Vega Options Explained: A Practical Guide to Volatility and Skew

Discover how vega helps you understand option price sensitivity to volatility changes. This guide covers implied volatility, skew patterns, and practical strategies for managing volatility exposure.

TL;DR: Vega measures how much an option's price changes when implied volatility moves by 1%. Understanding vega alongside volatility skew patterns helps you anticipate price movements and manage exposure, whether you hold long or short options positions.

Options pricing involves more than just tracking the underlying asset's price. Implied volatility, often called IV, plays a central role in determining what you pay for an option contract. This is where vega becomes essential. As one of the key options Greeks, vega quantifies your exposure to volatility changes. When you combine this understanding with volatility skew, which describes how implied volatility varies across different strike prices, you gain deeper insight into market sentiment and option pricing dynamics.

This guide breaks down vega options explained in practical terms, walks through volatility skew patterns, and shows how these concepts connect to help you make more informed trading decisions.

What Is Vega in Options Trading?

Vega measures the estimated change in an option's price for every 1% movement in implied volatility. Unlike delta, which tracks price sensitivity to the underlying asset, vega focuses entirely on volatility expectations.

For example, if an option has a vega of 0.12 and is priced at USD 5.00, a 1% increase in implied volatility would raise the option price to approximately USD 5.12. Conversely, a 1% decrease would lower it to around USD 4.88.

How Implied Volatility Differs from Historical Volatility

Historical volatility looks backward, measuring how much an asset's price has fluctuated over a specific period. Implied volatility looks forward, reflecting the market's expectation of future price movement. Options prices embed this forward-looking expectation, and vega captures your sensitivity to changes in that expectation.

When the market anticipates large price swings, whether due to earnings announcements, economic data releases, or geopolitical events, implied volatility rises. This elevated IV directly increases option premiums through vega exposure.

Key Factors That Influence Vega

Several factors determine the size of an option's vega value. Understanding these helps you select positions that align with your volatility outlook.

Moneyness and Vega Sensitivity

At-the-money (ATM) options exhibit the highest vega values. As an option moves further in-the-money or out-of-the-money, vega decreases. This occurs because ATM options have the greatest uncertainty regarding whether they will expire with intrinsic value.

Consider two options on the same underlying asset: one ATM and one deep out-of-the-money. The ATM option will show significantly higher sensitivity to volatility changes, making it more responsive when implied volatility shifts.

Time to Expiration

Vega is higher for options with more time until expiration. Longer-dated options have greater exposure to potential volatility changes because more time means more opportunity for unexpected events to affect pricing.

As expiration approaches, vega declines. Near-term options have less time for volatility expectations to shift, so they become less sensitive to IV changes. This relationship matters when structuring positions across different expiration cycles.

Long Vega Versus Short Vega Positions

Your vega exposure depends on whether you buy or sell options. This distinction shapes how volatility changes affect your profit and loss.

Long Vega Strategies

When you buy options, whether calls or puts, you hold positive vega. You benefit when implied volatility increases because rising IV pushes option premiums higher. However, if implied volatility declines, long option positions may lose value even if the underlying price moves modestly in the expected direction. Common long vega strategies include:

-

Long calls or long puts

-

Long straddles (buying a call and put at the same strike)

-

Long strangles (buying out-of-the-money calls and puts)

-

Calendar spreads in certain configurations

Long vega positions are generally more sensitive to increases in implied volatility and may be more affected during periods of volatility expansion.

Short Vega Strategies

Selling options gives you negative vega. You benefit when implied volatility decreases because declining IV reduces option premiums, allowing you to potentially close positions at lower prices.If implied volatility rises unexpectedly, short option positions may incur losses due to increasing option premiums. Short vega strategies include:

-

Naked or covered option writing

-

Credit spreads

-

Iron condors

-

Short straddles and strangles

Short vega positions are more sensitive to decreases in implied volatility and are affected differently during stable market conditions.

Tip: Monitor IV levels relative to their historical range before entering positions. When implied volatility is elevated relative to its historical range, option premiums may be higher. Subsequent normalization in volatility can affect option pricing.

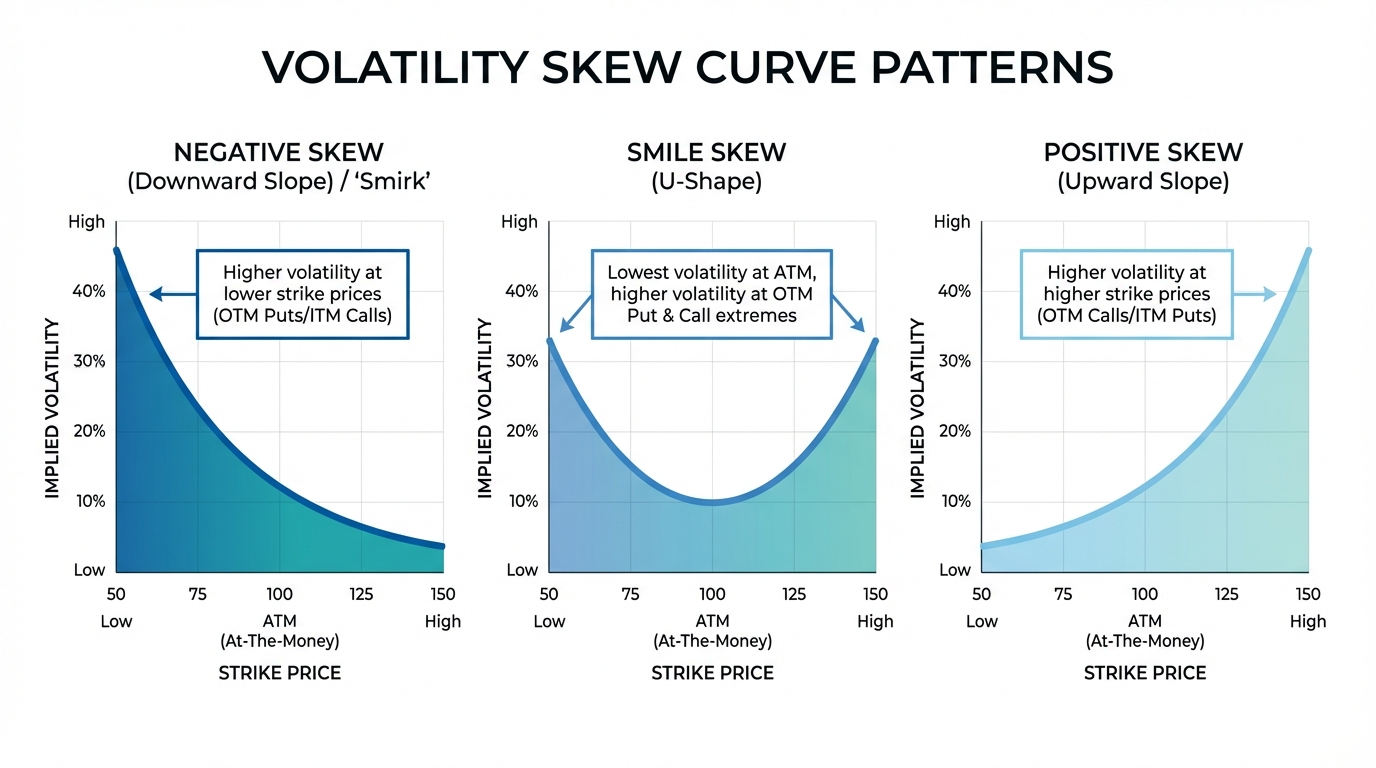

Understanding Volatility Skew

Volatility skew describes the pattern of implied volatility across different strike prices for options with the same expiration date. In a perfectly efficient market, all strikes would show identical IV. Reality differs; the market prices risk unevenly across strikes, creating recognizable skew patterns.

Negative Skew

The most common pattern in equity markets, negative skew shows higher implied volatility for out-of-the-money puts compared to out-of-the-money calls. This creates a downward-sloping curve when plotting IV against strike price.

Negative skew reflects the market's tendency to price in crash risk. Investors often pay a premium for downside protection, driving up the cost of lower-strike puts. This pattern intensified after the 1987 market crash and remains a persistent feature of equity options markets.

Positive Skew

Positive skew occurs when out-of-the-money calls carry higher implied volatility than puts. This upward-sloping pattern appears more frequently in commodity markets or assets where supply shocks can cause rapid price increases.

Gold options, for instance, sometimes exhibit positive skew when markets anticipate potential safe-haven buying during economic stress.

Smile Skew

A volatility smile forms when both out-of-the-money puts and calls show higher implied volatility than at-the-money options. This U-shaped pattern suggests the market expects significant movement in either direction but remains uncertain about which way.

Smile patterns appear more often in currency markets and during periods of heightened uncertainty around specific events.

How Vega and Skew Work Together

Understanding both concepts simultaneously provides practical advantages. Vega tells you how sensitive your position is to volatility changes; skew tells you where the market perceives risk across different price levels.

When negative skew is steep, out-of-the-money puts carry elevated IV. Buying these puts means paying a premium for implied volatility that exceeds at-the-money levels. If you hold these positions and skew flattens, even without a change in overall IV levels, your puts could lose value as their individual implied volatility normalizes.

Conversely, selling options in areas of elevated skew can capture premium if skew reverts toward more typical levels. This approach involves risk considerations, particularly during periods of market stress.

Calculating Position Vega

For portfolios with multiple options, calculating total position vega helps you understand aggregate volatility exposure. The formula is straightforward:

Position Vega = Contract Vega × 100 × Number of Contracts × Direction

Direction is +1 for long positions and -1 for short positions. Multiplying by 100 accounts for the standard contract size of 100 shares per option.

If you hold 5 long call contracts with a vega of 0.15, your position vega equals 0.15 × 100 × 5 × 1 = 75. A 1% increase in implied volatility would theoretically add USD 75 to your position value.

Getting Started with Vega in Your Trading

Applying vega and skew concepts requires attention to market context. Here are practical considerations:

Check IV Levels Before Entry: Compare current implied volatility to its historical range. Buying options when IV sits at the high end of its range increases the challenge of profiting as volatility normalizes.

Consider Expiration Selection: Longer-dated options provide more vega exposure but also more premium at risk. Match your time horizon to your volatility outlook.

Monitor Skew Changes: Track how the volatility surface shifts, not just overall IV levels. Skew movements affect specific strikes differently.

Balance Vega Across Positions: Combining long and short vega positions can create more neutral portfolios less sensitive to volatility swings.

Platforms offering options trading on US markets provide tools to view vega and other Greeks alongside your positions. This data supports more informed decision-making when evaluating investment products and managing exposure.

Frequently Asked Questions

What is a good vega value for options?

There is no single ideal vega value; the appropriate level depends on your strategy and volatility outlook. Higher vega suits traders expecting volatility expansion, while lower vega or negative vega positions benefit from stable or declining volatility.

Does vega affect calls and puts the same way?

Yes. Vega is positive for both long calls and long puts. An increase in implied volatility raises the theoretical value of both contract types equally, assuming other factors remain constant.

How do I reduce vega exposure in my portfolio?

You can reduce vega by selling options against long positions, using spreads that partially offset vega, or shifting toward shorter-dated expirations that naturally carry lower vega.

Conclusion

Vega provides essential insight into how volatility expectations affect option prices. Combined with an understanding of volatility skew, you can better interpret market sentiment, select appropriate strategies, and manage exposure effectively. These concepts form a foundation for navigating options markets with greater awareness.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.