Singapore Capital Gains Tax: A Key Advantage for Investors

Singapore imposes no capital gains tax on individuals or companies, givinginvestors a significant structural advantage. Here is what you need to know.

TL;DR: Singapore does not impose a capital gains tax on individuals or companies, making it one of the most investment-friendly jurisdictions in the world. Profits from selling shares, Exchange Traded Funds (ETFs), and other financial instruments are generally not taxed — but gains from trading activity may be treated as taxable income by the Inland Revenue Authority of Singapore (IRAS).

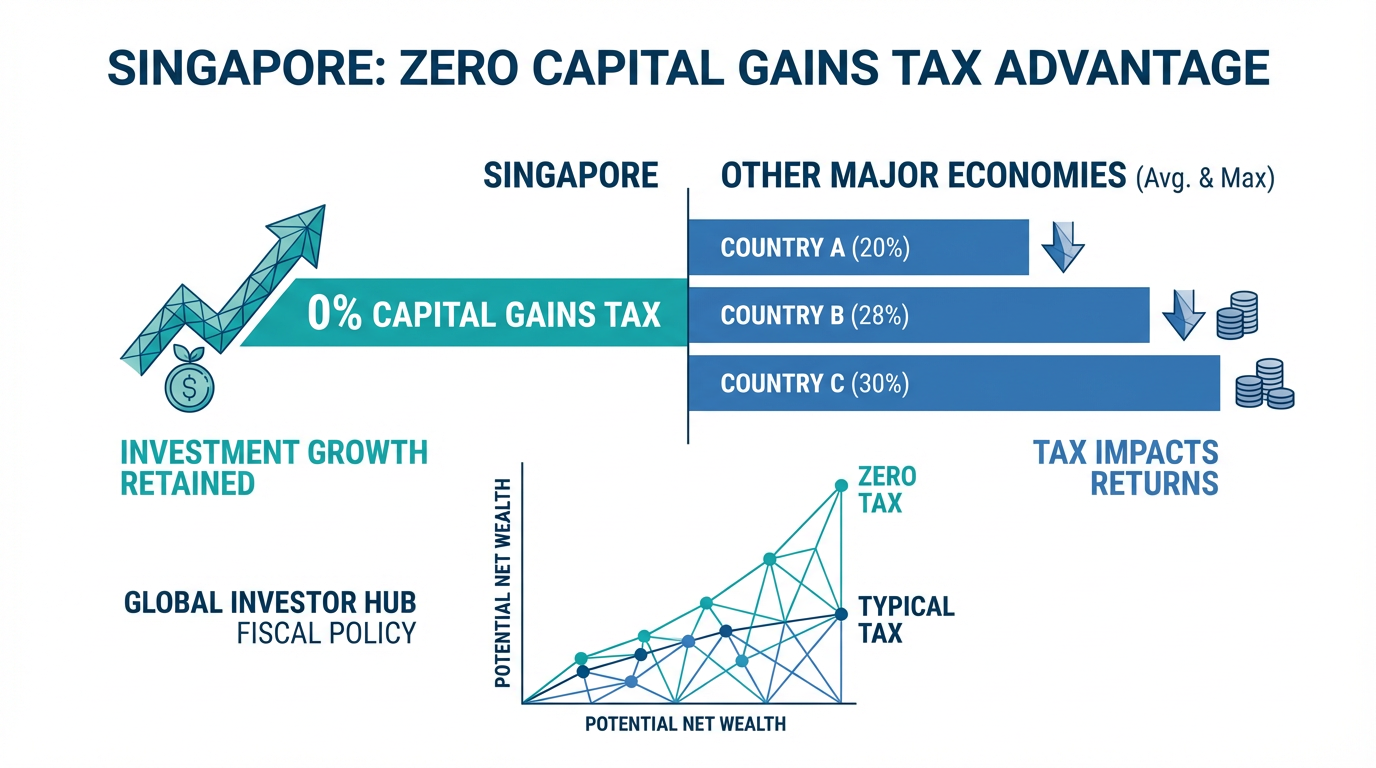

Investors who choose Singapore as their base often cite the absence of a capital gains tax as one of its most compelling advantages. Unlike many developed economies where profits from asset sales attract tax rates of 20% or more, Singapore taxes income rather than wealth accumulation. For retail investors trading stocks, ETFs, Real Estate Investment Trusts (REITs), or other financial instruments, this policy can significantly improve net returns over time. Understanding how the Singapore capital gains tax framework works — and the distinctions IRAS draws — helps investors make more informed decisions about their portfolios.

Singapore's Approach to Capital Gains Tax

Singapore does not have a formal capital gains tax regime, as confirmed by IRAS official guidance. When you sell shares, investment properties, ETFs, or other assets at a profit, those gains are generally not subject to income tax. Singapore's government has deliberately designed its tax system to attract capital and foster long-term investment. By removing capital gains taxation, investors can retain more of their returns and redeploy capital without a tax penalty on each transaction.

How This Differs From Other Countries

To appreciate Singapore's position, consider how other major economies treat capital gains. In the United States, long-term capital gains are taxed at 0% to 20% depending on income level, while short-term gains can reach 37% at ordinary income rates. In the United Kingdom, capital gains tax on both residential property and other assets (including shares) is currently 18% for basic-rate taxpayers and 24% for higher-rate taxpayers, following changes introduced in the October 2024 Autumn Budget (per HM Revenue and Customs 2024/2025 guidance). Singapore's 0% rate stands in sharp contrast, making it a structurally advantageous environment for investors.

The Critical Distinction: Capital Gains vs. Trading Income

While Singapore does not tax capital gains, this does not mean all investment profits are automatically exempt. IRAS makes a clear distinction between capital gains (not taxable) and income from trading (taxable). Getting this distinction wrong can have real financial consequences.

The Badges of Trade Framework

To determine whether your profits are capital or income in nature, IRAS applies the "Badges of Trade" — a set of indicators originally developed in UK tax law and used in Singapore judicial decisions. These factors include:

Frequency of transactions: Buying and selling assets repeatedly over short periods suggests trading rather than investing.

Holding period: Assets sold soon after purchase are more likely to be treated as trading stock.

Profit-seeking intent: If your primary purpose was to sell at a profit rather than hold for income or long-term appreciation, gains may be taxable.

Financing arrangements: Using short-term loans to fund purchases suggests a plan to sell quickly, which points toward trading activity.

Nature of the asset: Certain assets are more commonly associated with trading.

Method of acquisition: How and why the asset was purchased provides context for intent.

No single factor determines the outcome. IRAS looks at the full picture of each investor's situation.

What This Means in Practice

For most retail investors in Singapore who buy shares, ETFs, or REITs with a long-term view and hold them for months or years, the gains upon eventual sale would typically be treated as capital gains and not taxed. Active traders who frequently buy and sell within short time frames face a higher risk of having their gains reclassified as trading income by IRAS.

Tip: If you are uncertain about how your investment activity might be classified, keeping thorough records of your investment rationale, holding period, and transaction history strengthens your position as a genuine investor rather than a trader.

Capital Gains Tax on Shares and Financial Instruments

Singapore's treatment of share disposals is particularly favourable for investors. According to IRAS guidance, gains from selling shares, ETFs, and other financial instruments are generally considered capital gains and are not subject to income tax for individuals.

This applies to Singapore-listed securities on the Singapore Exchange (SGX), as well as shares traded on foreign exchanges. Whether you are investing in blue-chip Singapore stocks, US equities, or Hong Kong-listed companies, the same principle applies: profits from genuine investment activity are typically not taxable.

The Safe Harbour Rule for Companies

For corporate investors, IRAS provides additional certainty through the Safe Harbour Rule. Under this framework, a company's gain from disposing of shares in another company is treated as not taxable if:

The company holds at least 20% of the ordinary shares in the investee company; and

The company has held those shares continuously for at least 24 months prior to disposal.

This rule provides businesses with a clear framework for managing their investment portfolios without uncertainty about tax treatment. From 1 January 2026, the Safe Harbour Rule was extended to cover certain preference shares with equity-like characteristics, such as rights to participate in profits or residual value on exit, rather than fixed returns.

Foreign-Sourced Capital Gains: An Important Update

Capital gains from local asset disposals continue to be non-taxable regardless of when or how they are received. However, from 1 January 2024, a new regime applies to foreign asset disposals. Where an entity within a relevant group disposes of a foreign asset and receives the resulting gains in Singapore, those gains may be treated as taxable income if the entity lacks adequate economic substance in Singapore. Economic substance is assessed based on operational factors including human resources, premises, and business activities.

For individual retail investors, this change is generally not relevant — the economic substance rules target entities within multinational groups. Individual investors continue to benefit from Singapore's capital gains-free environment across both local and foreign investments.

What Singapore's Tax Environment Means for Portfolio Diversification

The absence of capital gains tax creates meaningful opportunities for portfolio diversification. Investors are not penalised for rebalancing their portfolios, taking profits from outperforming positions, or switching between asset classes. In countries with capital gains taxes, the tax cost of rebalancing can act as a drag on portfolio management decisions.

For Singapore investors, this means exploring the full range of investment products across different markets without the tax complexity of asset reallocation in other jurisdictions. Whether you are considering Singapore-listed stocks, US equities, REITs, or ETFs, the framework supports a more active approach to portfolio management. You can explore investment products available on Longbridge across Singapore, US, and Hong Kong markets.

Dividends: A Different Story

While capital gains are not taxed, dividends are treated differently. Singapore does not impose withholding tax on dividends paid by Singapore-resident companies. However, dividends received from foreign companies may be subject to withholding tax in the source country, and foreign dividends remitted to Singapore may attract Singapore income tax in certain circumstances. Income-focused investors should be aware that the tax efficiency of capital gains does not automatically extend to all income streams.

Compliance and Documentation for Investors

Even though capital gains are generally not taxable, maintaining proper records remains important. If IRAS questions whether your gains are capital or trading in nature, documentation supporting your investment intent becomes critical. Practical steps include:

Keeping records of when you purchased each investment and your reasons for buying.

Retaining brokerage statements, trade confirmations, and account records.

Documenting your investment strategy and any changes to it.

Noting the source of funds used to make investments.

If IRAS determines your gains are trading income and you have not declared them, penalties can range from late payment charges to more serious enforcement actions under Singapore's Income Tax Act. Genuinely non-taxable capital gains do not need to be declared in your annual income tax return.

Tip: For peace of mind, investors who engage in frequent or higher-volume trading should consider seeking guidance from a qualified Singapore tax professional to ensure their activity is appropriately classified.

Frequently Asked Questions

Does Singapore have a capital gains tax?

No. Singapore does not impose a capital gains tax on individuals or companies. Gains from selling shares, ETFs, REITs, and property are generally not taxable. The exception is when IRAS determines that the activity amounts to trading rather than genuine investment, in which case profits may be taxed as income.

Do foreigners pay capital gains tax in Singapore?

No. Singapore does not differentiate between residents and foreigners for capital gains treatment. Both are equally exempt under Singapore law. However, the same Badges of Trade apply: if activity is deemed trading rather than investing, gains may be taxable as income.

Are share trading profits taxed in Singapore?

Profits from buying and selling shares are generally treated as capital gains and not taxed. However, if IRAS determines you are carrying on a trade in shares — based on high transaction frequency, short holding periods, and profit-focused intent — those profits may be taxable. Most long-term retail investors fall clearly within the capital gains category.

What about dividend income from shares?

Dividends from Singapore-listed companies are generally exempt from tax for individual investors. Dividends from foreign companies may be subject to withholding tax in the source country, and foreign dividends remitted to Singapore may attract Singapore income tax in certain circumstances.

What is the Safe Harbour Rule for company share disposals?

The Safe Harbour Rule provides certainty of non-taxation for companies disposing of shares where they hold at least 20% of ordinary shares for at least 24 consecutive months. From January 2026, this rule was extended to certain preference shares with equity-like features, providing broader protection for corporate portfolios.

Conclusion

Singapore's absence of a capital gains tax is a genuine structural advantage for investors. The ability to sell shares, ETFs, REITs, and other financial instruments without triggering a tax liability allows investors to focus on performance rather than tax optimisation. The key is understanding the line between capital gains and trading income: investors who buy and hold with genuine investment intent sit comfortably within the non-taxable category, while frequent traders should be aware that IRAS may view their activity differently.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.