Put Options: Hedging Strategies for Singaporeans

Learn how put options work as portfolio insurance for Singapore investors. Explore protective put strategies, risk management techniques, and practical implementation tips.

TL;DR: Put options function as portfolio insurance, giving Singaporean investors the right to sell stocks at predetermined prices. This put options guide covers protective put strategies, collar strategies, and practical implementation tips to help investors hedge against market downturns while maintaining upside potential.

Market volatility is an inherent part of investing, and Singaporean investors seeking to protect their portfolios need effective risk management tools. Put options offer a strategic solution—functioning much like insurance policies for your stock holdings. Whether investors hold Singapore stocks, US stocks, or Hong Kong shares through platforms regulated by the Monetary Authority of Singapore (MAS), understanding put options can help navigate uncertain market conditions with confidence.

This comprehensive put options guide explores how these financial instruments work, when to use them, and how Singaporean investors can implement hedging strategies to protect their portfolios without completely liquidating positions.

What Are Put Options?

A put option is a contract that grants the owner the right, but not the obligation, to sell an underlying asset at a specified price (called the strike price) on or before a predetermined expiration date. Each options contract typically represents 100 shares of the underlying stock.

Unlike stock ownership, where you benefit from price increases, put options gain value when the underlying asset's price declines. According to research from the Corporate Finance Institute, put options become more valuable as stock prices fall, making them an effective hedging tool during market downturns.

How Put Options Work

When you purchase a put option, you pay an upfront cost called the premium. This premium represents the maximum amount you can lose, regardless of how the underlying stock performs. If the stock price falls below the strike price, you can exercise your right to sell at the higher strike price, generating a return that offsets losses in your stock holdings.

For example, if an investor owns 100 shares of a company trading at SGD 50 and purchases a put option with a SGD 45 strike price for SGD 1 per share (SGD 100 total premium), the investor has protected the position against significant downside. If the stock plummets to SGD 30, the investor can still sell at SGD 45, limiting the loss to SGD 600 instead of SGD 2,000.

Put Options vs Call Options

Understanding the distinction between put and call options is fundamental to this put options guide. A call option gives you the right to buy a stock at a specified price, profiting when prices rise. Conversely, a put option gives you the right to sell at a specified price, profiting when prices fall. For hedging purposes, put options provide protection against downside risk.

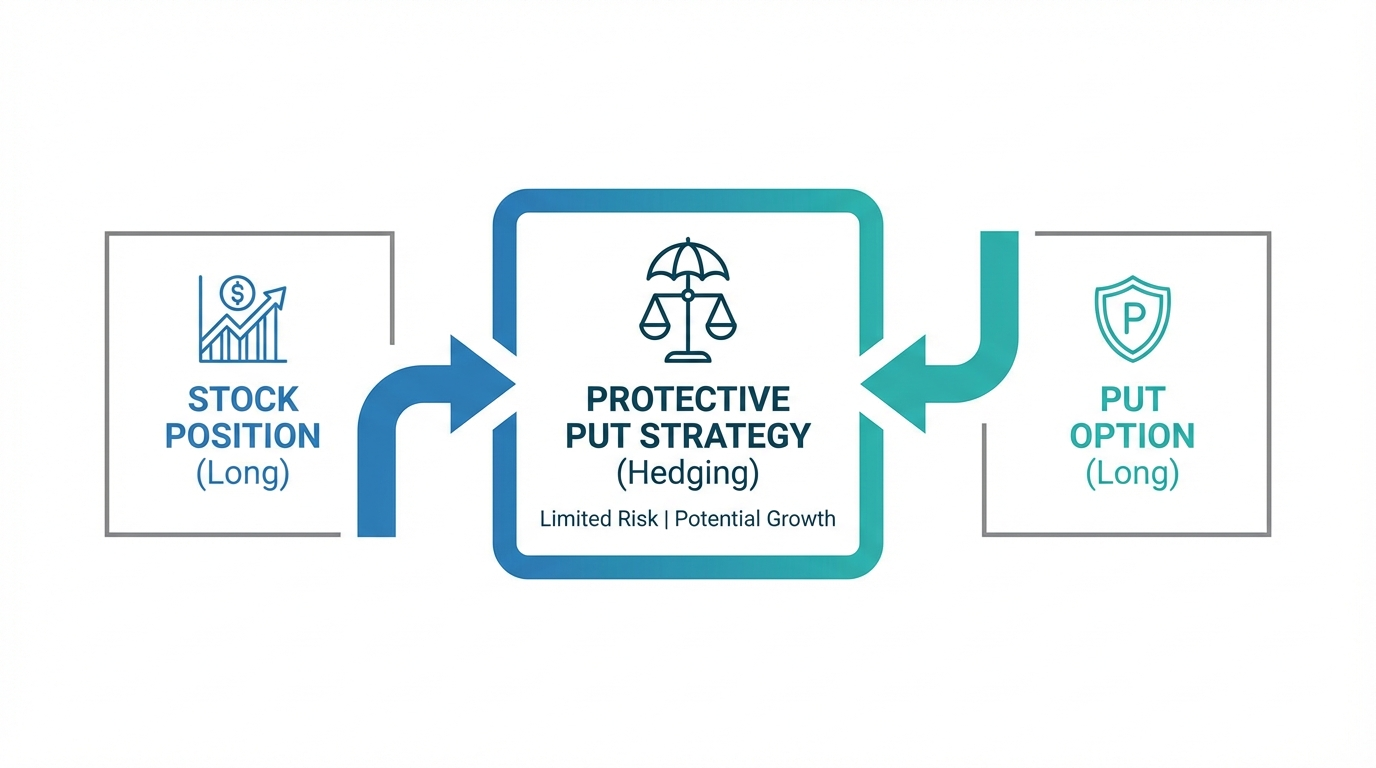

Understanding Protective Put Strategies

The protective put strategy is the most straightforward hedging approach for investors who own stocks and want downside protection. This strategy combines stock ownership with put option purchases to create a safety net.

Protective puts are particularly valuable when investors believe in a stock's long-term potential but anticipate short-term volatility, market conditions appear uncertain, they hold concentrated positions with significant unrealized gains, or earnings announcements may trigger price swings.

Advanced Hedging: The Collar Strategy

For investors seeking cost-effective hedging, the collar strategy combines a protective put with the sale of a call option at a higher strike price. For example, If an investor owns100 shares at SGD 50, the investor might buy a put at SGD 45 and sell a call at SGD 55. This approach limits both potential downside and upside, creating a "collar" around your position.

Generally, collars are particularly useful for dividend-focused investors who want to reduce hedging costs while accepting capped gains. The call premium received partially or fully offsets the put premium paid, sometimes creating a "zero-cost collar."

Out-of-the-Money Puts for Partial Protection

Not all hedging strategies require comprehensive protection. Out-of-the-money (OTM) puts offer a middle ground between full protection and no hedging. An OTM put has a strike price below the current market price. For instance, if a stock trades at SGD 50, an OTM put might have a strike price of SGD 40 or lower.

OTM puts usually require a lower premium than at-the-money alternatives because they provide protection only if the stock experiences a significant decline. OTM puts work well when investors seek protection against significant losses without paying high premiums, or when their risk tolerance accepts moderate declines but not major crashes.

Key Considerations Before Implementing Put Option Hedging

Before implementing put option strategies, Singaporean investors should evaluate several critical factors that affect hedging effectiveness and cost.

Time Decay and Expiration

Options are time-sensitive instruments. As expiration approaches, option premiums decline due to time decay—even if the underlying stock price remains stable. Options theory indicates that time decay accelerates in the final weeks before expiration, requiring regular protection renewals.

Hedging Costs and Portfolio Size

Hedging costs depend on portfolio size, protection level, time horizon, and market volatility. Hedging all holdings is more expensive than partial hedging. Many investors hedge only their largest or most volatile positions.

Regulatory Compliance

Singapore investors must trade options through MAS-regulated platforms. Most brokers require investors to demonstrate options trading knowledge and sign acknowledgment agreements. While Singapore does not impose capital gains tax on investment activities, according to IRAS, gains from trading financial derivatives as personal investment are generally not taxable. Yet, taxation depends on individual circumstances, and investors should consult a tax advisor.

Practical Implementation: Choosing Strike Prices and Expiration Dates

Successful hedging requires strategic selection of strike prices and expiration dates based on individual risk tolerance, time horizon, and market outlook.

Strike Price Selection

The strike price choice determines the protection level and premium cost. At-the-money puts offer immediate protection but carry the highest cost. Slightly out-of-the-money puts (5-10% below current price) provide a balanced approach. Deep out-of-the-money puts (15%+ below current price) offer the lowest cost but only protect against severe declines.

Expiration Date Selection

Near-term expiration (1-2 months) has lower costs but requires frequent renewals. Medium-term expiration (3-6 months) balances cost and coverage duration. Long-term expiration (6+ months or LEAPS) requires higher upfront premiums but fewer renewals.

Position Sizing

Investors do not need to hedge their entire portfolio. Consider full hedging (one put per 100 shares), partial hedging (50-75% coverage), selective hedging (largest positions only), or portfolio-level hedging using index puts.

Monitoring Hedged Position

Once investors have established put option protection, ongoing monitoring ensures their hedging strategy remains aligned with their investment objectives. Key metrics to track include delta, theta (daily time decay), and implied volatility.

Consider adjusting the hedging position when stock prices change significantly, implied volatility shifts, the investment thesis changes, or options approach expiration. Longbridge's real-time market data helps investors monitor these factors. As put options approach expiration, investors can "roll" their position by closing the expiring option and purchasing a new one with a later expiration date.

Common Mistakes to Avoid

Over-hedging may erode profitability through premium costs. Match hedging intensity to actual risk levels—not every position requires full protection. Calculate all-in hedging costs including premium costs, transaction fees, and bid-ask spreads before implementing strategies.

Investors often check put options during market declines, as this often means paying inflated premiums. Instead, establish systematic hedging rules based on portfolio allocation and risk tolerance. View put options as part of a comprehensive risk management framework alongside stop-loss orders, position sizing, and portfolio diversification.

Frequently Asked Questions

How do put options work for beginners?

Put options give the holder the right to sell a stock at a specific price (strike price) before a certain date (expiration). The holder pays an upfront premium for this right. If the stock price falls below the strike price, the position benefits by selling at the higher strike price. If not, the option expires, losing only the premium paid.

When are put options typically purchased?

Put options are typically considered when investors expect a stock price to decline or want to protect existing holdings from downside risk. Common scenarios include anticipating short-term volatility while maintaining long-term conviction, hedging concentrated positions, or protecting gains during uncertain periods. Put options are most cost-effective when purchased before volatility spikes.

What is the difference between put options and call options?

Put options give the holder the right to sell a stock at a specified price, profiting when prices fall. Call options give the holder the right to buy, profiting when prices rise. Both involve paying premiums for the right (not obligation) to transact at predetermined prices.

Are put options risky for Singapore investors?

Put options carry defined, limited risk when purchased. The maximum loss is the premium paid upfront, regardless of how the underlying stock performs. This makes buying put options less risky than short selling stocks, which has unlimited loss potential. Singapore investors should understand contract mechanics, time decay, and volatility effects before trading through MAS-regulated platforms.

How much does it cost to hedge with put options?

Hedging costs vary based on strike price proximity, time to expiration, underlying stock volatility, and portfolio size. For a typical stock position, protective put premiums might range from 1-5% of the underlying position value for three to six months of protection, though this varies based on market conditions. Investors should note that actual costs are highly variable and depend on factors such as implied volatility and market conditions.

Conclusion

Put options provide Singaporean investors with a powerful tool for portfolio protection, functioning as insurance against market downturns while preserving upside potential. This put options guide has explored protective puts, collar strategies, and out-of-the-money puts—each offering different cost-protection trade-offs.

Successful hedging requires understanding strike price selection, expiration timing, and ongoing position management. While put options involve premiums and time decay, they offer flexibility and defined risk that complement portfolio management techniques.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.