Volkswagen Group's operating profit of 6.7 billion euros in the first half of 2025 shows a significant year-on-year decline | Financial Report Analysis

Produced by Zhineng Auto

In the first half of 2025, Volkswagen Group delivered a half-year report with complex signals: revenue remained basically flat, but core profit indicators declined significantly. Pre-tax profit fell by 36% year-on-year, cash flow turned negative, and the two key transformation businesses of software and batteries continued to incur losses. The much-anticipated CARIAD and PowerCo failed to turn positive.

Behind these numbers is a structural imbalance exposed by a century-old industrial giant during the industrial transition cycle: it must maintain the steady state of traditional businesses while betting huge costs on future technologies, and at the same time face external shocks from geopolitical policies in the US and China markets.

This imbalance is not only present in the financial figures but also permeates its brand matrix and organizational structure. The pace of advancement of sub-brands in the paths of intelligence and electrification is out of sync, and the software platform has not been integrated, resulting in low internal resource coordination efficiency.

Volkswagen Group, which profits from the US and China markets, faces excessive load on the cost center in Europe due to profitability pressures in key markets, putting pressure on the pace of transformation.

Part 1

From Stability to Pressure:

Operating Profit of 6.7 Billion Euros

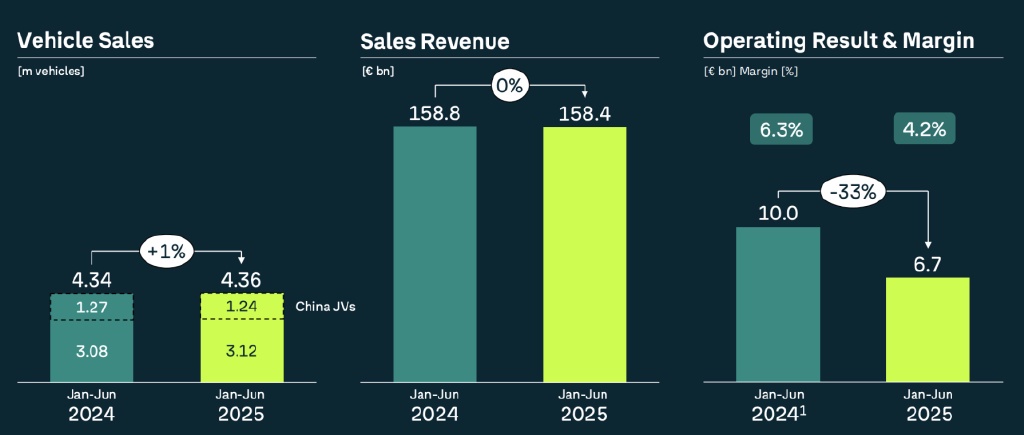

In the first half of 2025, Volkswagen Group achieved revenue of 158.4 billion euros, a year-on-year decrease of only 0.3%, maintaining overall scale stability, but profitability showed a significant decline.

◎ Operating profit: 6.7 billion euros, operating profit margin 4.2%; excluding US tariffs, restructuring, and diesel-related costs, the profit margin is 5.6%(in line with the full-year original expected range). The adjusted profit margin for H1 2024 was 6.3%, a year-on-year decrease.

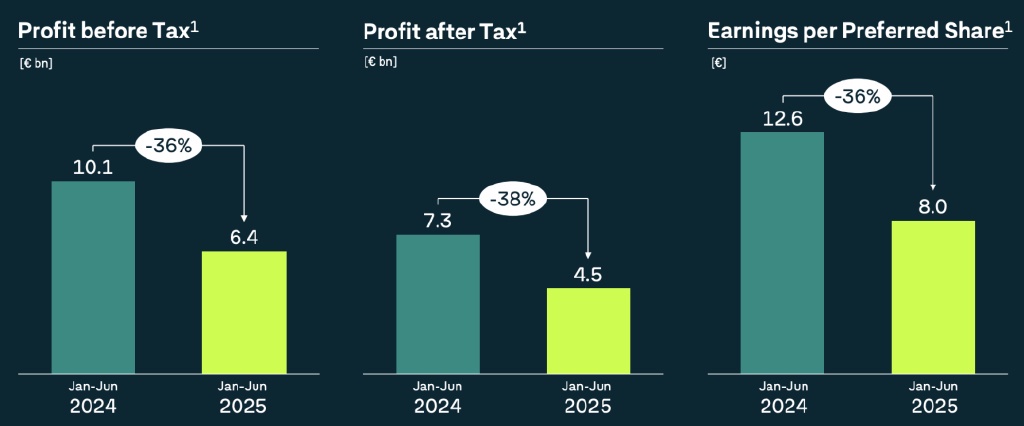

◎ Pre-tax profit: 6.4 billion euros, a year-on-year decrease of 36%(H1 2024 was 10.1 billion euros);

◎ Post-tax profit 4.5 billion euros, a year-on-year decrease of 38%.

There are three direct factors causing the profit decline:

◎ The first is the drastic change in US tariff policy, especially the 1.2 billion euro tariff expenditure in the second quarter, which forced the full-year profit margin forecast range to be lowered;

◎ The second is the one-time expenditure brought about by internal restructuring and layoff plans, including CARIAD layoffs and the implementation of the "Future Volkswagen" plan;

◎ The third is the structural challenges of the BEV business. Although sales increased by 47% year-on-year, profitability is insufficient, and it is facing a difficult transition from sales-driven to efficiency-driven.

In terms of cash flow

◎ The net cash flow of the automotive business in H1 was -1.4 billion euros. Excluding mergers and acquisitions and diesel issues, it only achieved a slight positive inflow, showing that the capital side is squeezed by new investments(such as additional investment in Rivian)and old burdens(such as dieselgate costs).

◎ Net liquidity decreased from 34.4 billion at the beginning of the year to 28.4 billion euros, below the lower limit of the mid-term target range.

◎ Quarterly, the Q1 profit margin was 3.7%, and Q2 temporarily rebounded to 4.7% due to the concentrated release of tariffs.

At the brand level

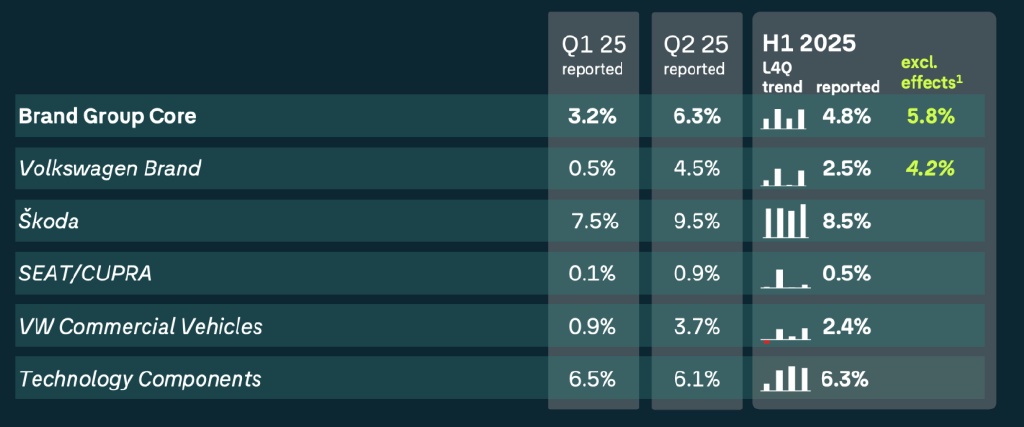

◎ The core brand group(Volkswagen, Skoda, etc.)saw a 2.6 percentage point increase in profit margin driven by product structure optimization and regional market recovery.

◎ Audi still shows weakness in cost control, with a Q2 profit margin of only 3.2%.

◎ Porsche was affected by declining sales and high investment, with the profit margin falling to 1.9%, a decrease of more than 11 percentage points compared to the same period last year.

The differentiation trend reflects the uneven progress of the brand matrix in the technical transformation path. Volkswagen is encountering organizational inertia and investment imbalance issues in the transition from "scale-driven" to "efficiency-driven".

In the first half of the year, Volkswagen delivered 4.4 million vehicles worldwide, a slight increase of 1% year-on-year, maintaining a global market share of about 10%.

In terms of pure electric vehicles, significant progress was made, with delivery volume increasing by 47% year-on-year. The main models include ID.4/5(85,000 units), ID.3(61,000 units), and Q4 e-tron(45,000 units).

In Western Europe, demand for electric vehicles is strong, with order volume increasing by 62% year-on-year, and orders can be scheduled until the fourth quarter of 2025.

By region

◎ The European market grew by 2%, and South America performed well with an 18% increase;

◎ However, the Chinese market declined by 2%, and North America fell by 7%.

Overall, Volkswagen continues to accelerate in electrification, and although some regions are under pressure, global deliveries remain stable.

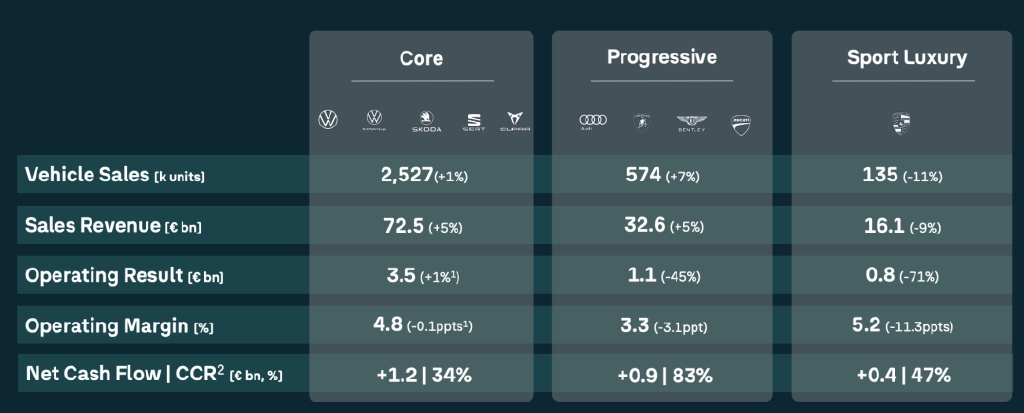

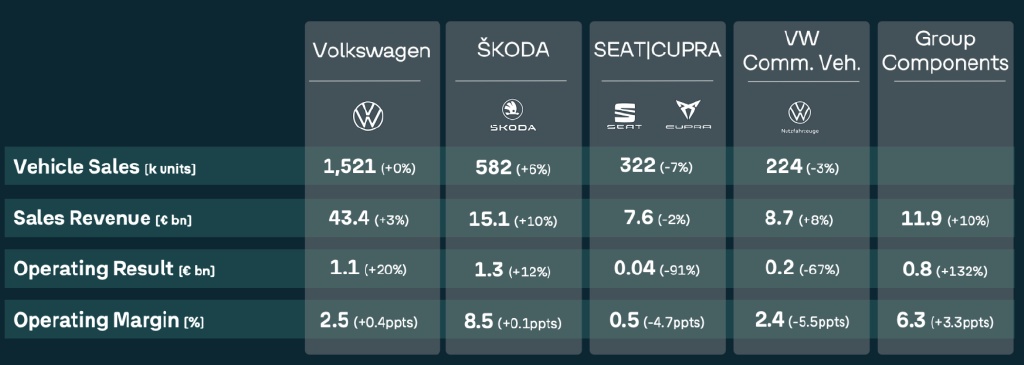

In the first half of this year, the core brands under the Volkswagen Group(such as Volkswagen, Skoda, etc.)sold a total of 2.527 million vehicles, a year-on-year increase of 1%, achieving revenue of 72.48 billion euros, with an operating profit of 3.455 billion euros and a profit margin of 4.8%.

Among them, Skoda performed well with a profit margin of 8.5%; in contrast, SEAT/CUPRA's profit margin was only 0.5%, a year-on-year decrease of 4.7 percentage points.

In the high-end camp, the Progressive brand where Audi is located saw a 7% increase in sales to 574,000 vehicles, with revenue increasing by 5% to 32.573 billion euros, but operating profit fell by 45% year-on-year, with the profit margin dropping to 3.3%.

In the top Sport Luxury segment(such as Porsche, etc.), sales were 135,000 vehicles, a year-on-year decrease of 11%, with revenue down 9%, and profit falling by 71%, with the profit margin dropping to 5.2%. The main brands remain stable, but the high-end and luxury segments are under significant pressure.

Part 2

The Dual Burden of the Chinese Market and Technical Path Choices

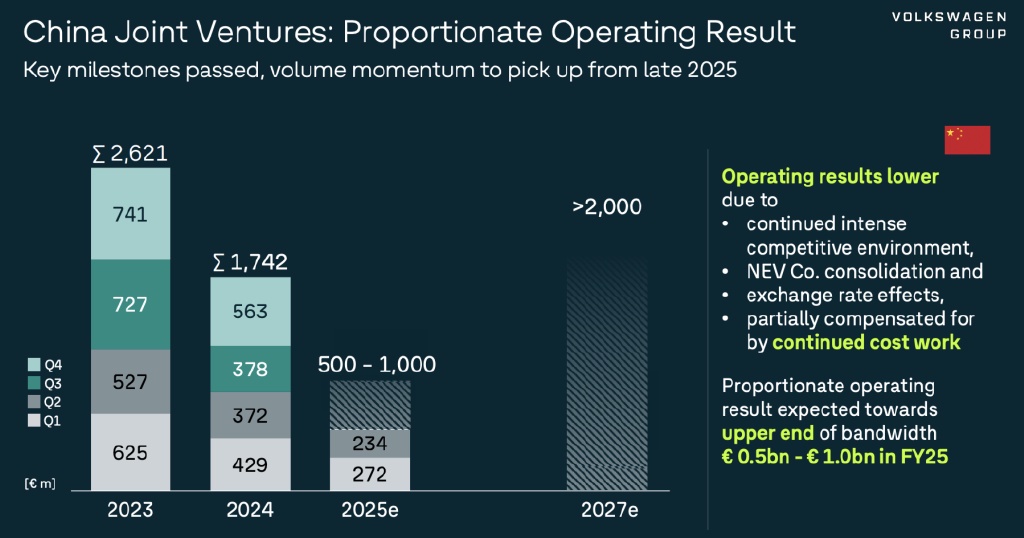

Chinese joint ventures(SAIC, FAW)saw a 2% year-on-year decline in delivery volume, but it is expected to rebound in the second half of the year with the launch of new products.

Operating profit calculated using the equity method was 506 million euros(H1 2024 was 727 million euros), affected by price wars, exchange rates, and new energy transformation costs, but cost optimization partially offset the pressure. The full-year expected operating profit is expected to reach 500-1 billion euros due to the launch of ICV products and the recovery of BEV deliveries.

Intelligent networking and electrification transformation are Volkswagen's current core technology directions. However, judging from the implementation in the first half of 2025, the software and battery businesses are still in a high-investment, low-output climbing period.

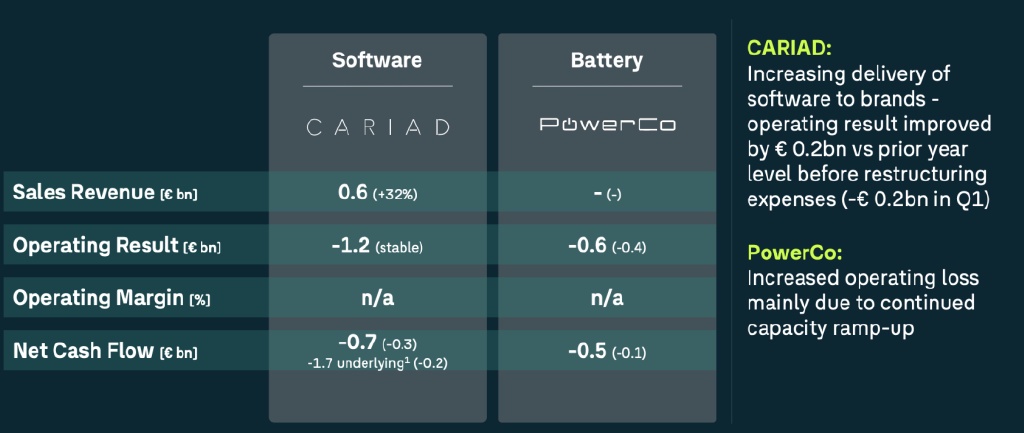

The software subsidiary CARIAD recorded a loss of 1.172 billion euros in H1, almost the same as last year. Volkswagen has proposed a plan to lay off 30% of its staff by the end of 2025, but in the context of the software architecture(especially the E³ platform)not being successfully implemented, layoffs are unlikely to immediately improve technical efficiency.

The core issue of CARIAD's continued losses is that its self-developed software has not yet achieved effective integration and implementation, and the adaptation progress of multiple brands on the E³ platform is lagging.

More importantly, the software platform has not formed a unified interface standard, resulting in low coordination efficiency in the vehicle control domain, further affecting the delivery cycle and user experience of electric vehicle products. For example, the iteration pace of intelligent cockpits and assisted driving functions in Audi models is significantly behind market demand.

The battery business is carried by PowerCo, which recorded a loss of 592 million euros in H1(213 million in Q1, 379 million in Q2), with the scale of losses expanding quarter by quarter.

Although Volkswagen has laid out battery factories in multiple locations in Europe, the production lines are still in the climbing stage, and yield and scale effects have not been released. In terms of technical routes, the Prismatic cell route still faces compatibility issues with the industry's mainstream CTP/CTC architecture.

The difficulty in controlling battery costs makes the gross profit margin of BEV products low. Even in the context of sales growth, it is difficult to boost overall profits. Taking models such as ID.3 and ID.4 as examples, orders in the European market have increased significantly, but their profitability still lags behind fuel vehicles, especially in markets with fierce competition in terminal prices, where BEV gross profit levels are severely under pressure.

Volkswagen Group's "In China, For China" strategy is also in its initial stage, with intelligent networked models expected to be launched on a large scale in Q4 2025.

Although the plan proposes to launch 50 new energy vehicles before 2030, the local R&D system has not yet formed a complete closed loop, and the software ecosystem still relies on third-party solutions. Intelligent cockpits and advanced assisted driving functions still have a significant gap compared to local brands.

The uncertainty of technical path choices is also reflected in the capital investment structure.

While maintaining high-intensity R&D expenditures, the losses of CARIAD and PowerCo are dragging down the overall capital return efficiency. The existing software platform cannot effectively support the coordinated development of multiple brands, instead forming internal friction, which also limits the integration and delivery efficiency of electric vehicle models.

Summary

Volkswagen Group's pure electric strategy, as of 2025, has affected the overall balance, future profitability models, global organizational structure, intelligent and electrification technology routes, and even the industrial logic it has relied on for a long time.

The first half of 2025 reveals a typical case of a giant in the automotive industry with a large scale but declining flexibility. A multi-brand strategy without synergy effects, an electric vehicle profitability model that has not yet been established, and the impact of the external trade environment together constitute this structural imbalance during the transition period.

For Volkswagen, the current issue is "how to maintain profitability during the transition and how to break down coordination barriers within the organization." In the past, Volkswagen won the market with its strong system capabilities; now, it needs to find an organizational rhythm that adapts to the new era of technology pace in China and global markets. Volkswagen not only needs to live in the era of software-defined vehicles but also needs to redefine itself.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.