Options Greeks: Delta, Gamma, Theta for Beginners

Discover how options Greeks—Delta, Gamma, and Theta—help you measure risk and make informed trading decisions. Clear explanations with practical examples for beginners.

TL;DR: Options Greeks—Delta, Gamma, and Theta—are essential risk measurement tools that help you understand how option prices respond to market changes. Delta tracks price sensitivity, Gamma measures Delta's rate of change, and Theta quantifies time decay. Mastering these fundamentals empowers you to make informed trading decisions and manage risk effectively.

Options trading can feel overwhelming when you first encounter terms like Delta, Gamma, and Theta. These measurements, collectively known as options Greeks, aren't just academic concepts—they're practical tools that reveal how your options positions will respond to changing market conditions. Whether you're exploring options trading on platforms that offer multi-market access or just starting to understand derivatives, grasping these Greeks is your first step toward confident, informed decision-making.

Think of options Greeks as your trading dashboard. Just as a car's dashboard shows speed, fuel level, and engine temperature, Greeks show you how your option's value will change based on price movements, time passing, and volatility shifts. This guide breaks down the three most important Greeks—Delta, Gamma, and Theta—in plain language, so you can apply them immediately to your trading strategy.

What Are Options Greeks and Why Do They Matter?

Options Greeks are mathematical calculations that measure different dimensions of risk in an options contract. According to research from leading options education platforms, these metrics help traders quantify the theoretical impact of various market factors on option prices.

The term "Greeks" comes from the Greek letters used to represent these measurements. While there are five primary Greeks (Delta, Gamma, Theta, Vega, and Rho), beginners should focus on the first three, as they have the most immediate and visible impact on daily trading decisions.

Greeks serve critical functions including risk assessment, position management, strategy selection, and portfolio protection. Thoroughly understand them, and combine this with a comprehensive options trading terms to build a solid foundation. Make them transforms options from mysterious instruments into manageable, strategic tools.

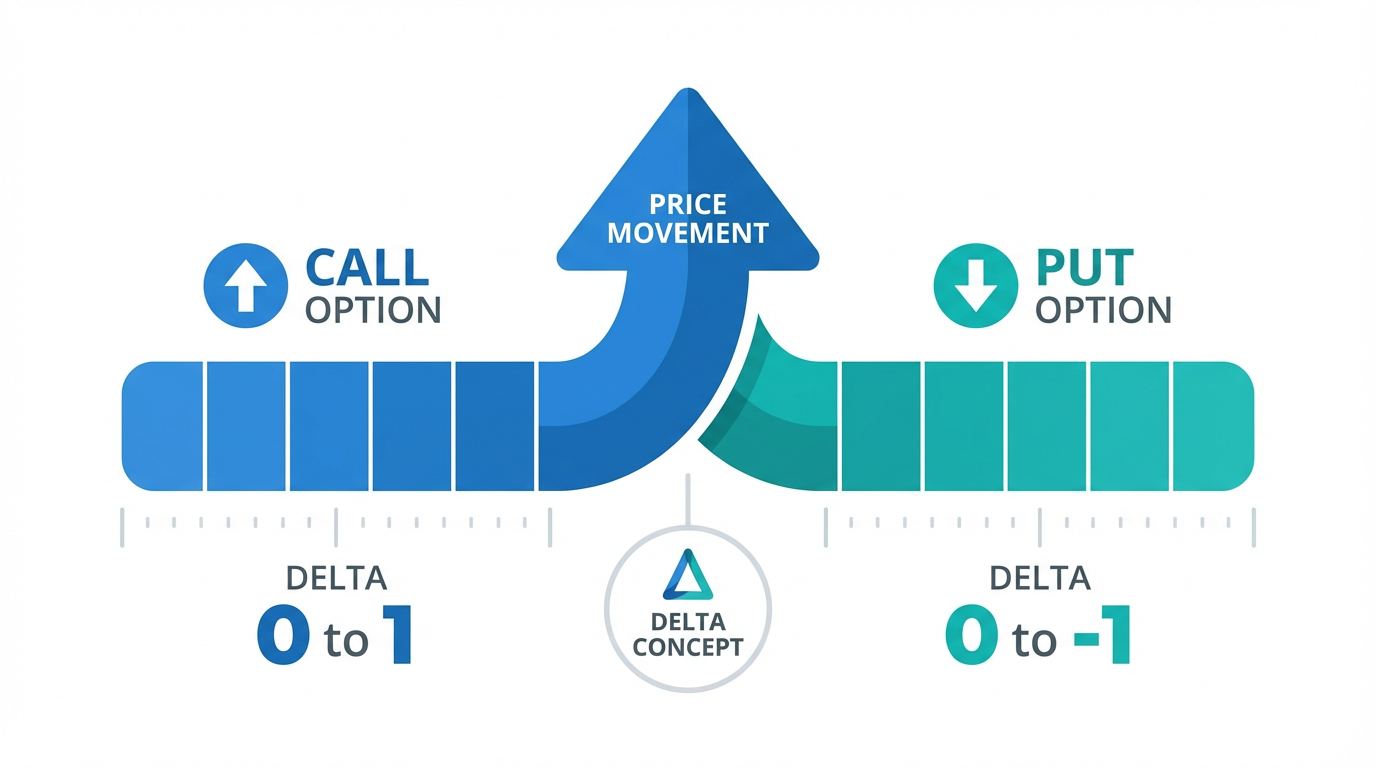

Delta: Understanding Price Sensitivity

Delta measures how much an option's price will theoretically change for every one-dollar move in the underlying asset's price. It's the most fundamental Greek and the first one most traders learn.

How Delta Works

Call options have a positive Delta ranging from 0 to 1, while put options have a negative Delta ranging from 0 to -1. A call option with a Delta of 0.50 means the option price should theoretically increase by fifty cents if the stock rises by one dollar.

Beyond price sensitivity, Delta also provides a rough estimate of the probability that an option will expire in-the-money (ITM). An option with a Delta of 0.70 has approximately a 70% chance of expiring in-the-money.

Delta in Different Scenarios

At-the-money (ATM) options: Delta typically sits around 0.50 for calls and -0.50 for puts

In-the-money (ITM) options: Delta approaches 1 for calls and -1 for puts

Out-of-the-money (OTM) options: Delta approaches 0, reflecting lower price sensitivity

For traders using platforms like Longbridge that provide options trading in US markets, understanding Delta helps you select strike prices that align with your directional bias and risk tolerance.

Gamma: The Rate of Change

If Delta is the speedometer showing how fast your option price moves, Gamma is the accelerator showing how quickly that speed changes. Gamma measures the rate of change in Delta for every one-dollar move in the underlying asset.

Why Gamma Matters

Gamma is crucial because Delta isn't static—it changes as the stock price moves. A high Gamma means your Delta will change rapidly, making your position more dynamic and potentially more profitable (or risky).

Gamma Characteristics

Always positive: Both calls and puts have positive Gamma

Highest for ATM options: Options near the current stock price have the highest Gamma

Increases near expiration: Short-term options have higher Gamma than long-term options

Practical Gamma Example

Imagine an investor owns a call option with Delta of 0.50 and Gamma of 0.10. If the stock rises by one dollar, the option price increases by fifty cents and the new Delta becomes 0.60. If the stock rises another dollar, the option now gains sixty cents instead of fifty cents. This acceleration effect makes Gamma particularly important for active traders.

High Gamma positions can work in your favour when the market moves your way, but they can also create rapid losses when the market moves against you. Traders often monitor their portfolio's total Gamma exposure, especially approaching expiration when Gamma accelerates.

Theta: Understanding Time Decay

Theta quantifies how much value your option loses each day as expiration approaches, assuming all other factors remain constant. This phenomenon is called time decay, and it's one of the most predictable aspects of options trading.

How Theta Works

Theta is expressed as a negative number for long options positions (both calls and puts), indicating that the option loses value each day. For example, a Theta of -0.05 means your option will theoretically lose five cents in value each day, all else being equal.

Theta Across Different Timeframes

Time decay isn't linear—it accelerates as expiration approaches. Long-term options experience slow time decay, while short-term options (30-45 days or less) see rapid acceleration. According to options education resources, the final 30 days before expiration see the steepest time decay, which is why many option sellers prefer strategies focused on this period.

ATM options experience the highest absolute Theta decay, while OTM options have high Theta relative to their price, losing value percentage-wise faster.

Working With and Against Theta

Theta creates a fundamental dynamic: option buyers fight against time decay, needing the underlying asset to move enough to overcome it, while option sellers benefit from Theta, collecting premium as time passes.

Understanding Theta helps you select appropriate expiration dates. If you expect a move within a week, buying a three-month option wastes premium. Conversely, if your thesis requires time to play out, selecting an option with only two weeks to expiration sets you up to fight steep time decay.

How Delta, Gamma, and Theta Work Together

These three Greeks interact in ways that shape your options positions. Gamma determines how quickly your Delta changes, meaning high Gamma can rapidly transform a neutral position into a highly directional one. Higher Delta options (closer to the money) also have higher absolute Theta, creating a trade-off: options with greater price sensitivity lose more value to time decay.

As expiration approaches, both Theta and Gamma accelerate for ATM options, creating heightened risk and opportunity where small price movements can generate outsized gains or losses.

Practical Application: Choosing the Right Options

Understanding Greeks transforms theoretical knowledge into practical decision-making. Here's how to apply this knowledge when selecting options:

For Directional Trades

If investors expect movement within days or weeks, investors seeking directional exposure often look for higher Delta options (e.g., 0.60 or above), while accepting higher Theta if they're confident in timing, and monitor Gamma to understand how their Delta will change.

For Longer-Term Positions

For longer-term views, investors might consider options with longer expirations (e.g., 60-90 days) to mitigate Theta impact and consider slightly OTM strikes to reduce cost while maintaining reasonable Delta.

For Income Strategies

Income-focused strategies often involve selling options with higher Theta to benefit from time decay collection while being aware of Gamma risk, especially near expiration.

Common Mistakes Beginners Make With Greeks

New traders often focus exclusively on Delta and directional movement, forgetting that Theta works against them daily. An option can move in your predicted direction but still lose money if the move doesn't overcome time decay.

Short-term options can experience dramatic Delta swings due to high Gamma near expiration. What starts as a moderately directional position can become extremely directional (or worthless) within hours.

Remember that Greeks provide theoretical estimates based on mathematical models, not guarantees. Actual price movements can differ due to volatility changes, liquidity factors, and other market dynamics.

Tools and Resources for Tracking Greeks

Online trading platforms display Greeks for each option contract, making this information readily accessible. When evaluating market data and option chains, pay attention to how Greeks change across different strike prices and expiration dates. Many platforms also offer position-level Greek calculations, showing your total portfolio Delta, Gamma, and Theta.

For those serious about options education, exploring Longbridge Academy can deepen your understanding of how Greeks interact with different strategies.

Frequently Asked Questions

What is the most important Greek for beginners?

Delta is typically the most important Greek for beginners because it directly shows how much your option price will change when the stock moves. It's the most intuitive to understand and has the most immediate impact on your position's profitability. Once you're comfortable with Delta, adding Theta and Gamma to your analysis creates a more complete risk picture.

How often do Greeks change?

Greeks change continuously as market conditions shift. Delta changes with every stock price movement (measured by Gamma), Theta decreases predictably each day, and all Greeks are affected by changes in volatility and time to expiration. Most trading platforms update Greeks in real-time during market hours.

Can I trade options successfully without understanding Greeks?

While technically possible, trading options without understanding Greeks significantly increases your risk of unexpected losses. Greeks help you anticipate how positions will behave, allowing you to make informed decisions about entries, exits, and position sizing. Successful long-term options trading requires at least basic Greek literacy.

Do I need to calculate Greeks myself?

No, all modern trading platforms calculate and display Greeks automatically for each option contract. Your job is to interpret these values and understand what they mean for your positions, not to perform the underlying mathematical calculations, which are based on complex models like Black-Scholes.

How do Greeks help with risk management?

Greeks quantify specific risks in measurable terms. Delta shows your directional exposure, helping you understand potential losses if the market moves against you. Theta shows how much you'll lose to time decay each day, helping you determine if your timeframe is realistic. Gamma reveals how stable your position is, alerting you to potential rapid changes in risk exposure.

Conclusion

Mastering options Greeks—Delta, Gamma, and Theta—transforms you from a speculative trader into an informed strategist. Delta reveals your price sensitivity, Gamma shows how dynamic your position is, and Theta quantifies the cost of holding your position over time.

Greeks are tools, not guarantees. They provide theoretical estimates helping you make informed decisions about position selection, timing, and risk management. As you develop your options trading skills, continuously monitor these Greeks alongside your market analysis. With practice, interpreting Greeks becomes second nature.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.