Margin Interest Rates: Understanding US Leverage Costs

Margin interest rates are the daily borrowing costs you pay when trading on leverage. This guide explains how they are calculated, what drives them, and how to manage the risks.

TL;DR: Margin interest rates are the borrowing costs you pay when using funds borrowed from a broker to trade. These rates typically range from 5% to 12% per year in the US market, accrue daily, and are closely tied to US Federal Reserve policy. Understanding these costs is essential before using leverage in your investment strategy.

Borrowing money to invest can amplify both your returns and your risks. When you trade on margin, your broker extends a loan secured by the assets in your account, and you pay margin interest rates on the borrowed amount. For Singapore investors accessing US markets, understanding these leverage costs is a core part of managing your overall trading expenses.

This guide explains what margin interest rates are, how they are calculated, what drives them, and what risks you should weigh before activating a margin account.

What Are Margin Interest Rates?

A margin interest rate is the annual interest charged by a broker on funds you borrow through a margin account. When you deposit securities or cash as collateral, your broker effectively gives you a loan to purchase additional securities. The interest rate on that loan is the margin rate.

Margin rates are quoted as an annual percentage rate (APR) but charged on a daily basis. This means your actual borrowing cost depends on both the stated rate and how long you hold the position open.

How a Margin Account Works

To open a margin account in the US market, brokers generally require a minimum deposit, often USD 2,000 or more. Under Regulation T, established by the US Federal Reserve Board, you can borrow up to 50% of the purchase price of eligible securities. So if you want to buy USD 10,000 worth of shares, you need at least USD 5,000 of your own capital.

Once your position is open, you also need to maintain a minimum level of equity in your account, typically around 30% of the current market value of your holdings. If your account falls below this threshold, your broker may trigger a margin call, requiring you to deposit more funds or sell assets to restore balance.

Margin Rates vs. Other Borrowing Costs

Compared to unsecured credit, margin rates can be lower. Credit card annual percentage rates in the US averaged between 22% and 24% in late 2024, according to Federal Reserve data, while margin rates typically ranged from 5% to 12% annually during the same period. However, the risks in leveraged investing are very different from ordinary consumer borrowing.

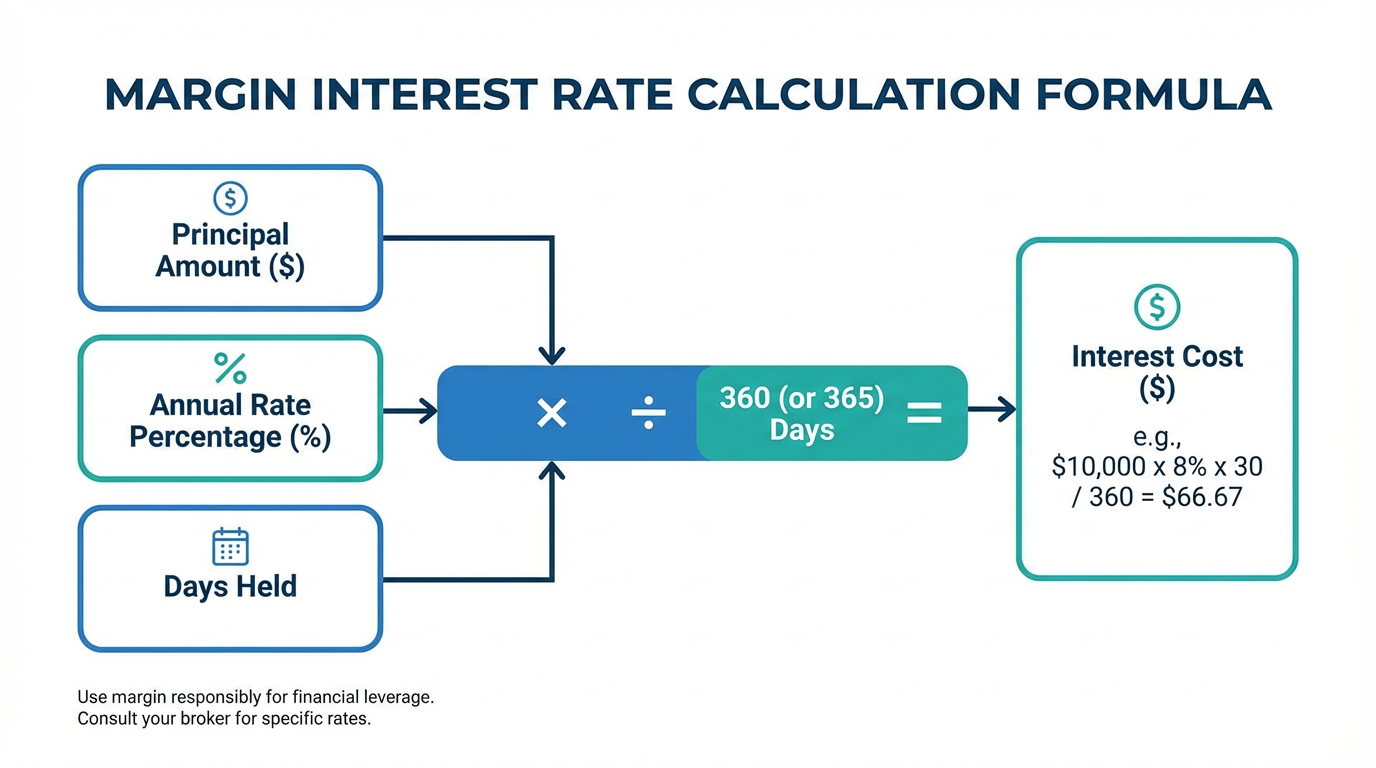

How Are Margin Interest Rates Calculated?

Understanding the calculation method helps you estimate your actual cost of carry before entering a leveraged trade.

The Basic Formula

Most brokers calculate daily margin interest using a standard formula:

Daily Interest = Principal Borrowed x (Annual Rate / 365)

To find your total cost for a given period, multiply the daily interest by the number of days you hold the position.

Example: If you borrow USD 20,000 at an annual margin rate of 8%, your daily interest charge is approximately USD 4.38 (that is, USD 20,000 x 8% / 365). Hold that position for 30 days, and you owe roughly USD 131 in interest. Hold it for 90 days, and the cost climbs to around USD 394.

Some brokers use 360 days instead of 365 for their calculations. The difference is minor but worth checking in your broker's terms.

Tiered Rate Structures

Most US brokers apply a tiered pricing model, meaning the interest rate decreases as your borrowed balance increases. A typical structure might look like:

-

Balances under USD 25,000: base rate plus a higher spread

-

Balances between USD 25,000 and USD 100,000: base rate plus a moderate spread

-

Balances over USD 100,000: base rate plus a smaller spread

This means smaller accounts generally pay higher effective rates than larger ones. The exact spread above the base rate varies by broker, so reviewing each broker's published margin rate schedule is the most reliable way to compare costs.

When Is Interest Charged?

Interest accrues daily and is posted to your account monthly, beginning from the date the credit is extended. Even after you sell a position, any remaining debit balance continues to accrue interest until fully paid down.

What Drives Margin Interest Rates?

Several factors influence the rate you pay on a margin loan.

US Federal Reserve Policy

The primary driver is the US Federal Reserve's federal funds rate, the benchmark rate at which banks lend to each other overnight. When the Federal Reserve raises interest rates, as it did from 2022 to 2023, brokers typically pass higher borrowing costs on to margin traders within weeks. During that period, margin rates at many US brokers rose from under 3% to the range of 8% to 12%.

The Base Rate Framework and Market Conditions

Brokers establish an internal base lending rate influenced by the federal funds rate, the prime rate (the rate banks charge their most creditworthy customers), and other commercial benchmarks. They apply a markup or markdown based on your account balance tier. During periods of elevated market volatility or high borrowing demand, rates can also rise as the risk profile of margin lending increases.

Understanding the Hurdle Rate and Risk

One concept that experienced traders use when evaluating margin is the hurdle rate. This is the minimum return your investment must generate simply to cover the cost of borrowing.

If your annual margin rate is 8%, your leveraged position must return more than 8% per year just to break even on the interest expense. This is before accounting for any transaction costs, currency exchange fees, or taxes.

The Amplification Effect

Leverage amplifies outcomes in both directions. If you invest USD 10,000 of your own capital and borrow another USD 10,000 at 8% per year, a 10% gain on the total USD 20,000 position yields USD 2,000, minus approximately USD 800 in annual interest, leaving USD 1,200 net — a 12% return on your own capital. But if the position falls 10%, you lose USD 2,000 plus interest, producing a net loss of roughly USD 2,800 on your own USD 10,000 — a 28% loss. (This example is for illustration purposes only and does not constitute investment advice.)

Margin Calls and Forced Liquidation

A margin call occurs when your account equity drops below the maintenance margin requirement, typically around 30% of the current market value of your holdings. At this point, your broker will demand that you deposit additional funds or securities. If you are unable to meet the call, the broker has the right to sell your positions without prior notice to bring the account back into compliance.

This forced liquidation can lock in losses at the worst possible time, during market downturns when prices are already falling. Understanding this mechanism is critical before using leverage.

Important: Margin trading involves substantial risk. You can lose more than your initial deposit, and losses are not capped at the value of your collateral. Always assess your risk tolerance and financial position carefully before using leverage.

Practical Considerations for Investors

Before activating a margin account, there are a few key principles to apply.

Calculate Your Cost of Carry

Determine whether the expected return from your position needs to exceed your margin interest rate. For example, if an asset has historically returned 6% annually and your rate is 8%, the borrowing cost would exceed the historical return, all else being equal.

Position Duration Matters

Margin costs accumulate over time. Day traders who close positions before the close of the market often pay minimal interest. For longer-term positions, accumulated interest becomes a meaningful drag on returns. The longer you hold a borrowed position, the higher your total cost.

Maintain an Equity Buffer and Review Your Rate Schedule

Never borrow against the full value of your eligible assets. Leaving a cash buffer gives you room to absorb price moves without triggering a margin call. Also review your broker's full rate schedule, including the base rate and tiered spreads, and check whether a netting policy applies, where cash in a linked account offsets your margin debit.

For those interested in accessing the US market with transparent pricing, you can review Longbridge's pricing information to understand available fee structures.

Margin Trading in the US Market: Key Points for Singapore Investors

For Singapore-based investors accessing US stocks, exchange-traded funds (ETFs), and options, margin rates are quoted in US dollars. Exchange rate movements between the Singapore dollar and the US dollar can add an additional layer of cost depending on how rates shift.

Platforms licensed by the Monetary Authority of Singapore (MAS) operate under regulatory frameworks covering risk disclosures, margin call procedures, and client asset protection. Verifying MAS licensing provides an important baseline for investor protection.

Longbridge, as an MAS-licensed digital brokerage, provides access to US market investment products including stocks, ETFs, REITs, and options. You can also use Longbridge's market data and quote-tracking tools to stay informed before making margin-related decisions.

Frequently Asked Questions

What is a typical margin interest rate for US stocks?

Margin interest rates for US stocks typically range from 5% to over 12% per year, depending on your account balance and the broker you use. Larger accounts generally receive lower rates through tiered pricing. Rates are directly influenced by the US Federal Reserve's benchmark interest rate decisions.

How is margin interest charged?

Interest accrues daily from the date you open a margin position and is posted monthly. The daily rate is calculated by dividing the annual percentage rate by either 360 or 365, then multiplying by your outstanding borrowed balance.

What happens if I get a margin call?

A margin call is issued when your account equity falls below the maintenance requirement, commonly around 30% of your position value. You must deposit additional funds or securities, or sell holdings to restore your equity. If you do not act in time, the broker can liquidate your positions without prior notice.

Can margin interest be reduced?

Yes. A larger account balance, a broker with competitive tiered rates, and shorter holding periods can all reduce your total interest costs. Some brokers also apply netting policies where cash in your account offsets your margin debit.

Is margin trading suitable for beginners?

Margin trading is generally not recommended for new investors. The combination of interest costs, maintenance requirements, and the risk of losses exceeding your initial investment requires a sound understanding of markets and risk management. The Longbridge Academy offers educational resources to help build this foundation.

Conclusion

Margin interest rates represent the direct cost of using leverage when trading in financial markets. They are calculated daily, tied closely to US Federal Reserve monetary policy, and vary across brokers based on account size and competitive positioning. For Singapore investors accessing US markets, understanding these rates is a prerequisite for evaluating whether any leveraged strategy makes financial sense.

The key principles are straightforward: calculate your hurdle rate, size your position with a buffer, and be prepared for the possibility of a margin call. Leverage can be a useful tool in certain market conditions, but it also magnifies risks proportionally with potential gains.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.