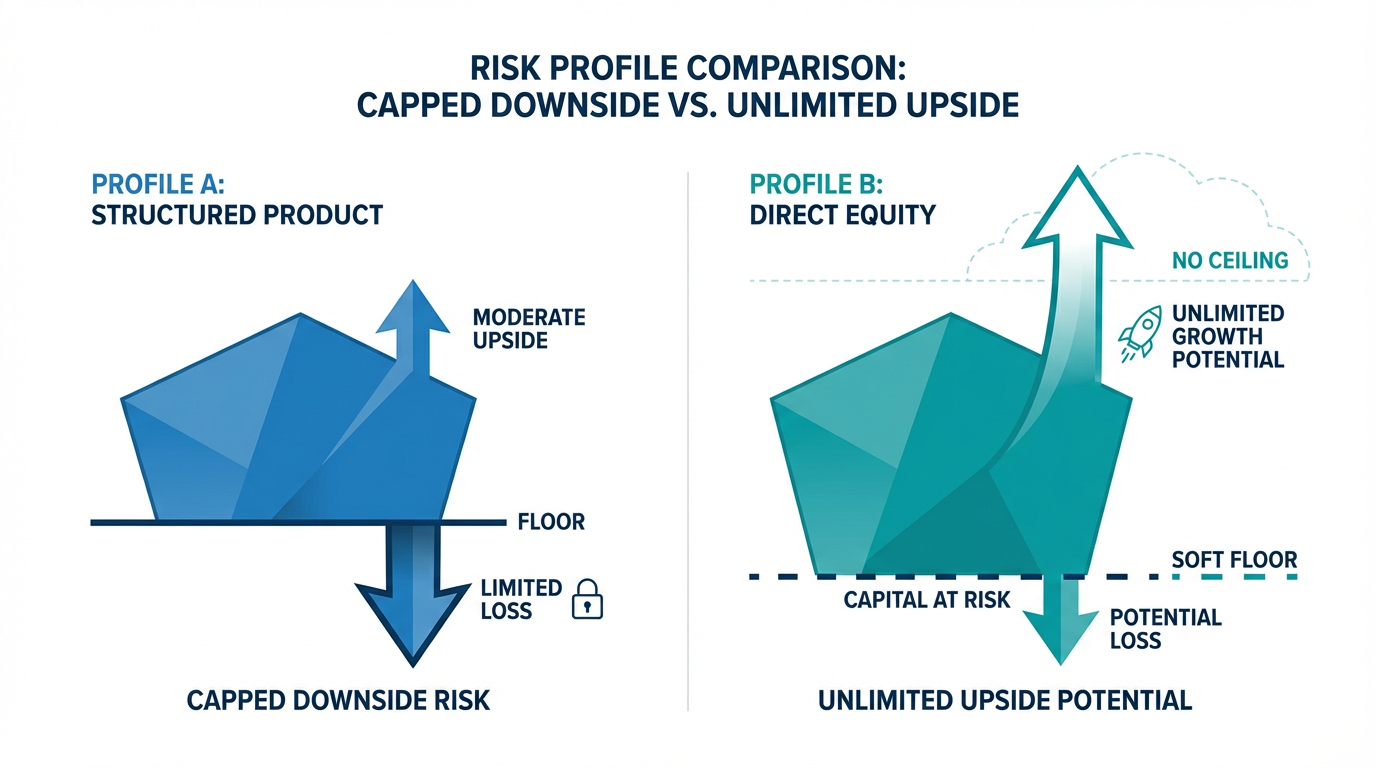

The upside potential of a protective put position is theoretically unlimited. If your stock price rises significantly, you benefit from those gains minus the cost of the put premium you paid. The put option simply expires worthless, and you keep all the stock appreciation above your cost basis.

Maximum Loss Calculation

Your downside risk is limited to a calculable amount. The maximum loss equals:

- Stock purchase price minus put strike price plus premium paid

For example, if you bought stock at USD 100, purchased a USD 95 strike put for USD 5, your maximum loss is USD 10 per share (100 - 95 + 5 = 10), regardless of how far the stock might fall.

Breakeven Point

Your breakeven point shifts higher when you add protective put coverage. Using the same example, if you paid USD 100 for the stock and USD 5 for the put, your cost basis becomes USD 105. The stock must trade above USD 105 for you to realize a profit on the combined position.

When to Consider Using Protective Puts

Protective puts work well in specific market situations where you want to maintain stock ownership while guarding against potential declines.

Ahead of Earnings Announcements

Company earnings reports can trigger significant stock price movements in either direction. If you hold shares of a company approaching earnings and feel uncertain about the outcome, a protective put allows you to participate in potential upside while limiting downside exposure if results disappoint.

Protecting Unrealized Gains

When a stock you own has appreciated substantially, you may want to lock in some of those gains without selling. A protective put establishes a minimum value for your position, allowing you to protect profits while remaining invested for potential additional growth.

Concentrated Stock Positions

If a single stock represents a large portion of your portfolio, protective puts can reduce concentration risk. This situation often arises with employee stock options or inherited shares where you may face restrictions on selling or prefer to maintain the position for tax reasons.

During Periods of Market Uncertainty

When broader market conditions create elevated volatility or uncertainty, protective puts offer a way to stay invested while managing downside risk. Rather than selling positions and potentially missing a recovery, you maintain exposure with defined risk parameters.

Protective Puts Versus Stop-Loss Orders

Investors often compare protective puts to stop-loss orders as risk management tools. Both aim to limit losses, but they work differently and produce different outcomes.

Advantages of Protective Puts

Stop-loss orders have a fundamental flaw: they trigger automatically when a stock hits the specified price, but the actual sale price may differ significantly during volatile trading. If bad news emerges overnight and a stock gaps down at the market open, your stop-loss may execute far below your intended exit price.

Protective puts provide more control. You have the right to sell at your strike price anytime before expiration, regardless of where the stock trades. If the stock drops sharply and then rebounds, you can choose whether to exercise the put or wait for further recovery.

Trade-offs to Consider

The main disadvantage of protective puts compared to stop-loss orders is cost. Stop-loss orders have no premium cost; you simply set the trigger price. Protective puts require paying a premium, which reduces your overall returns if the stock performs well or stays flat.

Time decay also affects protective puts. Options lose value as expiration approaches, so continuous protection requires purchasing new puts periodically, creating ongoing costs that can add up over time.

Costs and Considerations

Before implementing a protective put strategy, evaluate the cost implications and factor them into your investment decisions.

Premium Costs

The put option premium represents your maximum cost for the protection. Several factors influence premium pricing:

Time to expiration: Longer-dated options cost more than shorter-dated ones

Strike price selection: Puts with strike prices closer to the current stock price cost more

Implied volatility: Higher market volatility increases option premiums

Impact of Time Decay

Options are wasting assets, meaning they lose value as expiration approaches, all else being equal. This time decay, known as theta, works against protective put holders. If the stock price remains stable, your put will gradually decline in value until expiration.

Cost Reduction Strategies

To reduce protection costs, some investors implement a collar strategy by selling a call option above the current stock price while buying a protective put. The premium received from the call sale partially or fully offsets the put purchase cost. However, this approach caps your upside potential at the call strike price.

Getting Started with Protective Puts

If you decide protective puts fit your risk management needs, follow a structured approach to implementation.

Selecting Strike Prices

Choose a strike price that balances protection level against premium cost. At-the-money puts (strike price equal to current stock price) provide immediate protection but cost the most. Out-of-the-money puts (strike price below current stock price) cost less but allow for more initial downside before protection activates.

Consider how much decline you can tolerate before you want protection to engage. Many investors may consider strike prices 5% to 10% below the current stock price, depending on their risk tolerance.

Choosing Expiration Dates

Match your protection timeline to your investment outlook. If you want protection through an earnings announcement next month, a one-month put may suffice. For longer-term portfolio insurance, consider quarterly or longer-dated options, though be prepared for higher premium costs.

Position Sizing

Ensure you have the correct number of put contracts for your stock position. Since each contract covers 100 shares, divide your share count by 100 to determine contracts needed. Owning 300 shares requires three put contracts for full coverage.

For investors looking to explore options trading, Longbridge offers access to various investment products including options in the US market.

Frequently Asked Questions

What happens if my stock rises after buying a protective put?

If your stock price increases, you benefit from the appreciation minus the premium paid for the put. The put option expires worthless, and you keep all gains above your adjusted cost basis. This unlimited upside potential is a key advantage of the protective put strategy.

How is a protective put different from simply selling my stock?

Selling your stock eliminates downside risk but also removes any potential for gains. A protective put lets you maintain ownership and participate in potential upside while setting a floor on losses. Additionally, selling may trigger capital gains taxes, while protective puts allow you to defer that tax event.

Can I lose the entire premium paid for a protective put?

Yes. If the stock price stays above the strike price through expiration, the put expires worthless and you lose the entire premium paid. However, in this scenario, your stock position has performed well, and the premium represents the cost of insurance you did not need to use.

Conclusion

The protective put strategy offers investors a methodical approach to managing portfolio risk without sacrificing growth potential. By combining stock ownership with put option protection, you create a position with defined downside limits and unlimited upside opportunity. While the premium cost reduces overall returns when protection proves unnecessary, many investors find this trade-off worthwhile during uncertain market conditions or when protecting significant gains.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.