Options Position Sizing: Kelly Criterion Explained

The Kelly Criterion is a mathematical framework for options position sizing. Learn how to use win rate and reward-to-risk ratio to size trades with discipline.

TL;DR: The Kelly Criterion is a mathematical formula that helps options traders calculate the ideal percentage of capital to allocate per trade, based on win rate and reward-to-risk ratio. Using fractional Kelly (half or quarter of the full formula output) is widely recommended to balance growth potential with manageable risk. When applied correctly, it replaces guesswork in options position sizing with a disciplined, probability-driven framework.

Options trading rewards those who manage risk systematically. Yet one of the most overlooked decisions is how much capital to commit to each trade. Allocate too little and your returns remain modest; allocate too much and a single loss can significantly damage your portfolio. Options position sizing is the bridge between a good trading idea and sustainable long-term performance, and the Kelly Criterion offers a mathematically grounded approach. Developed by John Kelly Jr. at Bell Labs in 1956, it was later adapted by investors and traders to determine optimal capital allocation per trade.

What Is the Kelly Criterion?

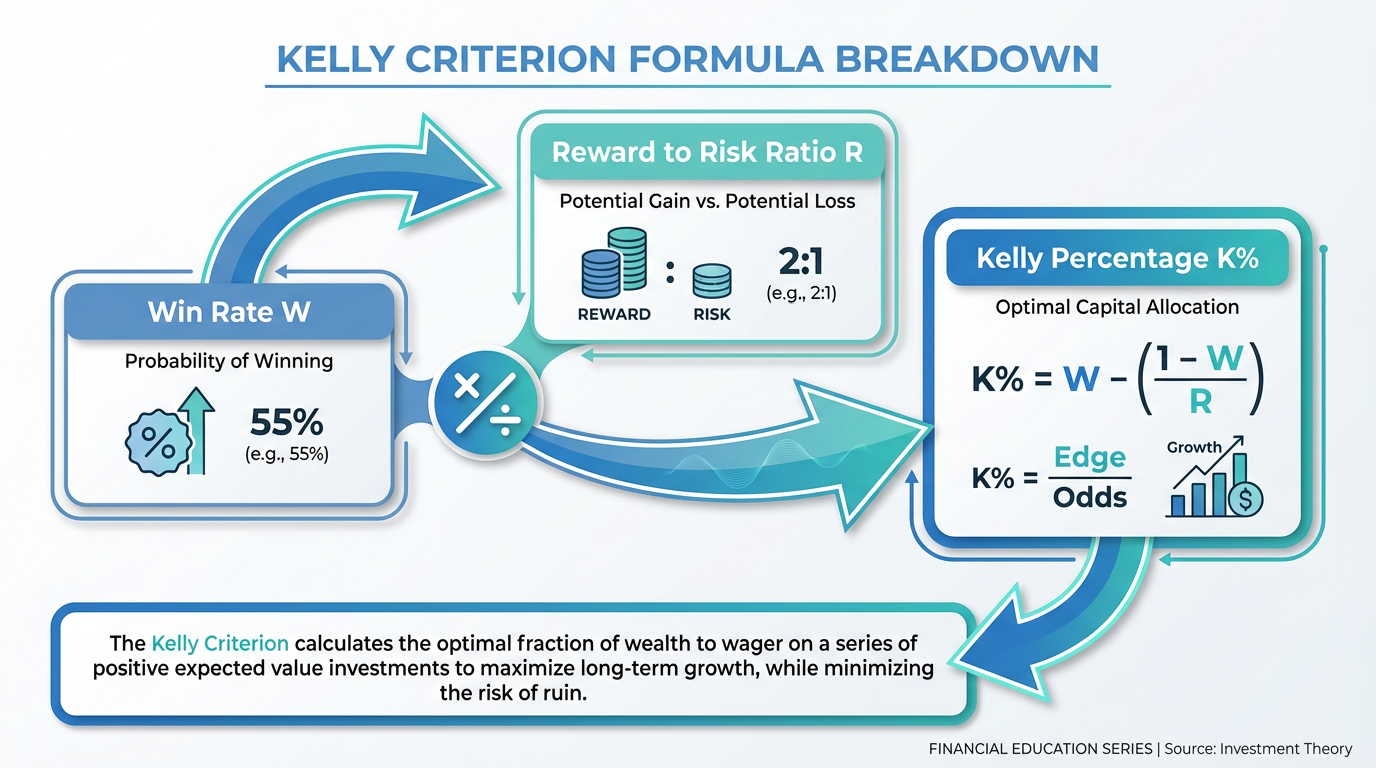

The Kelly Criterion is a formula that calculates the fraction of your total capital to allocate to a single trade. It is grounded in probability theory and designed to maximize long-term portfolio growth by sizing positions according to your statistical edge.

The formula is:

Kelly % = W − (1 − W) / R

Where:

-

W = Win rate (the probability that a trade will be profitable, expressed as a decimal)

-

R = Win/loss ratio (total value of winning trades divided by total value of losing trades)

The output, the Kelly percentage, tells you what proportion of your total portfolio to put into a given trade. If the result is negative, the formula signals there is no statistical edge, and the trade should be avoided.

An Example Calculation

Suppose your historical trading data shows a 55% win rate on your options trades, and your average winning trade returns 1.5 times what you lose on average losing trades. The Kelly Criterion gives:

Kelly % = 0.55 − (1 − 0.55) / 1.5 = 0.55 − 0.30 = 0.25, or 25%

This would imply a theoretical allocation of 25% based on the formula output. However, as discussed below, most traders apply a fractional version of this figure in practice.

Why This Formula Matters for Options Traders

Options involve leverage, time decay, and shifting probabilities. These features make position sizing more consequential than in straightforward stock trades. A position that is too large relative to your account can cause significant damage from a single adverse move, especially with strategies that carry uncapped or defined risk. The Kelly Criterion provides a principled framework to calibrate that exposure.

Applying the Kelly Criterion to Options Trades

Applying the Kelly Criterion to options requires a few adaptations, since options have unique characteristics compared to straightforward stock positions.

Using Delta as a Probability Proxy

In options trading, the delta of an option indicates how much its price is expected to move for each USD 1 move in the underlying asset. Conveniently, delta also serves as a rough proxy for the probability that an option will expire in the money (profitable at expiration).

For example, a call option with a delta of 0.40 has approximately a 40% probability of expiring in the money. This figure can be used as the win rate (W) in the Kelly formula. While delta is an approximation rather than a precise probability, it provides a practical starting point for calculations, particularly for traders who do not have extensive personal trade history to draw on.

Adjusting for Multi-Leg Strategies

Options strategies often involve multiple legs, such as vertical spreads, iron condors, and strangles. Calculate the net result across all legs to arrive at a combined outcome. The credit received or debit paid affects your break-even threshold and actual win/loss ratio. Evaluate the trade as a whole rather than each leg in isolation.

Using Historical Trade Data

Past trade logs are the most reliable source of Kelly inputs. Review at least 30 to 50 completed trades to calculate your actual win rate and average win-to-loss ratio. The more data you have, the more accurate your Kelly percentage will be. You can track market performance and conditions using Longbridge's market data services.

Full Kelly vs. Fractional Kelly: A Practical Decision

The full Kelly percentage, calculated directly from the formula, is mathematically designed to maximize the long-term growth rate of your capital. However, using the full Kelly recommendation comes with significant practical drawbacks.

Full Kelly is aggressive. Any overestimation of your win rate or reward ratio, even a small one, can result in a position that is far too large. The formula is sensitive to input accuracy, and errors compound quickly. Real markets introduce slippage, changing volatility, and execution gaps that probability models do not capture.

The Case for Half Kelly and Quarter Kelly

In practice, some traders use a fraction of the Kelly output: half-Kelly (50% of the calculated figure) or quarter-Kelly (25%). This sacrifices some theoretical maximum growth but produces smoother portfolio performance and reduces the risk of large drawdowns.

In the earlier example, full Kelly suggests 25% of capital; half-Kelly recommends 12.5%; quarter-Kelly recommends 6.25%. The smaller fractions align more closely with the risk tolerance of most retail investors.

Tip: Some traders choose to apply additional caps, such as limiting individual positions to a small percentage of total portfolio value, typically around 2% to 5%, regardless of what the Kelly formula outputs. This acts as an additional safety net beyond the formula itself.

Limitations of the Kelly Criterion

The Kelly Criterion is powerful, but applying it effectively requires awareness of its constraints.

Inputs Must Be Reliable

The formula is only as good as the data behind it. Overstating your win rate by a few percentage points can lead to meaningfully oversized positions. Traders with a short trade history may not have enough data for reliable Kelly inputs.

Markets Are Not Static

Win rates and win/loss ratios change as conditions evolve. A strategy that performed well in low-volatility periods may produce different results during market stress. Regular recalculation of your Kelly inputs is essential.

Kelly Does Not Select Trades

The formula tells you how much to risk, not which trades to take. It must be paired with a sound method for identifying setups and managing individual trade risk. The Longbridge Academy offers educational resources on options strategies and risk management.

Concentration Risk

Kelly treats each trade as independent. In practice, positions on correlated assets can move together. Sizing positions individually without accounting for correlation may create unintended portfolio-level concentration.

An Example of A Practical Framework for Applying Kelly to Options

Here is an example step-by-step process for incorporating Kelly into your options position sizing:

-

Review your trade history. Calculate your win rate and average win/loss ratio from at least 30 completed trades.

-

Apply the formula. Use Kelly % = W − (1 − W) / R to calculate the suggested allocation.

-

Use a fractional modifier. Multiply the result by 0.5 (half-Kelly) or 0.25 (quarter-Kelly).

-

Set an absolute cap. Define a maximum position size, for instance, 5% of total portfolio value. Never exceed this regardless of Kelly output.

-

Recalculate periodically. Update inputs every 20 to 30 trades or after significant strategy changes.

-

Skip negative Kelly trades. A negative result signals the trade lacks a positive expected value.

Explore the full range of investment products available, including US options, through the Longbridge products overview page.

How Kelly Compares to Other Position Sizing Methods

Several position sizing methods exist. Fixed fractional sizing risks a constant percentage (commonly 1% to 2%) on every trade regardless of edge, which is simpler but treats all setups equally. Fixed dollar sizing commits a set amount per trade and is easy to apply, but it does not scale with account growth or strategy quality. Volatility-adjusted sizing, using the Average True Range (ATR), sizes positions based on recent price movement to normalise risk across trades.

The Kelly Criterion stands apart by mathematically optimising for long-term compounding growth, provided inputs are reliable. Fractional Kelly combines this rigour with practical downside protection, making it a widely adopted approach among quantitative and systematic traders.

Frequently Asked Questions

What is the Kelly Criterion in simple terms?

The Kelly Criterion is a formula that calculates what percentage of your capital to risk on a trade based on how often you win and how much you win relative to what you lose. A higher win rate or better win/loss ratio increases the recommended allocation.

Is the Kelly Criterion suitable for beginners?

It is most useful for traders with a documented track record and enough trades to calculate reliable win rates. Beginners are often better served starting with simple fixed-fraction rules, such as risking 1% to 2% per trade, until they have built sufficient data.

What happens if my Kelly Criterion result is negative?

A negative result means the trade does not have a positive expected value based on your historical data. The correct action is to skip the trade. This is the formula's way of signalling there is no statistical edge with your current strategy parameters.

How often should I recalculate my Kelly inputs?

Recalculate your win rate and win/loss ratio every 20 to 30 trades, or after any significant change in your trading approach, market conditions, or the options strategies you use.

Can I use the Kelly Criterion for options spreads?

Yes, but account for the full trade outcome across all legs. For credit spreads, maximum profit is the premium received and maximum loss is the spread width minus the premium. Use those figures for the win/loss ratio alongside your historical win rate for that specific strategy.

Conclusion

Options position sizing is a consequential, and often underestimated, factor in long-term trading outcomes. The Kelly Criterion offers a mathematically grounded approach for deciding how much capital to allocate per trade, moving position sizing decisions from intuition to probability-based discipline.

In practice, fractional Kelly, either half or quarter of the formula output, is the recommended approach for most retail traders. It preserves the formula's logic while accounting for the uncertainty of real-world trading, where probability estimates are never perfectly precise.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.