MPF Investment Guide: Strategies for Choosing the Right Funds

MPF is more than just monthly deductions. Understand the five fund types, assess your risk tolerance, and leverage TVC tax benefits to maximize your MPF’s potential and boost your retirement savings.

TL;DR: The Mandatory Provident Fund (MPF) is an essential pillar of retirement security for every employee in Hong Kong. Actively selecting your funds, regularly reviewing your portfolio, and making use of Tax Deductible Voluntary Contributions (TVC) can help you manage your retirement savings more proactively. This article will walk you through the key strategies for choosing MPF funds, even if you’re starting from zero.

Every month, your MPF contribution is automatically deducted from your salary. For many Hong Kong employees, MPF feels like something the employer simply handles, but this passive attitude often means missing out on the full potential of decades of retirement savings. According to the MPFA, Hong Kong’s MPF system has accumulated assets of over HKD 1 trillion and covers more than 2.9 million employees, yet only a small number take an active approach to managing their MPF investment portfolios.

In reality, choosing MPF funds isn't complicated. With a few simple principles and a clear sense of your personal risk tolerance, you can make your mandatory savings work harder for you. In plain English, this article breaks down the steps to help you make smarter MPF fund selections and strengthen your retirement planning.

MPF Basics: Core Rules You Should Know

The Mandatory Provident Fund (MPF) is a statutory retirement savings system launched by the Hong Kong government in December 2000 and regulated by the MPFA. The law requires all employees aged 18 to 65 who have been employed for more than 60 days to enroll.

Contribution Rates and Limits

Typically, both the employer and employee must each contribute 5% of the employee's monthly salary. Monthly contributions are capped: for salaries of HKD 30,000 or above, the maximum contribution from both the employer and employee is HKD 1,500 each per month. If your monthly salary is less than HKD 7,100, you are exempt from employee contributions, but the employer must still contribute 5% of your salary.

Three Types of MPF Schemes

By law, MPF schemes fall into three categories:

-

Master Trust Scheme: Open to employees from different employers and the self-employed, offering economies of scale and commonly used by SMEs.

-

Employer Sponsored Scheme: Offered by a single large employer, only for its own employees.

-

Industry Scheme: For industries with high labor mobility, such as catering and construction.

Tip: Employers choose the scheme, but you have the right to choose the funds within the scheme. Exercising this right is the first step to taking control of your MPF.

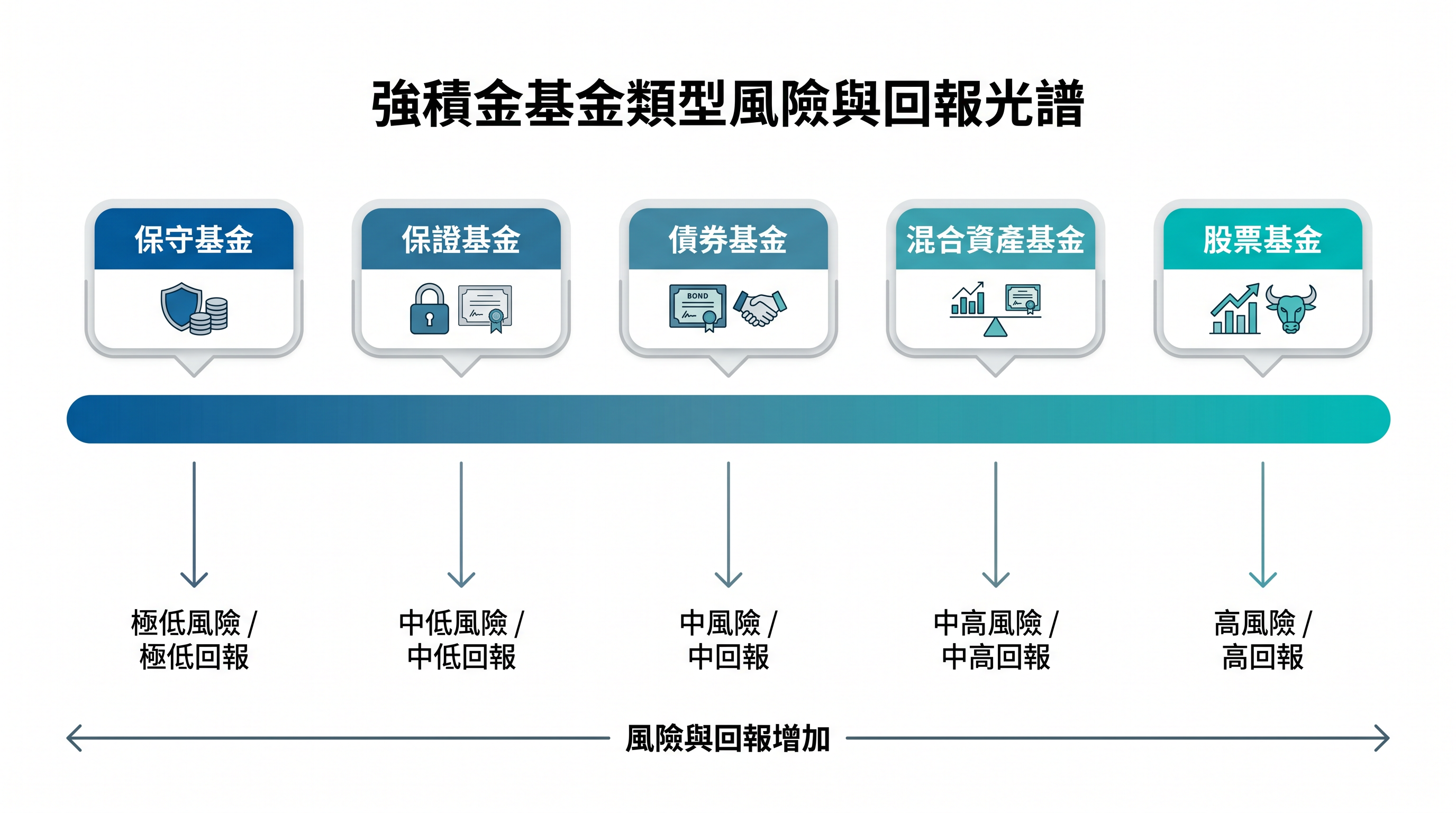

A Closer Look: The Five Main MPF Fund Types

MPF schemes offer five main types of funds, each with distinct risk and return characteristics. Understanding them is the first step in building your ideal portfolio.

Equity Funds

These mainly invest in stock markets—including Hong Kong, the US, and global equities. They offer higher potential returns but also greater market volatility, making them suitable for investors with a longer time frame and higher risk tolerance. Data from the MPFA fund platform shows equity fund expense ratios typically range from about 0.65% to 2.64%.

Mixed Assets Funds

These invest in both stocks and bonds, spreading risk across asset classes to reduce exposure to a single market. The risk level depends on the stock-to-bond ratio, making them suitable for those seeking a balance between return and risk.

Bond Funds

These focus mainly on various bonds, including government and corporate bonds. They provide relatively stable returns and less volatility compared to equity funds, and are suitable for those with lower risk tolerance or those nearing retirement.

Guaranteed Funds

These offer capital protection or minimum return guarantees, but come with conditions—such as needing to hold the fund for a specified period. Fees are typically higher, and switching funds before the lock-in period ends may lead to forfeiting the guarantee.

MPF Conservative Funds

These mainly invest in short-term deposits and Hong Kong dollar notes, focusing on capital preservation with lower returns. They are suitable for very conservative investors or those needing short-term capital protection.

How to Choose the Right MPF Funds for You

Once you understand the types of funds, the key is to make the most appropriate selections based on your own circumstances.

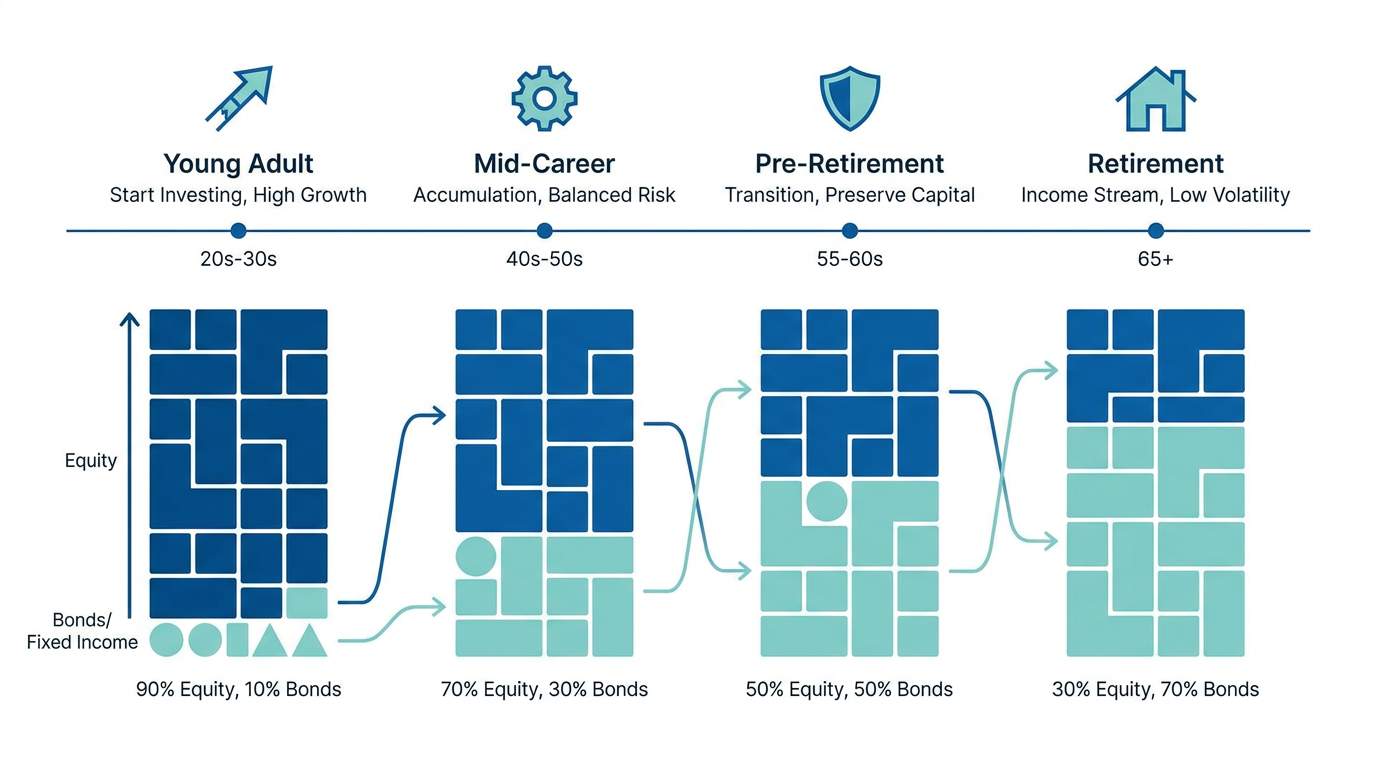

Step 1: Assess Your Risk Tolerance

Your ability to take on risk depends on several factors, such as age, income stability, family responsibilities, and personal financial goals. A common rule of thumb is the “100 minus age” formula—for instance, a 30-year-old might consider allocating roughly 70% of their MPF to equity funds and the rest to more conservative assets.

This is just a guideline to get started. Younger people have a longer investment horizon and can better weather short-term market ups and downs; those approaching retirement may want to gradually reduce risk and focus on protecting accumulated assets.

Step 2: Compare Fund Fees

Fees are a major influence on long-term returns—yet are often overlooked. Even if two funds perform similarly, small differences in fees can make a big difference over decades. Compare fund expense ratios on the MPFA Fund Platform and opt for funds with reasonable costs.

Important Tip: Index-tracking funds (such as passive index funds) generally have lower fees than actively managed funds. Over time, this fee difference can have a significant impact on your net returns.

Step 3: Check Long-Term Performance

Past returns don’t guarantee the future, but reviewing a fund’s longer-term (3 to 10 years) track record gives you an idea of its stability in different markets. Look at 1-, 3-, and 5-year performance, not just single-year results, to make a more balanced judgement.

Step 4: Diversify

Putting all your MPF into a single fund or market increases your risk. Consider spreading your money across different types of funds—such as local and global equities plus bond funds—to cushion your portfolio against diverse market conditions.

Default Investment Strategy (DIS): Is It Right for You?

If you’ve never picked your funds, your contributions are probably following the “Default Investment Strategy” (DIS), nicknamed the “set-and-forget” approach.

How DIS Works

DIS is a life-cycle strategy that automatically shifts your equity-bond mix as you age—focusing on growth assets (equities) when you’re young, and gradually raising the percentage of conservative assets (bonds) as you approach retirement in order to lower portfolio volatility. According to MPFA rules, the fund expense ratio for DIS is capped at 0.95%, so costs are controlled.

Pros and Cons of DIS

DIS is a reasonable starting place for those who don’t want to actively manage their MPF. But it uses a one-size-fits-all approach, which may not match your personal preferences or retirement ambitions. For instance, younger investors who are willing to take more risk might prefer a higher equity allocation to pursue greater potential returns in the early years.

Tax Deductible Voluntary Contributions (TVC): Tax Savings and Growth Benefits

Beyond mandatory contributions, TVC (Tax Deductible Voluntary Contributions) is another powerful savings tool to consider.

The Tax Advantages of TVC

According to Hong Kong Inland Revenue rules, you can claim up to HKD 60,000 of salary tax deduction per year for TVC into your MPF account. With the highest marginal tax rate at 17%, you could save up to HKD 10,200 in tax each year. For regular salary earners, this is a practical way to achieve both retirement savings and tax planning.

Important Notes on TVC

TVC funds must stay invested until age 65 before they can be withdrawn, so liquidity is limited. Make sure you have enough emergency savings before committing extra funds. TVC accounts can be set up under any MPFA-approved scheme, not just your employer’s plan.

Regular Reviews: An Essential MPF Management Habit

Choosing your funds isn’t a one-and-done decision. The market and your personal situation can change over time, so it’s essential to review your MPF portfolio regularly.

When Should You Review Your Portfolio?

It’s recommended to review your portfolio every six months to a year, and also after major life changes, including:

- Significant changes in your job or income

- Entering a new life stage (such as turning 40, 50, or approaching retirement)

- Major market volatility affecting your asset allocation

- Adjustments to your risk tolerance or financial goals

How to Make Use of the “Full Portability” MPF Transfer?

With phased implementation of the MPF “Full Portability” arrangement, new rules will soon allow for greater flexibility. According to the latest 2026 policy, the first phase covers employees who joined on or after May 1, 2025—they will be able to transfer both “employee mandatory contributions” and “employer mandatory contributions” together; employees who joined before this date will be included in a later legislative phase.

Under the new system, “Full Portability” transfers are much more efficient. Thanks to the launch of the eMPF platform, lengthy paperwork is a thing of the past. Eligible employees can simply log in to the eMPF App or online platform and complete the transfer of all accrued benefits electronically, usually within a few working days.

Frequently Asked Questions

Can MPF Be Used to Buy Property?

No. MPF can only be withdrawn in certain circumstances: reaching age 65, early retirement at 60, permanent departure from Hong Kong, total incapacity, terminal illness, or small-balance withdrawal. MPF cannot be used to buy property—a common misconception.

Are Bonuses and Double Pay Subject to MPF Contributions?

Yes. Bonuses and double pay count as “relevant income” for MPF contributions. However, once your monthly salary reaches the HKD 30,000 cap, the monthly MPF contribution limit remains at HKD 1,500—even if you receive bonuses.

What Should I Do with My MPF When I Change Jobs?

After leaving a job, you can keep your accrued benefits in your previous scheme, transfer them to your new employer’s scheme, or move them to a self-selected scheme. The eMPF platform makes managing and consolidating multiple MPF accounts much more convenient.

Do Self-Employed People Have to Contribute to MPF?

Yes. Self-employed people must join an MPF scheme within 60 days of becoming self-employed and contribute 5% of relevant income, subject to the same upper and lower limits as employees.

Conclusion

MPF is a crucial foundation for retirement security in Hong Kong. Instead of letting your contributions run on autopilot year after year, take some time to understand the fund types, assess your risk tolerance, and regularly review your portfolio—so every dollar you save works as hard as possible.

Whether you’re a fresh grad or a seasoned worker with years of contributions, it’s never too late to take an active role in managing your MPF. Investment decisions should be made thoughtfully based on your finances and risk appetite, and continual learning is the foundation of solid financial health.

The right investment tools for you depend on your goals, risk tolerance, market view, and experience. Whatever you choose, make sure you fully understand the mechanisms, risks, and trading rules—and build a robust risk management plan. For more investment insights, you can visit Longbridge Academy or download the Longbridge App.