Understanding Gamma in Options Trading

Gamma measures how quickly your options position changes as markets move. Understanding this second-order Greek is essential for managing risk in US options trading.

TL;DR: Gamma measures how quickly your options delta changes when the underlying stock moves by USD 1. Understanding gamma may help you anticipate how your position's risk profile shifts with market movements, particularly as expiration approaches when gamma accelerates dramatically.

When you trade options, understanding delta may give you a snapshot of your current risk exposure. But markets move continuously, and that risk exposure changes with every price tick. Gamma can tell you how fast those changes happen.

For Singapore traders accessing US options markets through platforms like Longbridge, gamma represents a crucial second-order risk metric. While delta measures your position's sensitivity to price movements, gamma measures the rate at which that sensitivity itself changes. Think of delta as speed and gamma as acceleration.

This distinction matters because options positions can shift from manageable to highly volatile quickly, especially near expiration. A position that seems stable one day can become dramatically exposed the next as gamma amplifies your delta risk. Understanding gamma may help you anticipate these changes and manage your portfolio accordingly.

What is Gamma in Options

Gamma measures the rate of change in an option's delta for every USD 1 movement in the underlying stock price. In mathematical terms, gamma is the first derivative of delta and the second derivative of the option price with respect to the underlying asset.

For example, consider a call option with a delta of 0.50 and a gamma of 0.05. If the underlying stock increases by USD 1, your new delta becomes 0.55. If the stock decreases by USD 1, your delta becomes 0.45.

This relationship between gamma and delta is fundamental to understanding options trading fundamentals. While delta tells you your current directional exposure, gamma tells you how that exposure evolves.

Gamma Values Across Different Options

Gamma values typically range from 0 to 1 for individual options, though the exact value depends on several factors:

Long positions (buying calls or puts) always have positive gamma. When you own options, rising gamma works in your favour because your delta moves in the profitable direction as the stock price moves.

Short positions (selling calls or puts) always have negative gamma. When you sell options, gamma works against you because your delta moves in the loss-making direction as the stock price moves.

At-the-money (ATM) options have the highest gamma values. This makes sense intuitively: small price movements can quickly shift an ATM option from being in-the-money to out-of-the-money or vice versa, creating rapid delta changes.

Deep in-the-money (ITM) options have low gamma because they already behave almost like the underlying stock. Their delta is already close to 1.00 for calls or -1.00 for puts, leaving little room for change.

Deep out-of-the-money (OTM) options also have low gamma because they're unlikely to finish in-the-money. Their delta remains close to zero regardless of small price movements.

The Delta-Gamma Relationship

Understanding how delta and gamma work together is essential for risk management. Delta provides a linear approximation of price changes, but gamma corrects for non-linearity. This curvature gives options their distinctive risk-reward profile.

Why This Relationship Matters for Risk Management

When you hold multiple options or construct multi-leg strategies, gamma exposure accumulates and can dominate your risk profile.

For example, consider a trader who sells ten at-the-money put options. The delta might suggest moderate directional risk, but the negative gamma means that if the stock moves sharply lower, the delta becomes increasingly negative. What started as manageable becomes a much larger short exposure.

Conversely, traders who buy options benefit from positive gamma. As the stock moves in their favour, their position automatically gains more directional exposure. This convexity is what options buyers pay for through the premium.

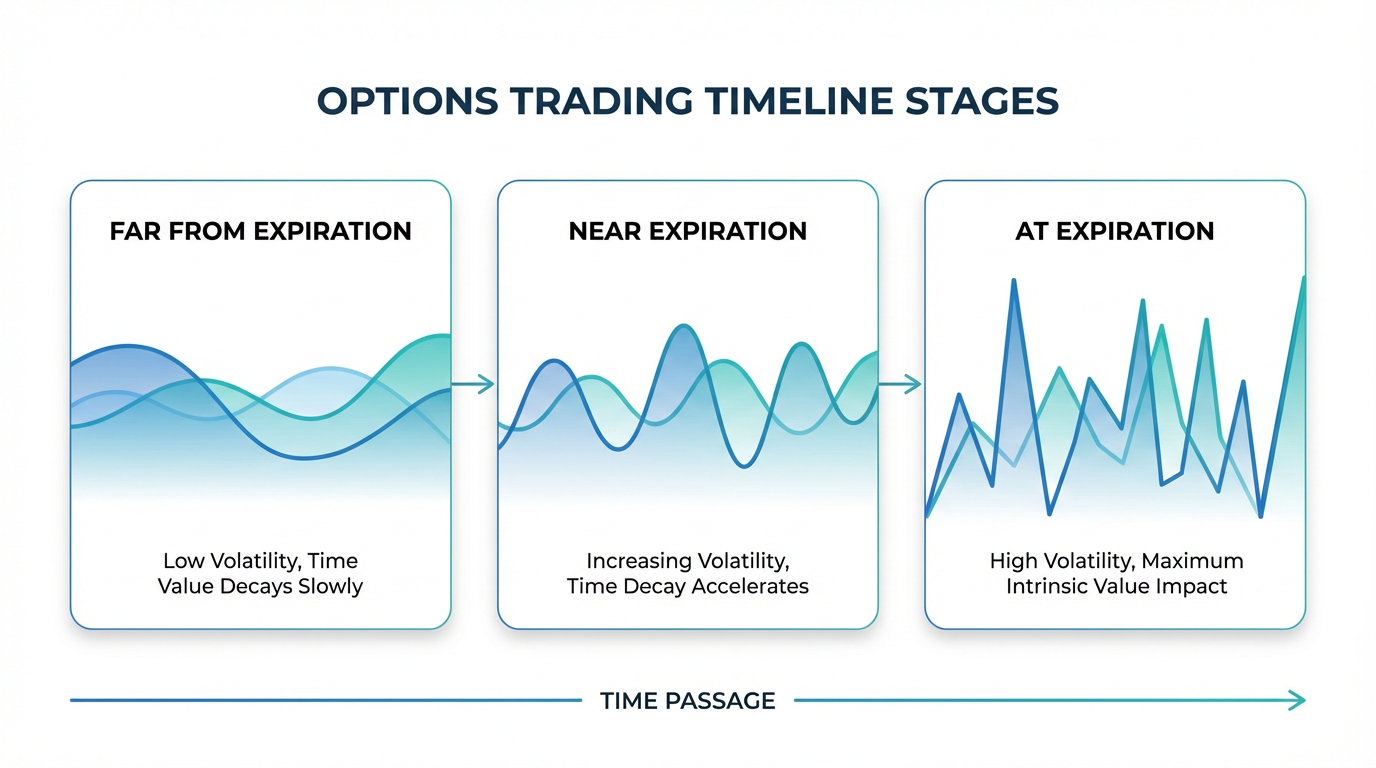

How Time Affects Gamma

Time to expiration may dramatically influence gamma behaviour. As expiration approaches, gamma increases for at-the-money options while decreasing for in-the-money and out-of-the-money options.

The Gamma Explosion Near Expiration

Options with just days or hours until expiration may exhibit extremely high gamma for at-the-money strikes. This phenomenon, sometimes called "gamma risk" or the "gamma explosion," occurs because small price movements can determine whether the option finishes in-the-money or worthless.

For traders holding short-dated ATM options, this may create substantial risk. A position that showed modest delta exposure on Monday can swing wildly by Friday as gamma accelerates the delta changes.

This effect is particularly relevant for Singapore traders trading US options, where market hours differences mean overnight gaps can create significant price movements. An option that closes slightly out-of-the-money in Singapore evening hours might open deep in-the-money the next morning due to US market movements.

Long-Dated Options and Gamma Stability

Options with months until expiration may typically have lower gamma, making their delta more stable. This stability costs more in premiums but provides predictable risk management and suits longer-term trading approaches.

Why Singapore Traders Should Care About Gamma

Singapore traders accessing US options markets face unique considerations when managing gamma risk. Time zone differences, currency exposure, and market access patterns all influence how gamma affects your trading.

Market Hours and Overnight Risk

US markets trade during Singapore's evening and early morning hours. This creates scenarios where significant price movements occur while you may not be actively monitoring positions.

High gamma positions amplify this overnight risk. An at-the-money option held into the US trading session can swing dramatically if news breaks or the market moves sharply. By the time Singapore markets open the next day, your position's risk profile may have changed completely.

Traders using Options trading in US markets through Longbridge can access real-time data and execute trades during US hours, but the timezone difference still requires careful planning around high-gamma periods.

Position Sizing with Gamma Awareness

Retail traders may size positions based on delta alone, overlooking how gamma can amplify exposure. A position sized appropriately today might become uncomfortably large as gamma drives delta higher.

As a practical guideline, you might want to consider how your delta could change if the underlying moves 5-10 percent. If that gamma-adjusted delta exceeds your risk tolerance, you can consider reducing position size or choosing strikes with lower gamma.

Managing Gamma Risk in Your Portfolio

Effective gamma management doesn't require complex mathematics or professional trading tools. Several straightforward approaches help retail traders control gamma exposure.

Practical Gamma Management Strategies

Choose your expiration dates strategically. Shorter-dated options provide higher leverage but come with higher gamma risk. Longer-dated options cost more but offer more stable gamma profiles. Match your expiration choice to your intended holding period and risk tolerance.

Monitor position gamma regularly. Most options platforms, including Longbridge's trading interface with real-time market data, display gamma values. Check how your gamma changes as expiration approaches and the underlying price moves.

Consider spreading strategies. Multi-leg options strategies can be constructed to reduce net gamma exposure. A long call spread, for example, combines positive gamma from the long call with negative gamma from the short call, resulting in lower net gamma than a naked long call.

Avoid high gamma near expiration without active monitoring. If you cannot actively monitor and adjust positions during US market hours, you should consider closing or rolling short-dated ATM options before the final week to expiration. The gamma risk typically outweighs the remaining time value for traders who cannot respond quickly to adverse movements.

When High Gamma Works in Your Favour

Positive gamma benefits traders who correctly anticipate direction. If you buy a call and the stock rallies, gamma automatically increases your delta, amplifying gains. This convexity is one of options' most attractive features.

Ensure your position size can withstand volatility. Even when gamma works in your favour, sharp temporary moves against your position can trigger stops or margin calls before the eventual favourable outcome.

Common Gamma Mistakes to Avoid

Ignoring Calendar Effects

An option with two weeks until expiration behaves very differently from the same strike with two days remaining, even at identical stock prices. This calendar effect becomes critical when rolling positions, as moving from short-dated to longer-dated options dramatically changes gamma exposure.

Underestimating Weekend and Holiday Risk

US market holidays and weekends create gaps in price discovery. For Singapore traders, a three-day US holiday weekend might span four calendar days from your perspective, creating extended gap risk in high-gamma positions.

Treating All Greeks Equally

High gamma often coincides with high theta (time decay), meaning your position loses value rapidly even if the stock price remains stable. Understanding these tradeoffs helps evaluate whether gamma exposure matches your trading objectives.

Frequently Asked Questions

What is gamma in options trading?

Gamma measures how much an option's delta changes when the underlying stock price moves by USD 1. It represents the rate of change of delta, helping traders understand how position sensitivity evolves with price movements.

Is high gamma good or bad for options traders?

High gamma may benefit buyers who correctly anticipate direction, as it amplifies gains. However, it may hurt options sellers and may create risk for anyone unable to actively manage positions, as it causes rapid, unexpected changes in exposure.

How does gamma change as options approach expiration?

Gamma increases dramatically for at-the-money options near expiration because small price movements determine whether the option finishes in-the-money or worthless. In-the-money and out-of-the-money options see gamma decrease.

Should Singapore traders worry about gamma when trading US options?

Yes, timezone differences mean high gamma positions can change dramatically during US trading hours when Singapore traders may be unable to monitor positions actively, making gamma awareness essential for risk management.

Can you hedge gamma risk in options trading?

Yes, gamma can be hedged through offsetting options positions with opposite gamma exposure. Professional traders may use dynamic hedging strategies involving the underlying asset, though this requires active management and incurs transaction costs.

Conclusion

Gamma represents a fundamental dimension of options risk that every trader should understand. While delta shows your current position, gamma reveals how quickly that position changes with market movements.

For Singapore traders accessing US options markets through platforms like Longbridge, gamma awareness is critical. Timezone differences and the accelerating nature of gamma near expiration create scenarios where positions shift dramatically during hours when you may be unable to monitor them actively.

Manage gamma effectively by matching expiration dates to your monitoring capabilities, sizing positions conservatively, and exercising caution with at-the-money options approaching expiration. Understanding how risk evolves over time might separate successful options traders from those who merely hope for favourable outcomes.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.