Comprehensive analysis report on US stock Palantir (ticker: PLTR)

Comprehensive Analysis Report on Palantir (Ticker: PLTR):

I. Business Model, Moat, and Growth Drivers

- Business Model

- Dual Engines: Government (55%) + Commercial (45%), US commercial revenue up 93% YoY in Q2 2025.

- Product Matrix: Gotham (Government), Foundry (Enterprise), AIP (AI Platform), reducing CAC via "Acquire-Expand-Scale" model, client count up 43% annually.

- Profit Model: Software subscriptions (60%) + Custom services (40%), gross margin 79.8%.

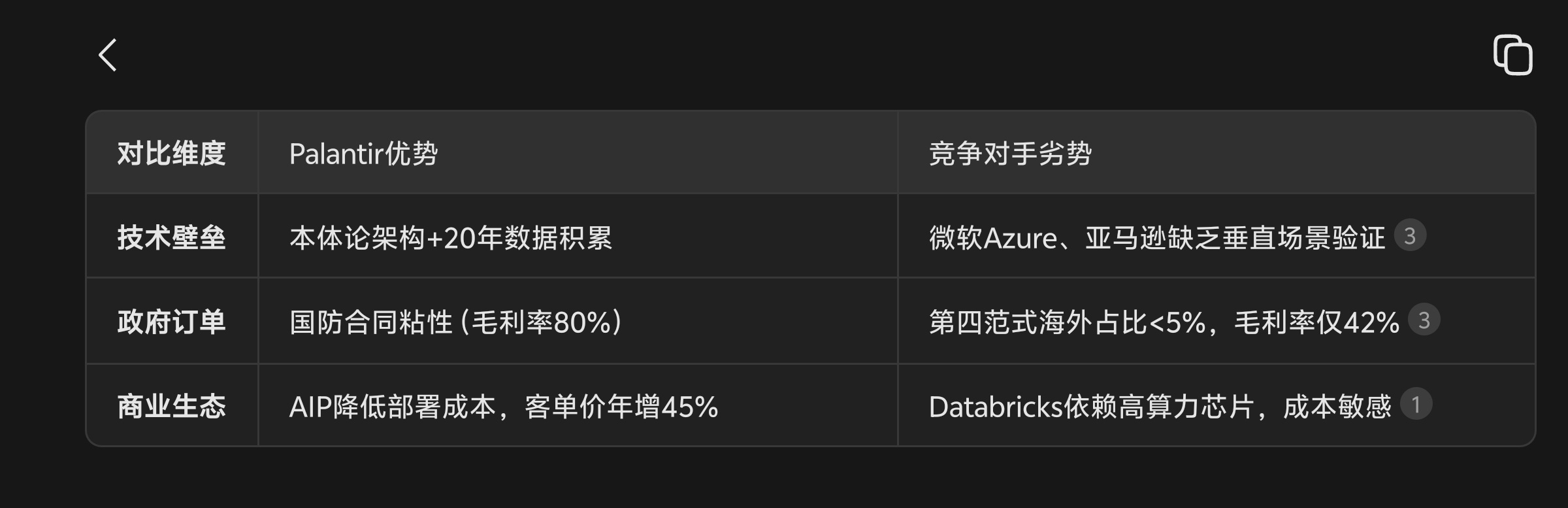

- Core Moat

- Ontology Tech: Transforms domain knowledge into reusable data frameworks, high switching costs (92% retention).

- Defense Barrier: Monopoly in US military AI systems, contracts >$10B (10-year).

- Cultural Cohesion: Engineer-led "mission-driven" culture, industry-leading execution.

- Growth Catalysts

- Commercial Expansion: US commercial revenue projected +85% in 2025, serving 849 clients across finance/healthcare/manufacturing.

- Global Breakthrough: 68% win rate in European govt tenders.

- AI Agents: AIP converts generative AI into workflows (e.g., BP’s $100M+ annual revenue boost).

- Delisting Risk

- None (positive GAAP earnings for 6 straight quarters).

II. Market Share Defense Score: 8.5/10

Conclusion: Tech + scenario + policy moats make disruption unlikely near-term.

III. Management & Governance

- Competence & Integrity

- Stable founding team (CEO Alex Karp: 20 years), but May 2025 $115M stock sale drew scrutiny.

- Ethics: Denies illegal surveillance, emphasizes platform security.

- Ownership Structure

- Triple-class shares: Karp holds 49.9% voting power, weak external influence (governance discount).

- Mission Alignment

- 100% focus on national security/enterprise efficiency, rejects authoritarian regimes.

IV. Market TAM & Industry Growth

- TAM: $1T global AI software market in 2025, Palantir share <1%.

- Penetration:

- Government: US defense AI spend +15% YoY, Palantir share >50%.

- Commercial: Covers 20% of Fortune 2000, clients +39% YoY.

- Projections:

2025 Revenue: $4.15B (guidance) → 2030 $30-40B (CAGR 35%)

Net Margin: 33% (2025Q2) → 40%+ by 2030 (scale).

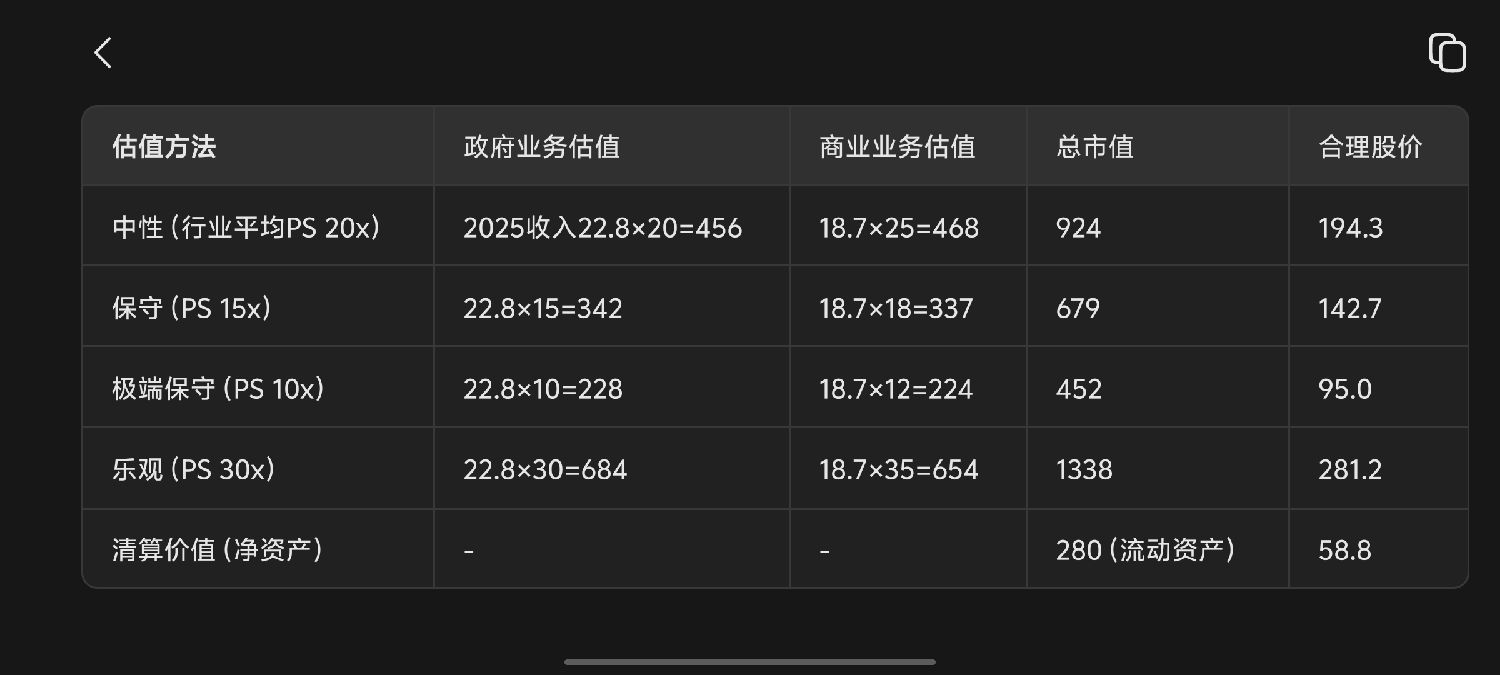

V. SOTP Valuation ($Barrick Mining(B.US))

Conclusion: Current $158.74 exceeds conservative estimates, limited margin of safety.

VI. F-score & Z-score Health

F-score (9/9):

1. ROA 3.27% → 1

2. ΔROA +15% → 1

3. CFO $569M → 1

4. CFO>ROA → 1

5. Leverage stable → 0

6. Quick ratio 5.55 → 1

7. No dilution → 1

8. Gross margin +1.2% → 1

9. Asset turnover 0.35 → 1

→ Extremely healthy.

Z-score:

258.5 (>>2.99 safe threshold) → No bankruptcy risk.

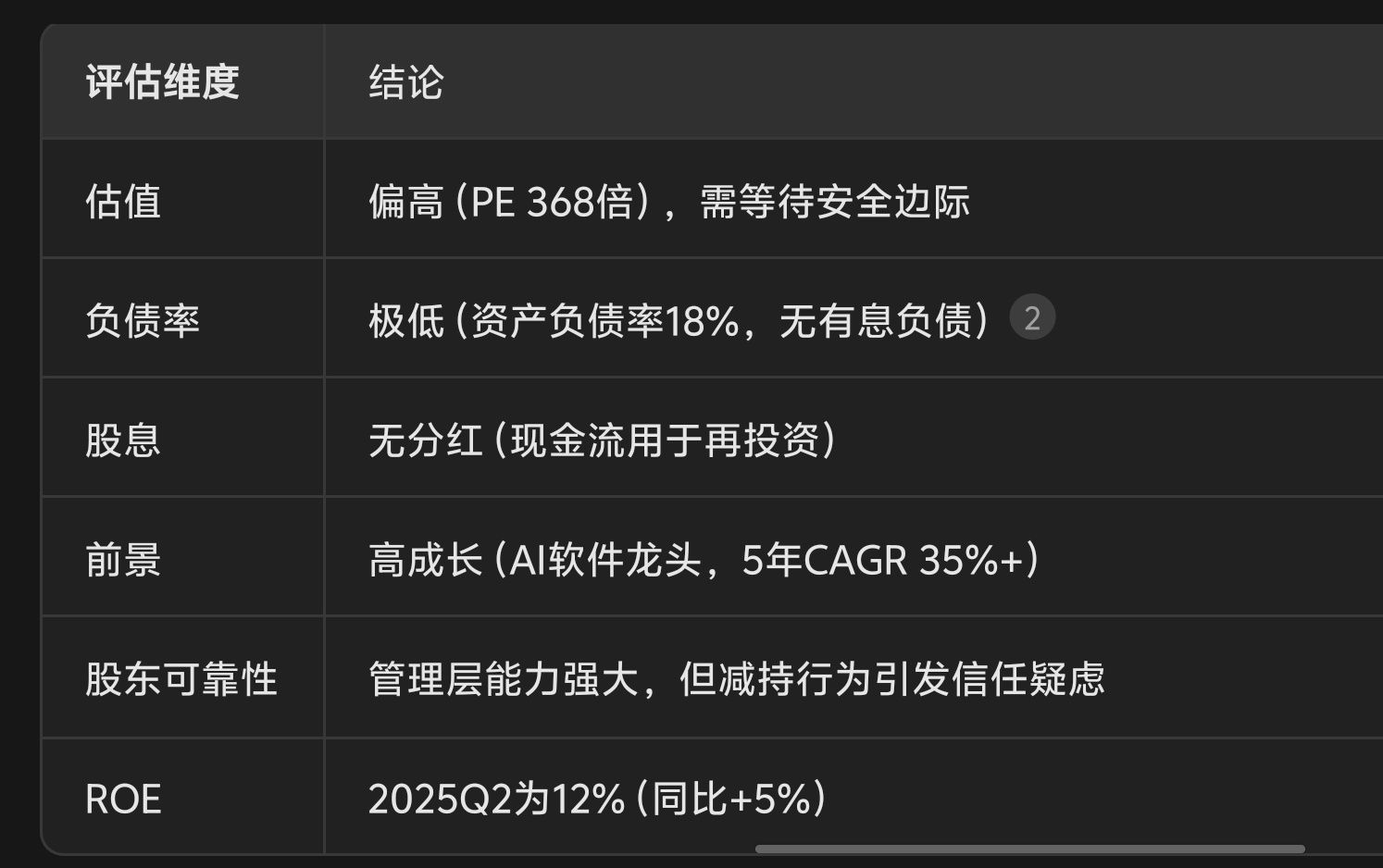

VII. Verdict: To Invest?

Risks:

• Defense cuts (Trump’s proposed 8% reduction);

• Open-source AI competition (US govt’s OpenStack push).

Recommendations:

• Long-term: ≤10% position at current price, heavy below $95 (ultra-conservative valuation).

• Short-term: Avoid—overvalued with technical pressure.

• Ideal entry: ≤$95 (PS 10x, $45.2B cap), PT $735.5 ($350B cap).

“Great company needs great price.” Palantir’s moat is deep, but current valuation requires digestion. Wait for the sweet spot, monitor commercial growth sustainability.

Disclaimer: Not investment advice.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.