Options Strangle Strategy: Lower Cost Volatility Trading

The options strangle strategy offers a cost-effective way to trade volatility by buying or selling out-of-the-money calls and puts with different strike prices.

TL;DR: The options strangle strategy involves buying or selling an out-of-the-money call and put simultaneously with the same expiration but different strike prices. This approach costs less than a straddle while enabling traders to profit from significant price movements (long strangle) or stable markets (short strangle).

Market volatility creates both opportunity and uncertainty. When you anticipate major price movements but cannot predict direction, or when you expect stability in turbulent times, the options strangle offers a flexible approach. Unlike a straddle that requires both options at the same strike price, a strangle uses different strikes, reducing your upfront cost while requiring larger price swings for profitability.

Understanding the options strangle helps investors learn how this strategy may be used to respond to uncertain market conditions. This guide explains both long and short strangle approaches, their risk profiles, and practical implementation considerations for Singapore investors trading US market options.

What is an Options Strangle?

An options strangle is a multi-leg strategy involving simultaneous purchase or sale of a call and put option on the same asset with the same expiration date but different strike prices. Both options are typically out-of-the-money (OTM), meaning the call strike sits above the current market price while the put strike sits below.

A long strangle involves purchasing both options to profit from substantial price movement in either direction. A short strangle involves selling both options to collect premium when you expect the asset to remain relatively stable.

The cost advantage over straddles represents the primary appeal. Since OTM options carry lower premiums than at-the-money options, strangles require less capital. However, the underlying asset must move further before reaching profitability. Strike price selection significantly influences costs and breakeven thresholds.

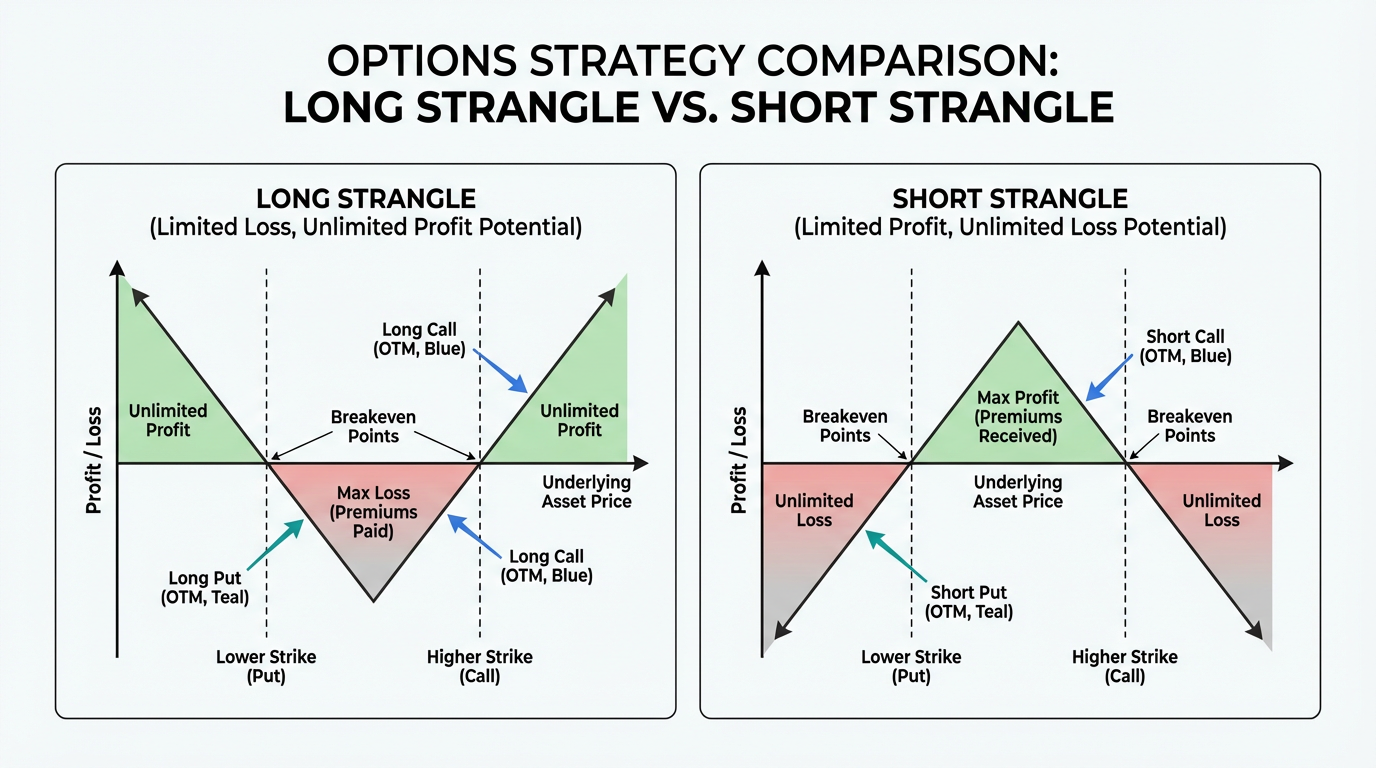

Long Strangle Strategy

A long strangle positions you to profit from significant volatility when you anticipate a major price move but lack certainty about direction. This proves particularly valuable before earnings announcements, regulatory decisions, or major economic releases.

To establish a long strangle, you simultaneously purchase an OTM call and put with identical expiration dates. For example, if Stock A trades at USD 50, you might buy a USD 55 call and USD 45 put. Your maximum loss equals the total premium paid, occurring if the stock remains between strikes at expiration.

Profit potential is unlimited upward and substantial downward. If Stock A surges to USD 65, your call gains USD 10 in intrinsic value. If it drops to USD 35, your put gains USD 10.

Long Strangles: Optimal Conditions

This strategy performs best when implied volatility is low relative to expected future movement. Purchasing when volatility is depressed improves potential returns when actual volatility materializes. The strategy typically suits situations where catalysts could trigger movement but direction remains unclear, such as regulatory approvals or quarterly earnings.

Maximum risk stays capped at premiums paid. However, the underlying must move beyond breakeven points: call strike plus total premium (upper) or put strike minus total premium (lower). Time decay accelerates in the final 30 days before expiration.

Short Strangle Strategy

A short strangle profits from stability rather than movement. By selling OTM options, you collect premium upfront and benefit when the underlying remains range-bound through expiration.

To implement, simultaneously sell an OTM call and put with the same expiration. Using Stock A at USD 50, you might sell the USD 55 call and USD 45 put, immediately receiving premium representing your maximum profit. Profit materializes if Stock A stays between USD 45 and USD 55 at expiration.

Short Strangles: Optimal Conditions

This strategy performs best in high implied volatility environments. When volatility spikes, option premiums inflate, enabling traders to capture elevated premium that cushions against adverse moves. Short strangles typically align with neutral outlooks when analysis suggests consolidation or calm trading.

You keep the premium collected if both options expire worthless, creating high profit probability. However, losses become unlimited upward if the stock surges past your call strike, and substantial downward if it collapses below your put strike. A single adverse move can erase profits from multiple successful trades, demanding rigorous risk management.

Strangle vs Straddle: Key Differences

Understanding how strangles compare to straddles helps you select the appropriate strategy. Both aim to profit from volatility, but their structural differences create distinct tradeoffs.

A straddle uses at-the-money options with identical strikes, while a strangle employs OTM options with different strikes. This fundamental difference drives the cost variation. Straddles require higher premium since at-the-money options carry more value, while strangles cost less due to OTM positioning.

The breakeven points differ accordingly. Straddles need smaller price movements to reach profitability since both options start with some intrinsic value. Strangles require larger moves to overcome the wider strike spread and premium paid. For example, a straddle might become profitable with a 5% move, while a comparable strangle needs 8% or more.

Probability of profit shifts between the two strategies. Straddles offer higher profit probability due to narrower breakeven points, making them preferable when you expect moderate volatility. Strangles provide better cost efficiency and risk-reward ratios when you anticipate extreme movements.

Risk Management for Strangle Positions

Effective risk management forms the foundation of sustainable options trading. The flexibility of strangles requires careful control mechanisms.

Position Sizing and Volatility Assessment

Some traders use position sizing rules such as limiting a single options strategy to a small percentage of typically around 1% to 3% of portfolio value. In practice, traders often apply stricter position limits of around 0.5% to 2% for strategies with theoretically unlimited risk. This ensures losses do not significantly impact overall capital.

Implied volatility analysis can be an important consideration. Some traders compare current implied volatility with its historical range before entering a strangle. Long strangles may be considered when implied volatility is in the lower quartile of its historical range, while short strangles may be evaluated when implied volatility is in the upper quartile, where option premiums are typically higher.

Managing Positions

For long strangles, take partial profits by closing the profitable side while holding the losing side if the market might reverse. If time passes without movement, cut losses rather than holding to expiration. For short strangles, close early if both options decay significantly to lock in profit while eliminating risk. Close short strangles if losses reach 200% to 300% of premium collected to prevent catastrophic outcomes.

Factors Affecting Strangle Profitability

Time Decay and Volatility

Time decay significantly affects strangle positions. Long strangles lose value daily regardless of price movement, with decay accelerating near expiration. Short strangles benefit from time decay, earning profit as time passes without significant price movement.

Long strangles gain value when implied volatility rises even without price movement, making pre-volatility purchases profitable. Short strangles lose value when implied volatility increases, with sudden spikes triggering substantial unrealized losses.

Strike Selection

Strike choices impact both cost and success probability. Selecting strikes with 20 to 30 delta provides reasonable premium collection or costs while maintaining profit potential. Narrower strikes increase costs but improve profit probability for long strangles. Wider strikes reduce costs but require more dramatic movements.

Frequently Asked Questions

What is the difference between a strangle and a straddle?

A straddle involves buying or selling options at the same strike price (typically at-the-money), while a strangle uses different strike prices (typically out-of-the-money). Strangles cost less to establish but require larger price movements to become profitable compared to straddles.

When should I use a long strangle instead of a short strangle?

A long strangle may be considered when significant price movement is expected in either direction, particularly if implied volatility is relatively low. A short strangle may be evaluated when the market is expected to remain range-bound, especially if implied volatility is relatively high.

How much can I lose with a strangle strategy?

With a long strangle, your maximum loss is limited to the total premium paid for both options. With a short strangle, potential losses are unlimited on the upside and substantial on the downside if the underlying asset moves significantly beyond your strike prices.

What happens to a strangle at expiration?

At expiration, any options that are out-of-the-money expire worthless. For a long strangle, you lose the premium paid if both options expire worthless. For a short strangle, you keep the full premium collected if both options finish out-of-the-money.

Is a strangle strategy suitable for beginners?

Long strangles can be suitable for beginners due to defined, limited risk equal to the premium paid. Short strangles carry unlimited risk and are better suited for experienced traders who understand options mechanics, risk management, and position sizing.

Conclusion

The options strangle strategy provides Singapore investors with a versatile approach to trading market volatility through US market options. By using out-of-the-money calls and puts with different strike prices, strangles offer cost advantages over straddles while adapting to multiple market scenarios. Long strangles position you to capture significant price movements when direction remains uncertain, while short strangles generate income during stable periods.

Success with strangles requires understanding risk-reward tradeoffs, implementing disciplined position management, and maintaining realistic expectations. The strategy demands attention to implied volatility levels, time decay effects, and proper position sizing to protect capital. Longbridge provides access to diverse investment products including US market options for implementing these strategies.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.