Time Decay (Theta): Options Enemy or Friend?

Time decay affects every options trade. Learn how theta works, when it's your ally or adversary, and practical strategies to navigate this powerful force in options markets.

TL;DR: Time decay (theta) reduces options value as expiration approaches, working against buyers but benefiting sellers. Whether theta is your enemy or friend depends entirely on your position: long options lose value daily, while short options profit from this predictable erosion. Understanding theta patterns helps you select optimal strategies and manage risk effectively.

Every options trader eventually faces the same realization: time is not neutral. Each day that passes chips away at your position's value, regardless of whether the underlying stock moves in your favor. This phenomenon, known as options time decay or theta, represents one of the most predictable yet frequently misunderstood forces in derivatives markets.

The question is not whether time decay exists but rather how you position yourself relative to it. For some traders, theta represents a relentless enemy that erodes profitable positions before they can be realized. For others, it serves as a reliable ally that generates consistent returns through strategic selling.

Singapore investors accessing United States (US) options markets need to grasp theta mechanics before deploying capital. This guide examines how time decay functions, when it helps or hurts your portfolio, and common practical strategies for managing this critical characteristic. Whether you are exploring educational resources on options trading or actively building positions, theta awareness can help investors better understand options risk dynamics.

What Is Theta and How Does It Measure Time Decay?

Theta represents the rate at which an option's value declines due to the passage of time, measured as the expected price change per day. If an option displays a theta of negative 0.05, its premium theoretically decreases by USD 0.05 each day, assuming all other market factors remain constant.

This Greek letter quantifies what options traders call extrinsic value erosion. Unlike intrinsic value (the amount an option is in-the-money), extrinsic value represents the premium traders pay for the possibility of favorable price movement before expiration. As expiration approaches, this possibility diminishes, and with it, the extrinsic component of the option's price.

Options premiums consist of intrinsic and extrinsic value. Intrinsic value equals the difference between the stock price and strike price for in-the-money options. An option to buy Stock A at USD 50 when it trades at USD 55 contains USD 5 of intrinsic value, unaffected by time decay.

Extrinsic value comprises everything beyond intrinsic worth, primarily reflecting time until expiration and implied volatility. A call option on Stock A with a USD 50 strike trading at USD 7 when the stock sits at USD 55 has USD 2 of extrinsic value vulnerable to theta decay.

As expiration nears, the probability that an out-of-the-money option will become profitable decreases. An option with 60 days until expiration offers substantially more opportunity for price movement than one expiring in 10 days. Markets price this temporal advantage into premiums, and theta measures its daily erosion.

Theta as Enemy: When Time Decay Works Against You

For traders holding long options positions (buying calls or puts), theta operates as a constant headwind. Every morning, your position's value has decreased slightly, even if the underlying stock price remains unchanged. This daily erosion continues regardless of market conditions, requiring the underlying asset to move sufficiently to overcome time decay losses.

Option buyers face a two-front battle: the underlying stock must move in the predicted direction with sufficient speed and magnitude to offset theta decay. This dual requirement explains why many long options positions expire worthless despite directionally correct predictions.

Consider a trader who buys a call option on Stock B trading at USD 100, selecting a USD 105 strike with 30 days until expiration. If the stock gradually rises to USD 103 over three weeks, the position might still show a loss due to accelerated time decay in the final weeks. The directional forecast proved correct, but the timing fell short of overcoming theta.

Time decay does not progress linearly. Options lose value slowly when expiration sits months away but shed premium rapidly in the final weeks. At-the-money (ATM) options particularly experience sharp acceleration as expiration approaches, with theta increasing dramatically in the last 30 days. This acceleration creates a critical planning consideration for option buyers. Many experienced traders avoid buying options inside this window unless anticipating immediate, substantial price movement.

Theta as Friend: When Time Decay Works for You

Selling options reverses the theta relationship entirely. Short options positions (selling calls or puts) benefit from time decay, with theta representing daily profit as the sold option loses value. This dynamic forms the foundation of income-generating options strategies favored by traders seeking consistent returns.

When you sell an option, you collect premium upfront. As days pass, the option decreases in value due to theta decay. If it expires worthless or you buy it back at a lower price, the difference represents profit. Time works in your favor.

Several strategies capitalize on theta decay. Covered calls involve selling call options against stock you own, generating income while maintaining upside participation to the strike price. Cash-secured puts collect premium while potentially acquiring stock at a discount.

Credit spreads combine buying and selling options at different strikes, benefiting from theta decay while defining maximum risk. Iron condors extend this by combining both call and put credit spreads, profiting from range-bound markets where theta steadily erodes sold options' value.

While theta works favorably for option sellers, these positions carry different risk characteristics than buying options. Sellers face theoretically unlimited risk on naked calls (if the underlying stock rises dramatically) and substantial risk on naked puts (if the stock falls sharply). Successful implementation requires disciplined risk management and position sizing.

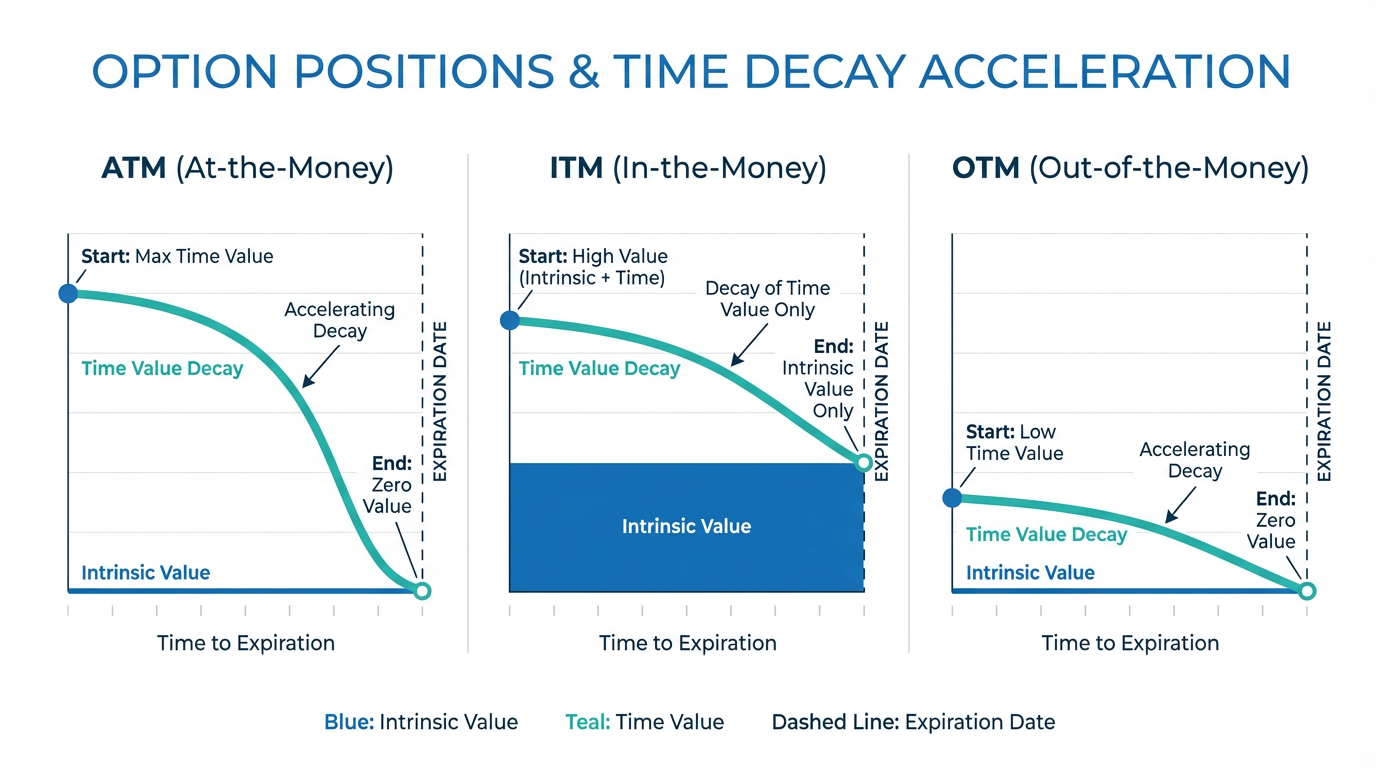

How Different Options Experience Time Decay

Not all options decay at the same rate. The relationship between the strike price and current stock price (known as moneyness) significantly influences theta values. Understanding these differences helps traders select optimal strike prices and expiration dates for their market outlook.

At-the-money options, where the strike price equals the current stock price, contain maximum extrinsic value. This makes ATM options particularly sensitive to time decay, exhibiting the highest absolute theta values. For a stock trading at USD 200, the USD 200 strike options hold purely extrinsic value that erodes most rapidly as expiration approaches.

In-the-money (ITM) options contain intrinsic value immune to time decay. Only the extrinsic portion decays. An ITM call with USD 10 of intrinsic value and USD 2 of extrinsic value experiences theta decay only on the USD 2 component, making ITM options less sensitive to time decay.

Out-of-the-money (OTM) options consist entirely of extrinsic value but contain less absolute premium than ATM options. While theta values appear lower in dollar terms, the percentage impact can be substantial. An OTM option trading at USD 0.50 with theta of negative 0.02 loses 4 percent of its value daily.

Factors That Influence Time Decay Rates

Implied volatility measures the market's expectation of future price fluctuations. Higher implied volatility increases options premiums, particularly extrinsic value components. Since theta decays extrinsic value, higher volatility options exhibit higher absolute theta values. Before significant corporate events like earnings, implied volatility typically spikes, intensifying time decay rates.

The relationship between time remaining and decay rate follows a non-linear pattern. Options with 90 days until expiration decay slowly, but as expiration nears, decay accelerates dramatically inside 30 days.

Practical Strategies for Managing Time Decay

Option buyers might consider reducing theta headwinds by purchasing longer-dated options (60 to 90 days until expiration) for slower daily decay rates, or selecting slightly in-the-money options where intrinsic value provides protection. Timing entries around expected catalysts like earnings announcements reduces time fighting theta while positioning for expected movement.

Some options sellers focus on contracts with approximately 30–45 days to expiration, where time decay often accelerates. Many experienced sellers close positions when capturing 50 to 80 percent of maximum profit rather than holding until expiration, recycling capital more efficiently.

Frequently Asked Questions

Is theta always negative for option buyers?

Yes, theta consistently works against long options positions because buyers pay premium for time value that inevitably decreases as expiration approaches. The only exception occurs at expiration when theta becomes zero since no time value remains.

How much does an option typically lose to theta decay daily?

Theta values vary widely based on multiple factors. At-the-money options with 30 days until expiration might display theta between negative 0.03 and negative 0.10, depending on the stock's volatility and price. Higher-priced and more volatile securities exhibit higher absolute theta values.

Can I profit from time decay without selling options?

Direct profit from time decay requires short options positions where you benefit from value erosion. However, certain spread strategies create theta-positive positions while limiting risk. Calendar spreads (selling near-term options and buying longer-dated options) can generate positive theta since near-term options decay faster than longer-dated equivalents.

Do weekends and holidays affect time decay?

Options pricing models typically account for calendar days, not just trading days, when calculating time decay. Theta continues eroding value over weekends and holidays, though options markets remain closed. Some traders consider this "weekend theta" when planning short-term positions.

Should beginners avoid theta decay entirely?

Rather than avoiding theta, beginners should understand how it affects different strategies and select approaches aligned with their risk tolerance. Starting with theta-positive strategies like covered calls provides income while learning options mechanics. Buying longer-dated options (90-plus days) reduces daily theta impact.

Conclusion

Time decay represents neither inherent enemy nor automatic friend in options trading. Your position determines which side of the theta equation you occupy. Long options holders battle daily value erosion that demands timely, substantial underlying price movement. Short options sellers collect premiums that decay predictably, generating income in stable or neutral markets while accepting defined risks.

Successful options trading requires honest assessment of your market outlook, risk tolerance, and time horizon. Rapid price movements tend to have a greater impact on long options positions because price changes may offset time decay. Anticipating range-bound markets with gradual trends favors theta-positive selling strategies.

Singapore investors accessing US options trading through Longbridge benefit from understanding theta mechanics before deploying capital. Whether building protective positions, generating portfolio income, or expressing directional views, time decay affects every options transaction.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.