JUNDA: Institutional consensus + cyclical turning point, a rare "distress reversal" target

The leading A-share photovoltaic cell company Junda Co., Ltd. is launching an IPO in Hong Kong, likely becoming the first A+H company in the PV industry. Its fundamentals and valuation show some highlights, especially the industry's new developments which are highly noteworthy.

Below is a detailed analysis, systematically dissecting the core logic of Junda's Hong Kong IPO based on capital signals, industry fundamentals, and the company's operational inflection points.

1. Broker Target Prices Imply 70%+ Upside, with National Team and Foreign Capital Signaling Strong Bullish Sentiment

For Junda's Hong Kong listing, the midpoint price of HKD 24 represents a more than 40% AH discount compared to its A-share price of around RMB 40, equivalent to a 60% discount, which is somewhat attractive.

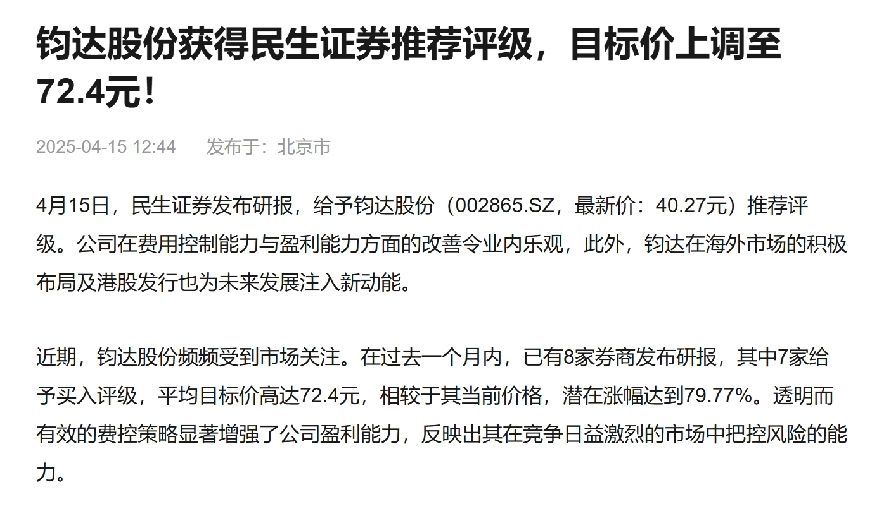

From late last year to Q1 this year, brokers have been aggressively recommending Junda. Public data shows an average target price of around RMB 72, while the current A-share price is about RMB 40, implying at least a 70% upside by 2025. Factoring in a 2026 PE of just 6x and the 40% Hong Kong discount, the potential upside could be even greater.

Beyond sell-side enthusiasm, Q1 buy-side fund flows have also signaled strong bullish momentum.

The National Social Security Fund 118 Portfolio newly established a 4.57% position in Junda during Q1 2025, making it the fourth-largest shareholder—a rare level of commitment. Historically, the moves of such state-backed long-term capital have been market bellwethers, with median three-year returns exceeding 200% for their heavy holdings.

Northbound capital, representing foreign investment trends, has seen three consecutive months of net inflows into Junda, with Hong Kong Stock Connect holdings rising from 2.3% at the start of the year to 4.1%, indicating long-term capital is positioning counter-cyclically.

The unanimous optimism among major institutions about Junda stems from the market's "smart money" often front-running cyclical inflection points. This consensus is no coincidence—it reflects the dual resonance of anticipated PV industry cyclical recovery and the company's turnaround potential.

2. Capacity Clearance Nears Completion, PV Industry Bottoming Signals Emerge, Ushering in a New Cycle of Supply-Demand Rebalancing.

To analyze Junda, one must discard traditional value-investing mindsets like "avoid losses" or "shun low profitability" and instead adopt a cyclical stock framework.

Historically, every post-overcapacity supply-side clearance has triggered subsequent "Davis Double Plays" for industry leaders. Like any cyclical sector, the PV industry is now replicating this pattern, with its fluctuations driven by technological iterations and supply-demand mismatches.

After the brutal 2023-2024 shakeout, price wars pushed industry-wide gross margins to historic lows. In 2024, N-type cell prices briefly plunged to RMB 0.28/W (vs. a peak of RMB 1.28/W), leaving the entire sector unprofitable.

But by Q1 2025, capacity clearance is nearing its end, heralding a "last-man-standing" era. CPIA data shows cell prices began stabilizing and rebounding in Q4 2024, with per-watt profits recovering. In Q1 2025, TOPCon high-efficiency capacity utilization rose to 60% (vs. 45% in Q4 2024), while outdated PERC capacity accelerated its exit, creating structural shortages in TOPCon supply.

Junda's edge lies in its early bet on TOPCon. Back in 2023, it fully impaired its P-type PERC capacity, pivoting decisively to N-type TOPCon. Today, over 90% of its 44GW capacity is N-type, with mass-production efficiency reaching 26.3%, above the industry average.

Policy tailwinds further bolster this: new N-type cell efficiency must now meet a 26% threshold, which Junda already achieves—a feat few peers can match. This technological moat grants stronger pricing power during profit recovery.

The "capacity clearance + tech transition" dynamic mirrors the 2019 hog cycle and 2020 lithium cycle bottoms, where Muyuan Foods surged 500% post-African swine fever and Tianqi Lithium gained 10x despite price crashes.

History shows that firms bold enough to innovate at cycle troughs often reap the next upcycle's richest rewards—especially leaders who endure losses to advance tech and globalize, ultimately capturing 超额收益 during demand rebounds.

At this juncture, Junda shares the "distress-to-prosperity" DNA of Muyuan and Tianqi.

3. Global Breakout + Tech Leadership Cement Junda's N-Type Moat, with 2025 Profitability Marking Its Turnaround

Beyond industry cyclical signals, the bullish case rests on Junda's own improving fundamentals, driven by "global capacity + tech premium" dual engines.

On globalization, Junda's overseas push is bearing fruit in two ways:

First, overseas sales now dominate (58% in Q1 2025 vs. 23.85% in 2024), insulating it from domestic price wars. Key markets like India, Turkey, and Europe offer 20-30% higher per-watt profits.

Second, its 5GW Oman project (year-end 2025 投产) will serve high-margin Middle Eastern/European markets, with just 10% U.S. tariffs (vs. 32-48% for Southeast Asia), lifting gross margins toward 15%+.

Technologically, Junda leads in TOPCon while prepping perovskite/BC tech. Its 海外 premium (RMB 0.34/W, 20% above domestic) and 订单 visibility into 2026H1 reflect this. Oman's full operation could deliver >RMB 1bn 2026 net profit—justifying 机构 consensus.

Notably, its R&D intensity (4.2% vs. industry 3.5%) and 200+ patents underpin xBC (efficiency +1-1.5%) and perovskite 叠层 (lab 效率 31%) pipelines, ensuring future tech competitiveness.

Conclusion

Junda meets both "turnaround" criteria: cyclical inflection + sector leadership. Like Muyuan/Tianqi, today's PV sector offers maximal "expectation gaps" and optimal risk-reward.

At 券商 average 2025 target of RMB 70 (70% upside), plus 港股's 40% discount (8x 2025 PE), potential 港股 upside could reach 100%. Post-listing 港股通 inclusion (within a month) may further boost liquidity.

When N-type tech gaps, globalization, and 港股通 flows converge, cyclical forces will reward those who believed during the darkest hours—why not take a small position? $DRINDA(02865.HK) $CATL(300750.SZ)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.