CBBC Mandatory Call (MCE) Risk: Lessons from Overnight Total Losses and a Comprehensive Risk-Management Guide

CBBCs’ Mandatory Call (knock-out) mechanism is the core risk that can wipe investors out overnight. This article explains how it works, Category R vs N, and five risk-management tips to fully understand CBBC risks.

TL;DR: The mandatory call mechanism in CBBCs (commonly known as a “knockout”) is the core risk that can take investors to zero overnight. Once the underlying asset’s price touches the call level, the CBBC is terminated immediately, and it will not “come back to life” even if the price later rebounds. Understanding the mandatory call mechanism, the differences between Category R and Category N, and position management are essential basics every investor must grasp before entering the market.

CBBCs (Callable Bull/Bear Contracts) have attracted large numbers of Hong Kong investors thanks to their low entry threshold and high leverage. However, whenever the market swings sharply, some investors suffer heavy losses because their CBBCs hit the call level—sometimes losing their entire principal overnight. How big are the risks in CBBCs? How does the mandatory call mechanism work? This article breaks it down from core mechanics to practical risk management to help you understand the potential pitfalls before you trade.

What are CBBCs?

CBBCs are structured products issued by issuers (typically investment banks) that allow investors to track the price movements of a stock or index at a lower cost, with embedded leverage.

- Bull CBBCs: Used when expecting the underlying asset to rise; if the underlying appreciates, the bull CBBC benefits accordingly

- Bear CBBCs: Used when expecting the underlying asset to fall; if the underlying depreciates, the bear CBBC benefits accordingly

The key differences between CBBCs and derivative warrants (warrants) are that CBBCs have minimal time decay, their prices more closely track the underlying stock or index, and their leverage is theoretically more transparent. Precisely because of this, many investors view CBBCs as “simple and easy to understand,” yet they often underestimate the lethal risk posed by the mandatory call mechanism.

For a structural comparison between CBBCs and warrants, refer to Longbridge Academy’s in-depth analysis of derivatives (https://longbridge.com/en/academy/sp/blog/a-comprehensive-guide-to-callable-bull-bear-contracts-in-depth-analysis-of-the-mandatory-call-mechanism-100007).

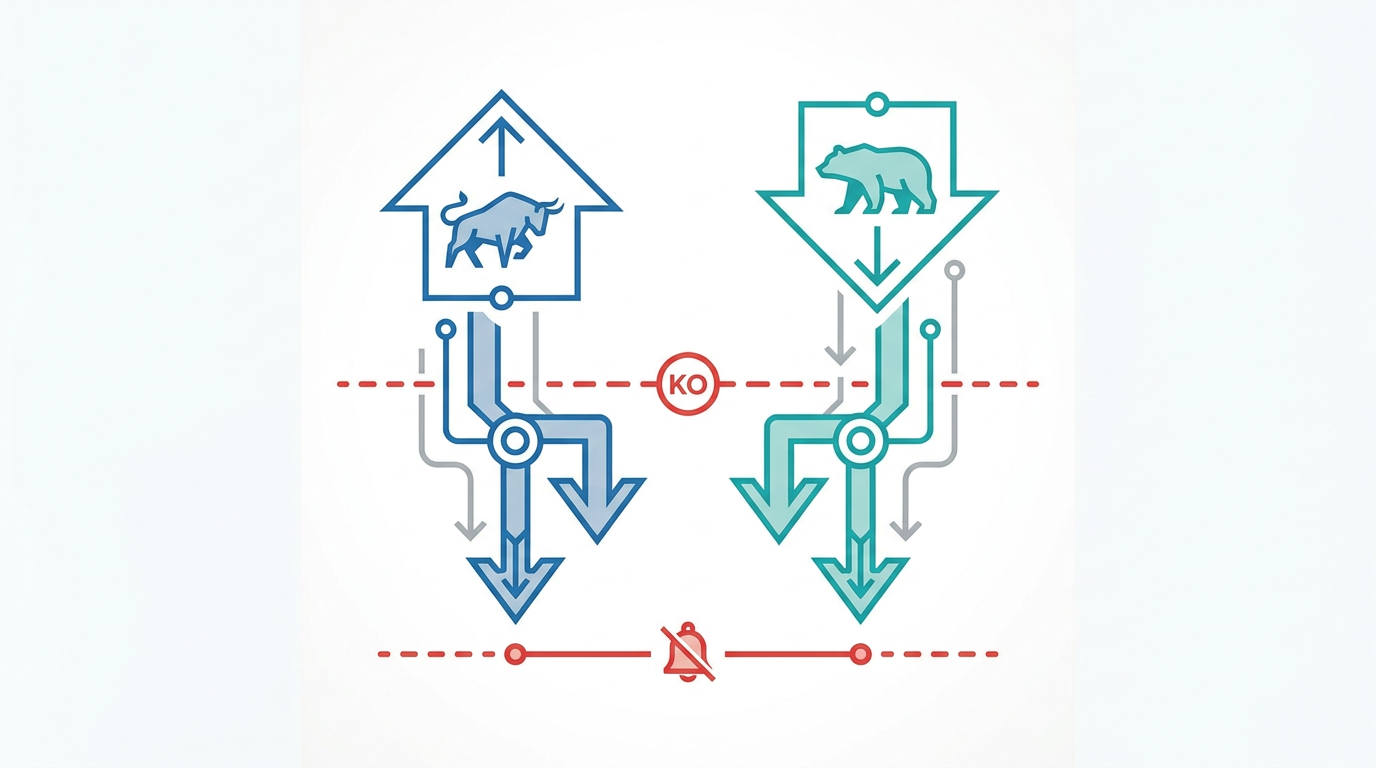

Mandatory Call Mechanism (Knockout): The core of going to zero overnight

The Mandatory Call Event (MCE), commonly known as a “knockout,” is a distinctive—and higher-risk—feature of CBBCs.

Knockout trigger conditions

According to the Hong Kong Exchanges and Clearing (HKEX) explanation on CBBCs (https://www.hkex.com.hk/Global/Exchange/FAQ/Products/Securities/CBBC?sc_lang=en), when the underlying asset’s price touches or surpasses the preset call level during trading hours (including the Pre-opening Session, Continuous Trading Session, and Closing Auction Session), the issuer will immediately trigger a mandatory call and terminate trading of that CBBC:

- Bull CBBC knockout: The underlying price falls to or below the call level

- Bear CBBC knockout: The underlying price rises to or above the call level

Once a knockout is triggered, the CBBC ceases trading immediately. Even if the underlying subsequently rebounds (bull) or retreats (bear), the CBBC will not “revive,” and holders cannot continue to participate in subsequent market moves.

Residual value after a knockout

How much investors can recover after a knockout depends on the CBBC category:

Important reminder: Almost all CBBCs currently circulating in the Hong Kong market are Category R. Category N CBBCs are now rarer, but the risk characteristics of the two differ markedly. Always verify the category before investing.

| Category | Relationship between call level and strike price | Residual value after knockout |

|---|---|---|

| Category N (Nil) | Call level = Strike price (no buffer) | Always zero |

| Category R (Residual) | Gap between call level and strike price (with buffer) | May be small, but could also be zero |

Residual value calculation for Category R CBBCs (hypothetical example):

Take a Category R bull CBBC as an example:

- Call level: 20,000 points; Strike: 19,800 points; Entitlement ratio: 10,000

- Lowest point during the observation period: 19,860 (above the strike)

- Residual value = (19,860 – 19,800) ÷ 10,000 = HKD 0.006

If the lowest point during the observation period falls to 19,800 or below, the buffer is fully penetrated, the residual value becomes zero, and the investor loses the entire principal.

Five major CBBC risks, explained

Beyond the mandatory call, CBBCs also involve multiple layers of risk that investors must not ignore.

Leverage risk

Leverage is a double-edged sword. With 10x leverage, a 1% move in the underlying theoretically leads to a 10% move in the CBBC price. Even small market fluctuations can cause sharp changes in CBBC prices, amplifying losses.

Liquidity risk

When the underlying price swings sharply, the issuer may suspend quoting, making it impossible for investors to sell their positions even before the call level is reached and increasing the risk of being unable to stop losses in time.

Price volatility risk near the call level

As the underlying approaches the call level, bid-ask spreads may widen, market liquidity may thin, and price volatility may intensify, making it difficult for investors to exit at desired prices.

Funding cost risk

Funding costs are embedded in the CBBC issue price and reflect the issuer’s financing costs. The further from maturity, the higher the funding cost, which weighs more on long-term holders.

Issuer credit risk

Per the Investor and Financial Education Council (IFEC) (https://www.ifec.org.hk/web/tc/investment/investment-products/warrants/warrant-trading/things-to-note.page), derivative warrants and CBBCs are not collateralized by the assets of the issuer or guarantor; holders are unsecured creditors of the issuer. If the issuer becomes insolvent or defaults, investors may be unable to recover all or part of the amounts due. Pay attention to the issuer’s credit rating before investing.

What scenarios are most prone to triggering a knockout?

Understanding high-risk scenarios helps investors prepare in advance:

Overnight gap risk

While Hong Kong equities are closed, US markets, futures, and global markets continue to trade. If major news breaks (e.g., geopolitical events or unexpected Fed decisions), the Hong Kong market may open with a large gap the next day, causing CBBCs to be knocked out in the first second of trading—leaving holders virtually no time to react.

Major data release windows

Key releases such as US Nonfarm Payrolls, CPI, and FOMC statements often spark intense volatility over short intervals. Holding CBBCs with call levels close to spot around these times materially increases knockout risk.

Market black swan events

On days of outsized market moves, the number of CBBCs that are mandatorily called is often elevated. While such surprises are hard to predict, investors can reduce the chance of mass knockouts by selecting CBBCs with call levels further from spot.

Five risk-management checkpoints when selecting CBBCs

To mitigate the above risks, investors can use the following approaches:

Distance to the call level

Selecting CBBCs whose call levels are further from the current underlying price (generally 3% to 8%) can lower the chance of unexpected knockouts from sudden events—though leverage will be correspondingly lower.

Control effective gearing

As a general guideline, keep effective gearing in the 5x to 15x range. The higher the leverage, the greater the potential return—but also the higher the risk of losing the entire principal after a knockout.

Ensure sufficient remaining tenor

Holding CBBCs close to maturity will see time value erosion gradually eat into position value even if no knockout occurs. Consider CBBCs with at least one month remaining.

Watch the outstanding ratio

An elevated outstanding ratio (the share of outstanding units held in the market) may cause issuer pricing to be more influenced by supply and demand, widening bid-ask spreads and raising transaction costs.

Set strict stop-loss levels

Before buying CBBCs, predefine the maximum loss you can tolerate (e.g., 20% to 30% of the amount invested). Once the loss hits that cap, close the position immediately to avoid waiting for a rebound and ultimately getting knocked out to zero.

Investment advice disclaimer: The above are general risk-management principles and do not constitute investment advice. Every investor has a different risk tolerance. Understand the product mechanics and potential losses thoroughly before entering the market.

How to check residual value after a knockout?

If you are unfortunately knocked out, you can follow up via:

-

Check the HKEX official website: HKEX provides a “called CBBCs” list on its website, detailing all CBBCs that have been mandatorily called, including the call time, settlement price, and any calculated residual value (if any).

-

Observation period and settlement price: The observation period covers the remainder of the trading session when the mandatory call occurred, as well as the entire next trading session. The lowest point during the observation period (for bull CBBCs) or the highest point (for bear CBBCs) is the settlement price used to compute residual value.

-

Credit timing of residual value: Per common market practice, any residual value is typically credited about five trading days after the call date by the issuer through the Central Clearing and Settlement System directly into investors’ securities accounts; no separate application is required.

Longbridge Securities offers CBBC trading services. Investors can learn more about tradable Hong Kong derivatives on Longbridge’s investment products page (https://longbridge.com/hk/investment-products).

FAQs

Can a CBBC continue trading after a knockout?

No. Once the underlying asset touches the call level, the CBBC stops trading immediately and will not restart. Even if the underlying later rises (bull) or falls (bear) to levels favorable to investors, the CBBC will not “revive” and cannot be traded again.

Does a Category R CBBC always have residual value after a knockout?

Not necessarily. Category R CBBCs may have a small residual value after a knockout, but it can also be zero. It depends on whether, during the observation period, the underlying’s lowest point (bull) or highest point (bear) remains above (or below) the strike. If the underlying further breaches the strike during the observation period, the residual value becomes zero.

Are CBBCs suitable for long-term holding?

Generally, CBBCs are not suitable as long-term investment tools. Although time decay is lower than for warrants, funding costs still accumulate over time and erode position value. CBBCs are better suited for short-term directional trades or as hedging tools rather than long-term holds.

Do overnight headlines before the open affect CBBCs?

Yes. If the market gaps at the open, a CBBC may be knocked out in the first second of trading, leaving holders almost no time to react. This is one scenario where CBBCs can be riskier than warrants—pay particular attention after significant moves in US markets heading into the Hong Kong open.

How can I find a CBBC’s call level information?

You can find details such as call level, strike, maturity date, and leverage on the HKEX website, issuer websites, or brokerage platforms with comprehensive market data. Using Longbridge Market Data (https://longbridge.com/en/markets) lets you track underlying price moves in real time to support decision-making.

Conclusion

The mandatory call mechanism in CBBCs is a double-edged sword: it is an automatic stop-loss embedded in the product design, yet it is also the biggest risk that can wipe investors out overnight. Understanding the trigger conditions for mandatory calls, the differences between Category R and Category N, and how residual value is calculated during the observation period is essential knowledge for every CBBC trader.

Which tool you choose depends on your investment objectives, risk tolerance, market view, and experience. Regardless of the instrument, you must fully understand its mechanics, risk profile, and trading rules, and establish a robust risk-management plan. You can learn more through Longbridge Academy (https://longbridge.com/en/academy) or by downloading the Longbridge App (https://longbridge.com/hk/download).