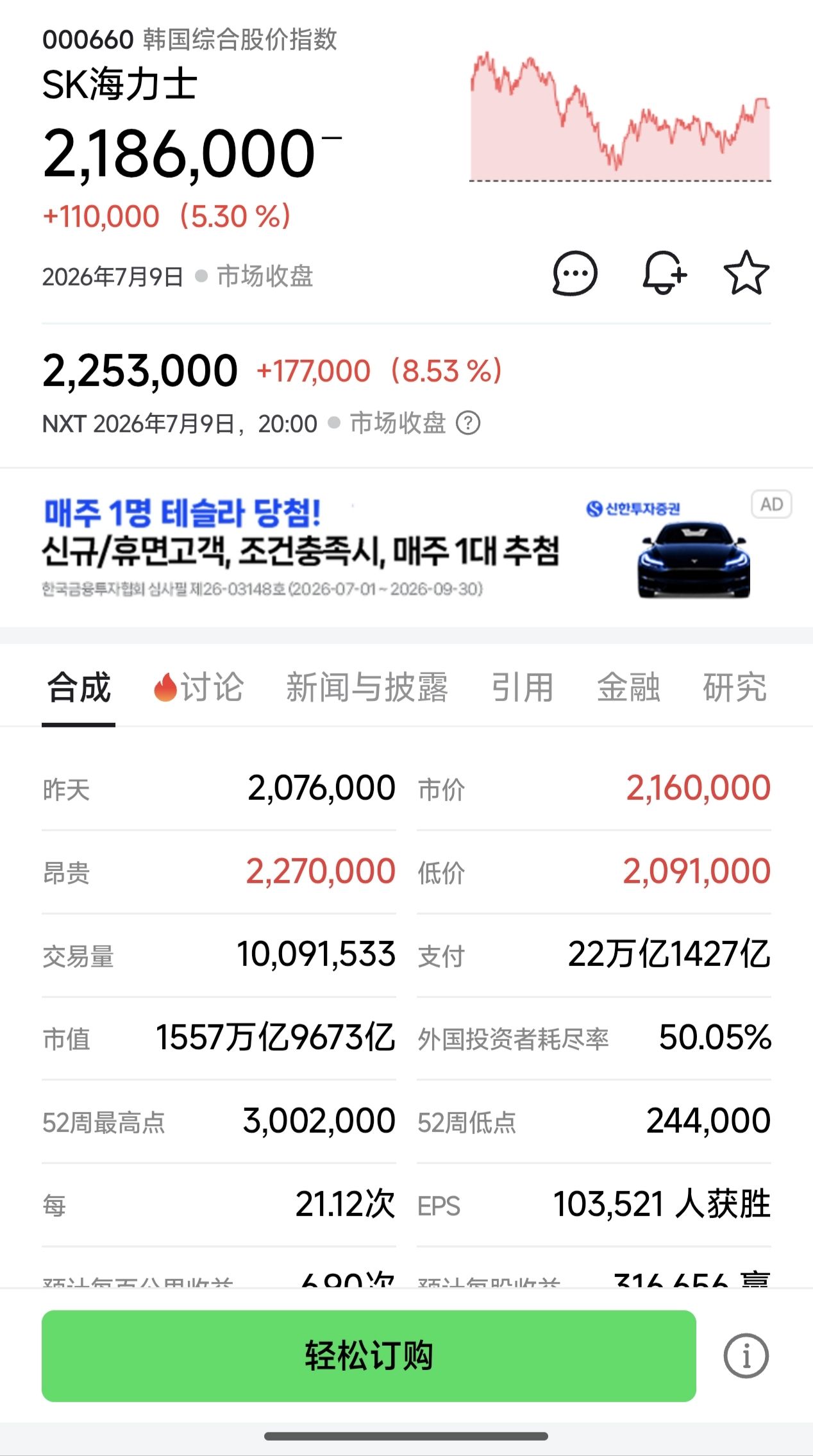

$XL2CSOPHYNIX(07709.HK) Let's understand the cross-market arbitrage principle behind this wave of institutional activity (summarized using Doubao). It's also a study note for myself. Please correct me if I'm wrong.

Basic premise: 10 US-listed ADRs = 1 South Korean Hynix stock; Before 7.29, only ADRs could be converted into Korean shares, but Korean shares could not be made into ADRs, so US shares could remain more expensive than Korean shares, with the price gap widening.

Phase 1: Today ~ 7.28 (Channel not fully open, profiting from the "widening price gap")

Institutional Operation

Buy ADRs in the US market (long), while simultaneously borrowing and selling Korean shares via futures/margin lending in South Korea (short Korean shares), with positions of equal market value on both sides.

How to guarantee profit? Not relying on stock price movements, only looking at which rises more.

1. Scenario 1: US shares surge, Korean shares rise slightly

Profit from ADRs > Loss from shorting Korean shares, net profit from the widening gap.

2. Scenario 2: US shares dip slightly, Korean shares plunge

Profit from shorting Korean shares > Loss from ADRs, still net profit.

3. Scenario 3: Both sides move up/down in sync and by the same magnitude

Long and short positions offset, no loss, holding to wait for the gap to continue widening.

Core Logic

Because the policy blocked the path of "turning cheap Korean shares into ADRs to dump on the US market," speculative funds in the US market will only keep pushing ADR prices higher. The price gap between the two markets will only keep expanding, allowing institutions to steadily capture the gains from premium expansion.

Phase 2: On 7.29, the day the channel opens, profiting from the "direct elimination of the price gap" - the ultimate profit.

Preparatory groundwork (institutions have already positioned themselves)

Before 7.28, a complete portfolio was established: holding a bunch of expensive ADRs, while owing a bunch of borrowed Korean shares for the short position.

Complete closed-loop operation (see how to make money in one step)

1. Institutions surrender their expensive US ADRs to the custodian bank for cancellation (cancellation is not for cash, but to convert into an equivalent amount of Korean shares);

2. The bank gives the institutions the corresponding number of Korean shares, which are exactly used to return the Korean shares previously borrowed for shorting, closing the short position directly;

3. Accounting: Initially sold Korean shares at a low price to get a sum of money, bought ADRs at a high price spending another sum, pocketing the huge price difference in between;

Why did Korean shares plunge on 7.29?

All market institutions uniformly canceled ADRs on the same day, converting and receiving a massive amount of Korean shares in bulk to return borrowed shares. A huge wave of Korean share sell orders suddenly flooded the market, driving the price down. Simultaneously, with massive ADR cancellations and reduced circulation, the US share price also fell, causing the high price gap between the two markets to disappear rapidly.

Underlying profit principle

Previously, US shares were 50% more expensive than Korean shares, meaning the same asset was priced significantly differently in the two markets. With the conversion channel available on 7.29, institutions directly exchanged their expensive US share certificates for cheap Korean shares to repay their debt, capturing the entire price difference in between. This is an almost risk-free closing arbitrage.

One-sentence summary

1. Before 7.29: Buy US shares, short Korean shares, bet that US shares remain more expensive than Korean shares, profit as the gap widens;

2. On 7.29: Cancel the expensive US ADRs and convert them into Korean shares, use them to repay the shares borrowed for shorting, capture the entire price difference profit in one go; The massive amount of converted shares are sold off collectively, directly suppressing the Korean share market.