Company Encyclopedia

View More

Siteone Landscape Supply

SITE.US

SiteOne Landscape Supply, Inc., together with its subsidiaries, engages in the wholesale distribution of landscape supplies in the United States and Canada. The company provides irrigation products, including controllers, valves, sprinkler heads, irrigation pipes, micro irrigation, and drip products; fertilizer, grass seed, and ice melt products; control products, such as herbicides, fungicides, rodenticides, and other pesticides; hardscapes, which includes pavers, natural stones, blocks, and other durable materials; landscape accessories that include mulches, soil amendments, drainage pipes, tools, and sods; nursery goods, which consist of deciduous and evergreen shrubs, ornamental, shade, evergreen trees, field grown and container-grown nursery stock, roses, perennials, annuals, bulbs, and plant species and cultivars; and outdoor lighting products that include lighting fixtures, LED lamps, wires, transformers, and accessories. It also offers consultative services consisting of assistance with irrigation project take-offs, commercial project planning, generation of sales leads, business operations, and product support services, as well as a series of technical and business management seminars; and distributes branded products of third parties. In addition, the company provides plant varieties under the Portfolio brand; and natural stone under the Solstice brand name.

756.12 B

SITE.USMarket value -Rank by Market Cap -/-

Valuation analysis

P/E

1Y

3Y

5Y

10Y

P/E

-

Industry Ranking

-/-

- P/E

- Price

- High

- Median

- Low

P/B

1Y

3Y

5Y

10Y

P/B

-

Industry Ranking

-/-

- P/B

- Price

- High

- Median

- Low

P/S

1Y

3Y

5Y

10Y

P/S

-

Industry Ranking

-/-

- P/S

- Price

- High

- Median

- Low

Dividend Yield

1Y

3Y

5Y

10Y

Dividend Yield

-

Industry Ranking

-/-

- Dividend Yield

- Price

- High

- Median

- Low

Institutional View & Shareholder

Analyst Ratings

- Price--

- Highest--

- Lowest--

News

View More

Posts

View More

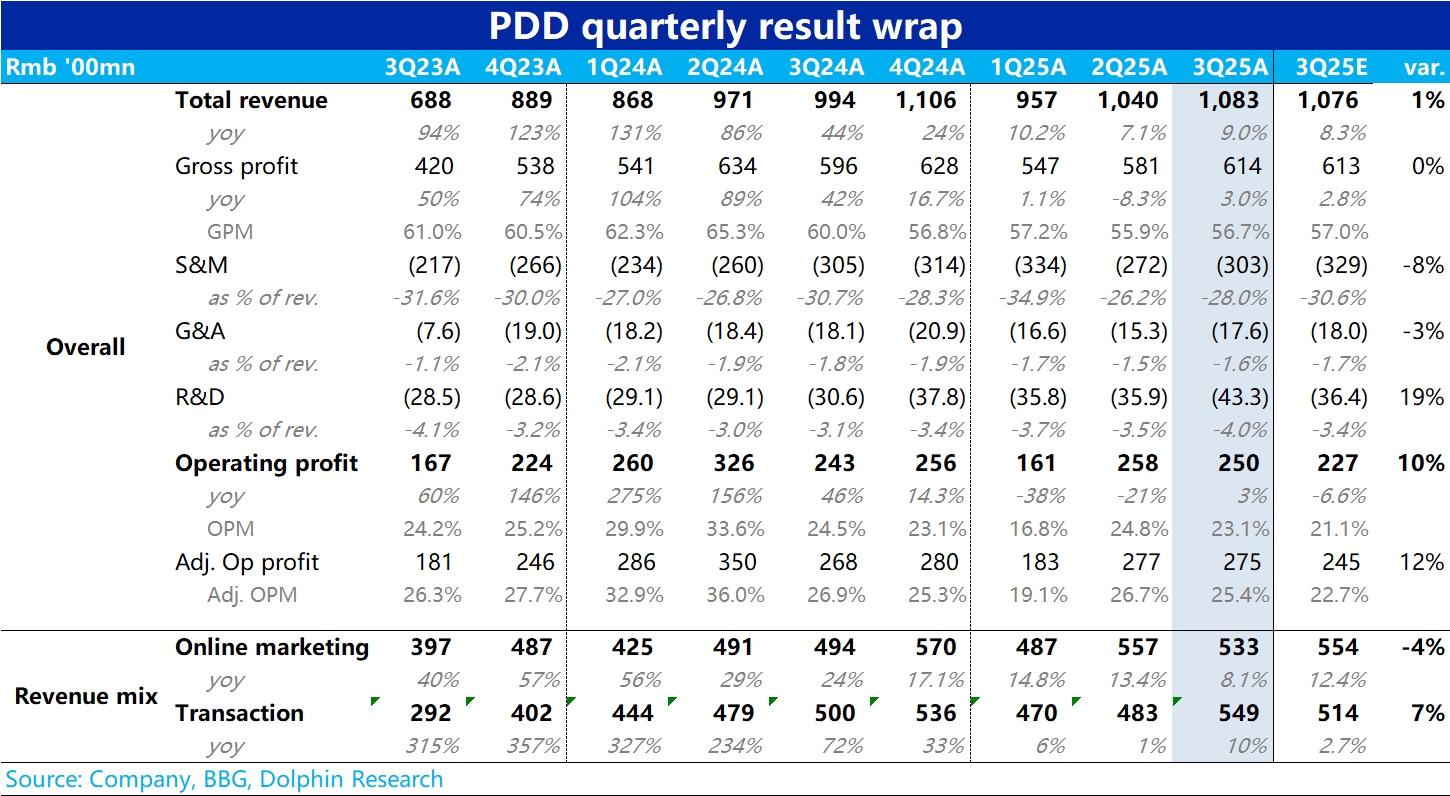

Pinduoduo 3Q25 Quick Interpretation: The performance of Pinduoduo, which was once unpredictable with its stock price often experiencing sharp rises and falls, has now become increasingly stable and "p...