Calendar Spreads: Time-Based Options Strategy

Calendar spreads let you profit from time decay by selling short-term options while buying longer-dated ones. Learn setup, risk management, and ideal market conditions.

TL;DR: A calendar spread is an options strategy where you sell a near-term option and buy a longer-dated option at the same strike price. This neutral strategy profits from faster time decay in the short-term option and benefits from rising implied volatility, with risk limited to the initial cost.

Options strategies offer diverse approaches to navigate market conditions, and the calendar spread stands out as a time-based method that capitalizes on how options lose value differently based on their expiration dates. Also known as a time spread or horizontal spread, an options calendar spread involves selling a short-term option while simultaneously buying a longer-term option of the same type (call or put) at the same strike price. This strategy appeals to investors who anticipate minimal price movement and want to profit from the accelerating time decay that affects near-term options more dramatically than longer-dated ones.

Understanding calendar spreads requires familiarity with how options pricing works, particularly the relationship between time decay and implied volatility (IV). When executed properly, this strategy can generate returns in sideways markets where directional strategies might struggle.

What Is a Calendar Spread?

A calendar spread is constructed by selling an option with a near-term expiration while simultaneously purchasing an option with a longer expiration date. Both options share the same strike price and are of the same type, meaning you create a call calendar spread using two call options or a put calendar spread using two put options.

The strategy's name derives from the use of different calendar dates for the two option contracts. Some traders also refer to it as a horizontal spread because, on an options chain display, different expiration dates appear horizontally across the screen.

Structure and Cost

Calendar spreads are net debit trades, meaning you pay to enter the position. The cost reflects the difference between the premium you pay for the longer-dated option and the premium you collect from selling the shorter-dated option. Since longer-dated options have more time value, they cost more than near-term options, resulting in a net outflow when opening the position.

This initial debit represents the maximum risk for the trade. Unlike undefined-risk strategies, you cannot lose more than you invest, which makes calendar spreads appealing to risk-conscious traders.

Call vs Put Calendar Spreads

While the mechanics are similar, choosing between calls and puts depends on your market outlook:

-

Call calendar spreads typically work best when the strike is at or slightly above the current stock price, positioning the trade with a neutral to slightly bullish bias

-

Put calendar spreads are often used when the strike is at or slightly below the current price, creating a neutral to slightly bearish stance

Both versions profit from the same fundamental principles: differential time decay and volatility changes.

How Calendar Spreads Generate Profits

Calendar spreads make money through two primary mechanisms that work in your favour when market conditions align properly.

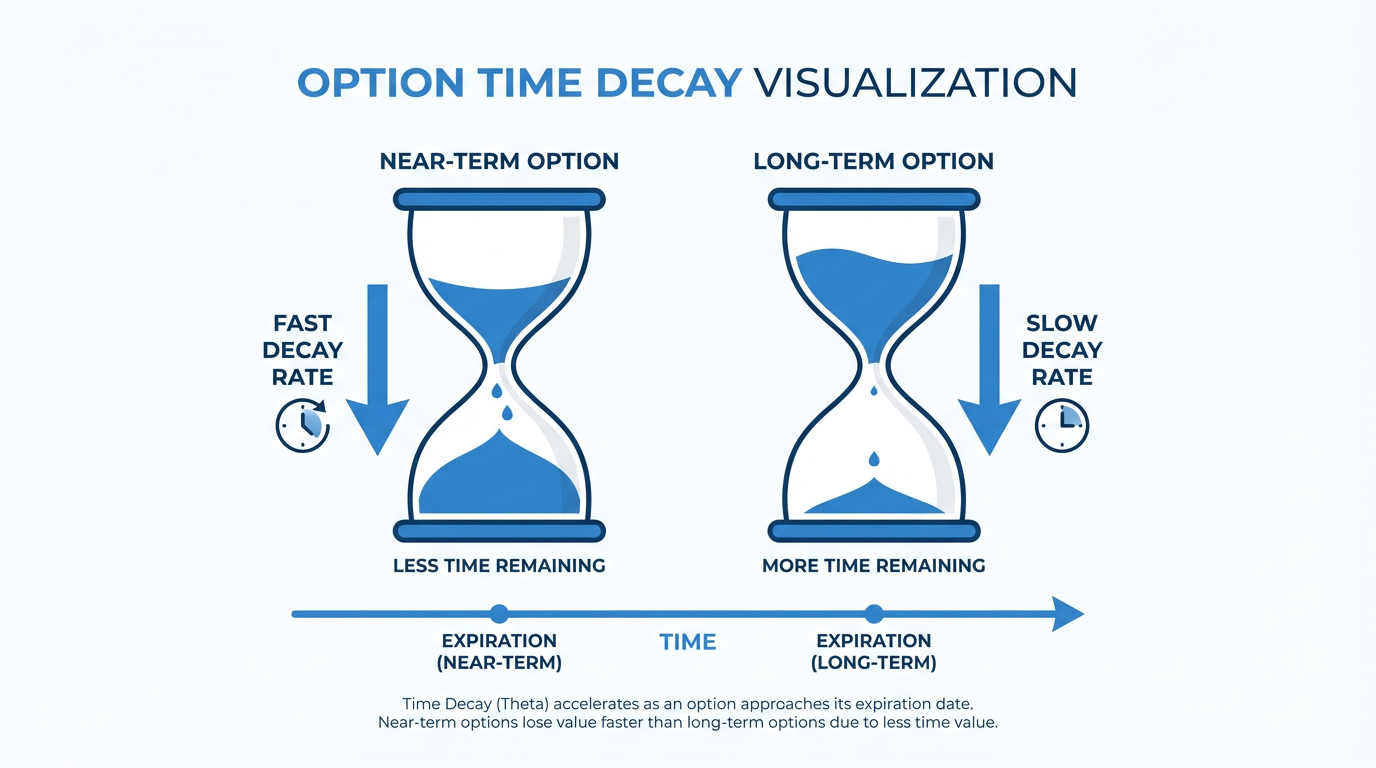

Time Decay Differential

Time decay, measured by the Greek letter theta, accelerates as options approach expiration. This acceleration is not linear but exponential, meaning an option with seven days to expiration loses value much faster than one with thirty-five days remaining.

In a calendar spread, you benefit from this differential. The short-term option you sold decays rapidly, losing value each day. Meanwhile, the longer-dated option you bought decays much more slowly. If the underlying stock price remains near your strike price, the short option can expire worthless (which is what you want, since you sold it), while the long option retains substantial value.

Implied Volatility Expansion

The second profit driver involves changes in implied volatility. Options with more time until expiration have higher vega, meaning they are more sensitive to changes in IV.

When IV rises across the market or for your specific underlying asset, the longer-dated option you own increases in value more than the shorter-dated option you sold. This creates a profit even if time decay has not fully played out yet.

Calendar spreads perform particularly well when initiated during periods of low IV with the expectation that volatility will increase.

Ideal Market Conditions

Calendar spreads are not all-weather strategies. They thrive in specific market environments and struggle in others.

Range-Bound Markets

The strategy performs optimally when the underlying asset trades sideways and remains close to your chosen strike price. Large price movements in either direction can hurt the position because both options will move away from their optimal profit zone.

Low to Rising Volatility

Entering calendar spreads when implied volatility is relatively low provides the best risk-reward setup. Low IV means you pay less for the longer-dated option, reducing the net debit.

When volatility subsequently rises, the longer-dated option gains value disproportionately due to its higher vega, while the short-term option's value increase is limited by its approaching expiration.

Time Until Expiration

Most traders structure calendar spreads with the short option expiring within two to six weeks and the long option expiring one to three months later. This timeframe provides sufficient differential in time decay rates while keeping both legs liquid and manageable.

Risk Management and Position Sizing

While calendar spreads offer defined risk, proper position management remains essential to long-term success.

Maximum Loss Scenarios

Your maximum loss equals the net debit paid to establish the position. This occurs if both options expire worthless when the stock moves far from your strike price. Most traders exit when the position has lost thirty to fifty percent of its value.

Profit Potential and Targets

Maximum profit occurs when the stock price equals your strike price at short option expiration, with the short option expiring worthless while the long option retains maximum time value. Traders may typically target returns of twenty-five to fifty percent of the net debit paid.

Assignment Risk

If you sell call options in a calendar spread and the stock moves above your strike price, assignment is possible. Assignment means the option buyer exercises their right to buy shares from you at the strike price.

To mitigate assignment risk, many experienced traders use index options with European-style settlement, which cannot be exercised early. Alternatively, closely monitor short options that move in the money and consider closing or rolling the position before assignment occurs.

Getting Started with Calendar Spreads

Implementing calendar spreads requires access to a platform that supports multi-leg options trading and provides clear visibility into Greeks and pricing.

Selecting the Underlying Asset

Choose stocks or ETFs with relatively stable price action and liquid options markets. High liquidity ensures tighter bid-ask spreads, reducing transaction costs. Assets with moderate implied volatility work best.

Strike Price Selection

Place the strike price at or near the current stock price for a neutral setup. You can adjust based on directional bias: strikes above current price are slightly bullish, while strikes below are slightly bearish.

Expiration Dates and Execution

Select a short option expiring in thirty to forty-five days and a long option expiring sixty to ninety days later. Execute as a single spread order to ensure proper fill pricing and reduce execution risk.

Adjustments and Exit Strategies

Active management distinguishes successful calendar spread trading from passive position holding.

Rolling the Short Option

When the short option approaches expiration and the trade is profitable, roll it forward by buying back the current option and selling a new one with a later expiration. This allows you to collect additional premium.

Managing Price Movement and Profits

When the stock moves away from your strike, you can close the position, roll to a new strike, or convert to a vertical spread. Many traders target returns of twenty-five to fifty percent of the net debit paid rather than holding for maximum profit.

Common Mistakes to Avoid

Even experienced options traders can stumble with calendar spreads if they overlook key considerations.

Key Mistakes

Avoid entering when implied volatility is elevated, as this increases cost and exposes you to contraction risk. Choose strikes at or near the current price rather than far out of the money. Focus on liquid options with tight bid-ask spreads and adequate open interest. Be cautious holding through earnings, as large price moves can hurt the position.

Frequently Asked Questions

What happens if the stock moves significantly before expiration?

Large price movements generally hurt calendar spreads because both options move away from the optimal profit zone. If the stock moves substantially, consider closing the position to limit losses or rolling the strike prices to better align with the new price level. Maximum loss is still limited to your initial debit.

Can I use calendar spreads with weekly options?

Yes, weekly options work for the short leg, providing more frequent premium collection opportunities. However, they may have wider bid-ask spreads and lower liquidity than monthly options.

How do dividends affect calendar spreads?

If the underlying stock pays a dividend while you have a short call option in the money, early assignment risk increases. Monitor ex-dividend dates and consider closing or rolling short call positions before these dates if the calls are in the money.

Are calendar spreads suitable for beginners?

Calendar spreads are intermediate-level strategies requiring understanding of time decay, implied volatility, and options Greeks. Master basic options concepts first before attempting this strategy.

How much capital do I need for calendar spreads?

Capital requirements equal the net debit paid, typically ranging from USD fifty to several hundred dollars depending on the underlying asset and expiration dates.

Conclusion

Calendar spreads are a type of strategic approach to options trading that leverages time decay differentials and volatility dynamics rather than relying solely on directional price movement. By selling short-term options while owning longer-dated contracts, traders can profit in range-bound markets where traditional directional strategies struggle. The defined-risk profile makes this strategy accessible for risk-conscious investors, while the multiple profit drivers provide opportunities across various market conditions.

Success with calendar spreads requires understanding when to enter positions, how to manage them actively, and when to take profits or cut losses. Execution typically involves considering liquid underlying assets, entering during low implied volatility periods, and maintaining realistic profit expectations.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.