Naked Options Risk: What Every Investor Should Know

Naked options carry uncapped loss potential. Learn how they work, why therisks are significant, and which safer alternatives — covered calls, cash-securedputs, and credit spreads — may better suit your investment strategy.

TL;DR: Naked options (also called uncovered options) involve selling options contracts without owning the underlying asset, exposing the seller to theoretically uncapped losses if the market moves against them. This article explains the key risks clearly and outlines safer structured alternatives such as covered calls and credit spreads that may better suit most retail investors.

Options trading offers genuine flexibility for investors, but not all strategies carry equal risk. Among the more aggressive approaches is writing naked options — selling an option contract without owning the underlying stock or holding cash reserves to cover a potential assignment. For investors exploring options in the US market, understanding naked options risk is essential before committing any capital. This article breaks down how naked options work, why the risks are significant, and which alternative strategies can help you pursue premium income while keeping your downside clearly defined.

What Are Naked Options?

An option contract gives the buyer the right — but not the obligation — to buy (call) or sell (put) a specified stock at an agreed price (the strike price) before a set expiry date. When you sell an options contract, you collect a premium upfront.

A naked option, also known as an uncovered option, is when you sell that contract without having either:

The underlying shares in your account (for a naked call), or

Cash reserved to cover the purchase obligation (for a naked put)

Because the exposure is unhedged, the position is described as "naked" or uncovered.

Naked Calls vs Naked Puts

Naked calls involve selling a call option without owning the underlying shares. If the stock rises sharply and the buyer exercises the option, you are obligated to sell shares you don't own — meaning you'd need to buy them on the open market at whatever the current price happens to be.

Naked puts involve selling a put option without holding cash to cover a potential purchase. If the stock drops and the buyer exercises the option, you must buy shares at the strike price regardless of how far the market price has fallen.

Both types carry substantial downside, but naked calls are generally viewed as more dangerous because share prices can, in theory, rise without limit.

The Key Risks of Naked Options

Understanding naked options risk means examining both the mechanics and the real-world scenarios where things go wrong.

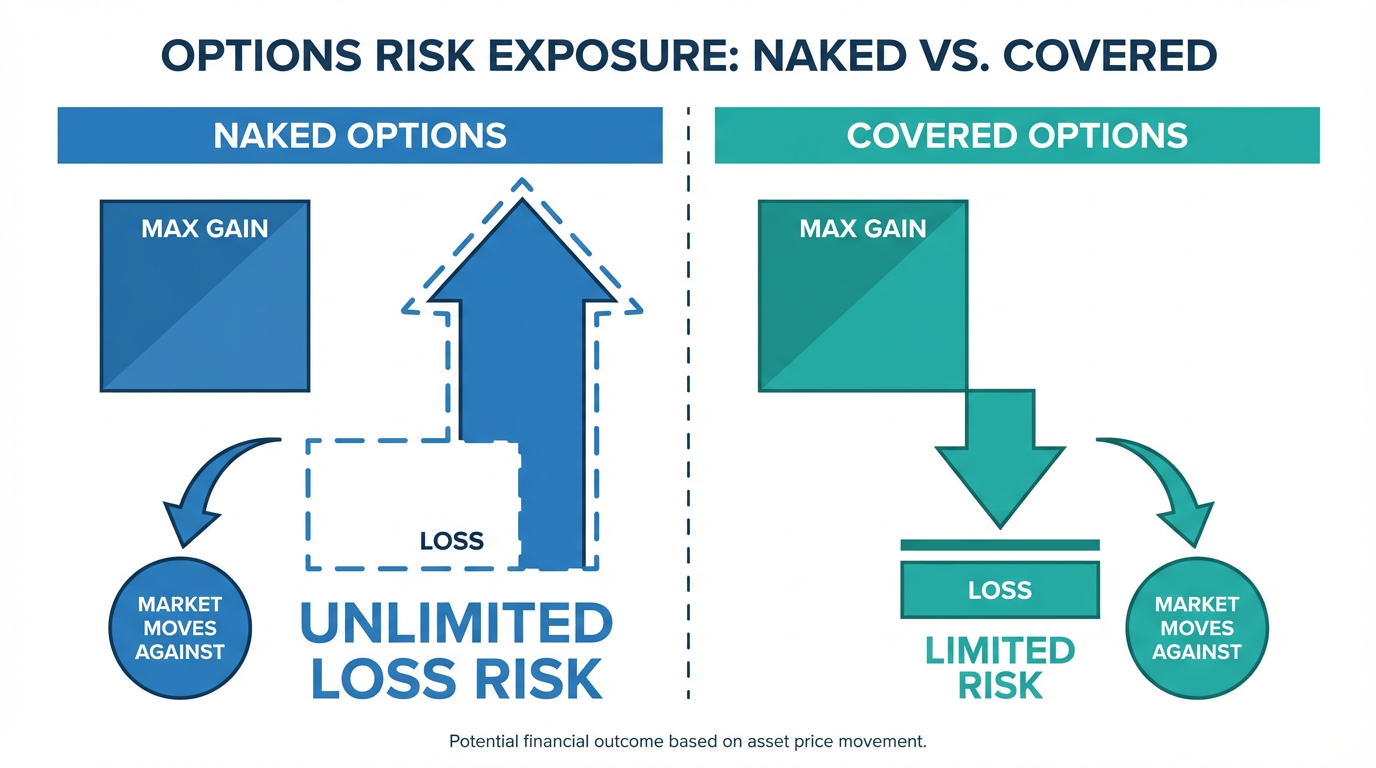

Unlimited Loss Potential (Naked Calls)

The defining characteristic of a naked call position is that losses are, in theory, uncapped. If you sell a naked call at a USD 50 strike price and the stock surges to USD 120 before expiry, you must still deliver shares at USD 50 — meaning you would need to buy at USD 120 and sell at USD 50, resulting in a USD 70 per share loss multiplied by the number of contracts written. (This example is for illustration purposes only and does not constitute investment advice.)

This asymmetry is stark: your maximum gain is the premium collected, while your maximum loss is unbounded.

Significant Risk with Naked Puts

While naked puts do not carry technically uncapped risk (since a stock can only fall to zero), the losses can still be severe. During the March 2020 market downturn, the S&P 500 fell approximately 30% in 22 trading days. Traders who were short naked puts during that period faced margin calls and were forced to buy shares at prices far above market value.

Margin Requirements and Capital Tie-Up

Brokers require naked options sellers to maintain a margin account with sufficient funds to cover a potential adverse move. According to the U.S. Securities and Exchange Commission (SEC), naked call writing is generally permitted only for investors with the highest options trading approval levels. These margin requirements are substantial and can tie up capital that could otherwise be deployed elsewhere.

Important: Margin requirements for naked options are typically much higher than for covered positions, because the broker must protect against the risk of uncapped losses.

Volatility Spikes Amplify Losses

Options pricing is heavily influenced by implied volatility — a measure of the market's expectation of future price swings. During market stress events such as sudden earnings surprises or broad sell-offs, volatility spikes sharply. This causes option prices to soar, meaning that even if the underlying stock hasn't moved significantly yet, the mark-to-market loss on a naked position can grow rapidly before you have time to close it.

Assignment Risk

American-style options — the type commonly traded on US equity markets — can be exercised at any point before expiry, not just on the final day. A naked options seller therefore faces assignment risk throughout the life of the contract, particularly when the position moves deeply in the money or near an ex-dividend date.

Who Typically Uses Naked Options?

Despite the risks, some experienced traders write naked options for specific reasons. Selling naked puts, for instance, can express a bullish view on a stock while collecting premium — effectively getting paid to wait for an entry price you already want. Naked calls may be used when a trader has high conviction that a stock will stay range-bound. In both cases, the appeal is capital efficiency: premium income without tying up shares or large cash reserves.

That said, most brokers restrict naked options writing to clients who meet the highest options trading approval thresholds, typically requiring demonstrated experience and a minimum portfolio size. For most retail investors, the asymmetric risk-reward profile — where the maximum gain is a fixed premium but the maximum loss is theoretically uncapped — does not align with sound risk management principles. The strategies in the next section offer ways to pursue similar income with clearly defined downside.

Safer Alternatives to Naked Options

Several alternatives allow investors to pursue option premium income while keeping their downside clearly defined.

Covered Calls

A covered call involves selling a call option on a stock you already own. Because you hold the underlying shares, the worst-case outcome is that your shares get called away at the strike price — a scenario you can evaluate before entering the trade.

Maximum gain: Premium collected, plus any share appreciation up to the strike price

Maximum loss: Cost of your shares minus the premium received

Covered calls are widely regarded as a conservative income-generating strategy and are often the first options strategy approved for retail accounts.

Cash-Secured Puts

A cash-secured put means selling a put option while holding enough cash to purchase the underlying shares if assignment occurs. Unlike a naked put, the cash is reserved, eliminating margin shortfall risk.

Maximum gain: Premium collected (if the stock stays above the strike price)

Maximum loss: The difference between the strike price and zero, minus the premium received — a defined and pre-planned exposure

This strategy suits investors willing to own a stock at a lower price while collecting a premium in the meantime.

Credit Spreads

A credit spread involves simultaneously selling one option and buying another on the same underlying asset, with the same expiry but a different strike price. This combination caps your maximum loss at the difference between the two strikes.

Call credit spread (bear call spread): Sell a call at a lower strike, buy a call at a higher strike. Profits if the stock stays below the lower strike.

Put credit spread (bull put spread): Sell a put at a higher strike, buy a put at a lower strike. Profits if the stock stays above the higher strike.

Credit spreads are popular precisely because the risk is defined at the moment of entry. Converting a naked option into a spread by purchasing an offsetting contract caps the maximum loss, at the cost of a slightly reduced premium. You can learn more about options strategies through the Longbridge Academy.

Long Options (Buying Calls or Puts)

Buying call or put options gives you fully defined risk: your maximum loss is limited to the premium paid, nothing more. While the probability of profit may be lower than selling options, the transparent risk profile makes this approach suitable for investors who are still building their options knowledge.

You can explore the full range of investment products available on Longbridge's investment products page.

Key Principles for Managing Options Risk

Whichever approach you choose, sound risk management is essential:

Define your risk before entering any position. Never take on more potential loss than you can genuinely absorb.

Maintain adequate buying power. Overextending your account leaves little room to manage positions if they move against you.

Understand assignment mechanics. Know exactly what happens to your account if the option is exercised before you sell it.

Monitor positions around earnings and market events. Volatility can increase rapidly around corporate announcements.

Stay informed. For broader market context, Longbridge News provides regular updates.

Frequently Asked Questions

What is the main difference between a naked option and a covered option?

A naked (uncovered) option is sold without the seller owning the underlying asset or reserving cash to cover the obligation. A covered option involves either owning the underlying shares (covered call) or holding sufficient cash (cash-secured put). Covered positions have clearly defined, limited risk; naked positions do not.

Can retail investors in Singapore trade naked options?

Options trading on US market securities is available through licensed brokers such as Longbridge, regulated by the Monetary Authority of Singapore (MAS). However, naked options writing typically requires the highest level of options trading approval, given the significant risk involved. Retail investors should carefully review eligibility requirements and assess whether their experience and risk tolerance align with such strategies.

Is it possible to turn a naked option into a safer position?

Yes. If you have already sold a naked option, you can convert it into a credit spread by purchasing an offsetting option at a different strike price. This caps your maximum loss, though it reduces the premium income retained.

Why do some traders still use naked options despite the risks?

Experienced traders sometimes write naked options in low-volatility environments, confident a stock will remain within a certain range. The appeal is premium income and capital efficiency. However, this strategy demands disciplined position sizing and active monitoring, and is not generally appropriate for most retail investors.

Conclusion

Naked options can appear attractive because of the premium income they generate, but the risk profile is fundamentally asymmetric: the maximum gain is capped at the premium received, while the potential loss is theoretically uncapped for naked calls. For most investors building options knowledge in the US market, strategies with defined risk — covered calls, cash-secured puts, and credit spreads — offer a more balanced approach.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. It is essential to fully understand each strategy's mechanics, risk characteristics, and execution rules before trading, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.