Yimai Sunshine 4000-word in-depth research report

$Zhejiang Zhongcheng(002522.SZ)$Meinian Onehealth(002044.SZ) $Aier(300015.SZ) researched OneMedNet (02522.HK), with the core being the growth potential of third-party medical imaging centers and the company's "license + expert" barriers, but the stability of profitability and asset efficiency on the financial side need close attention.

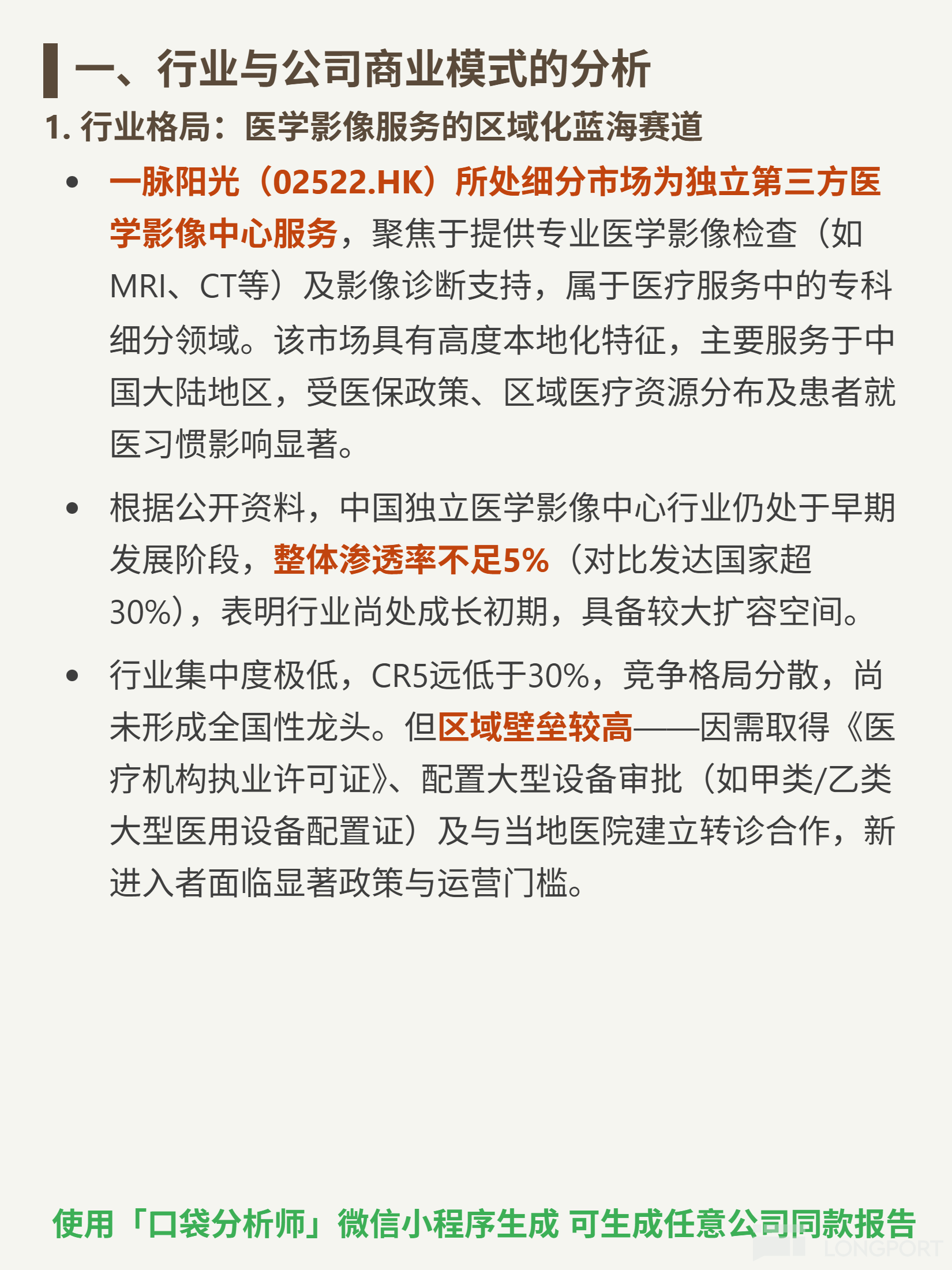

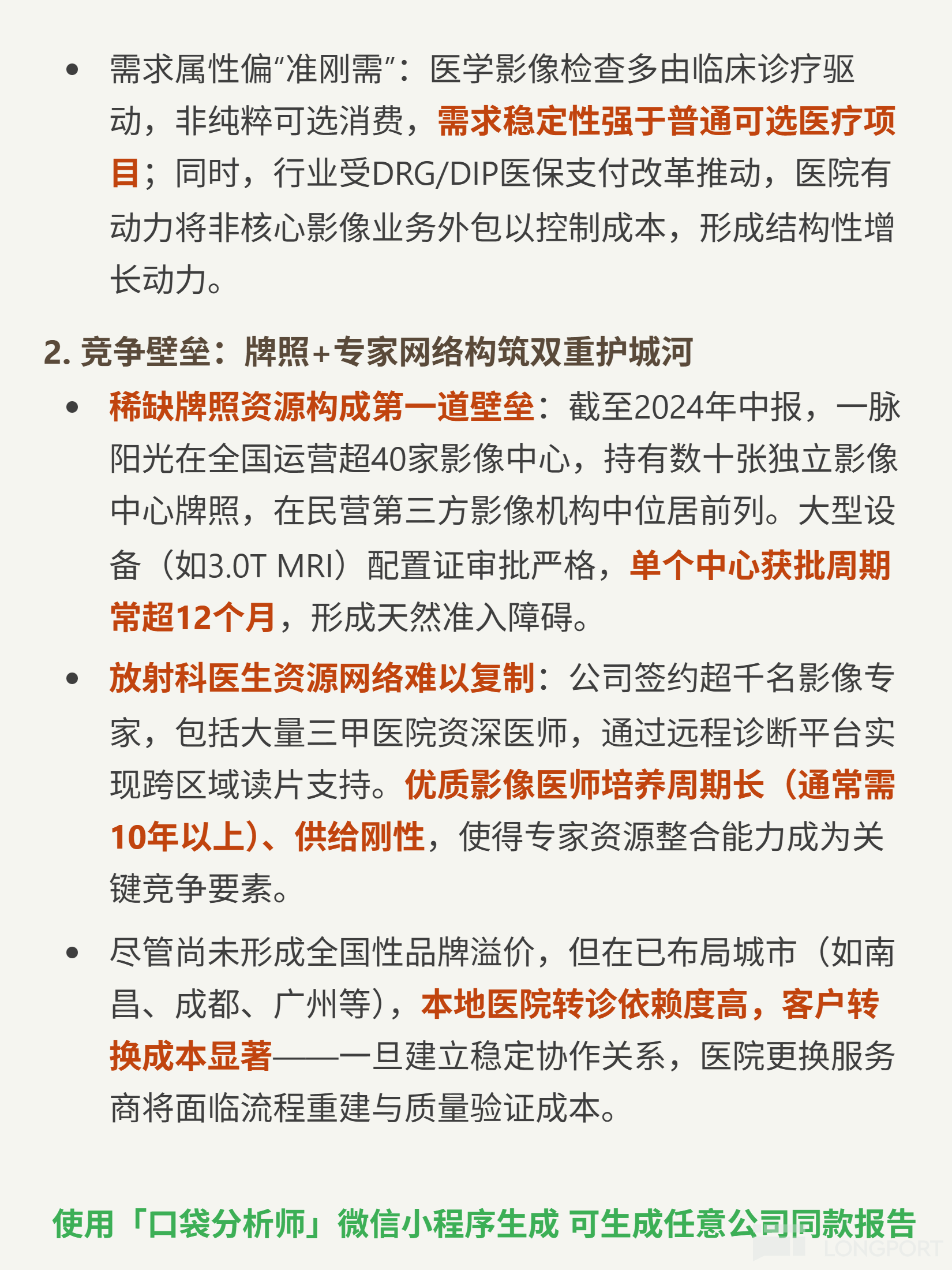

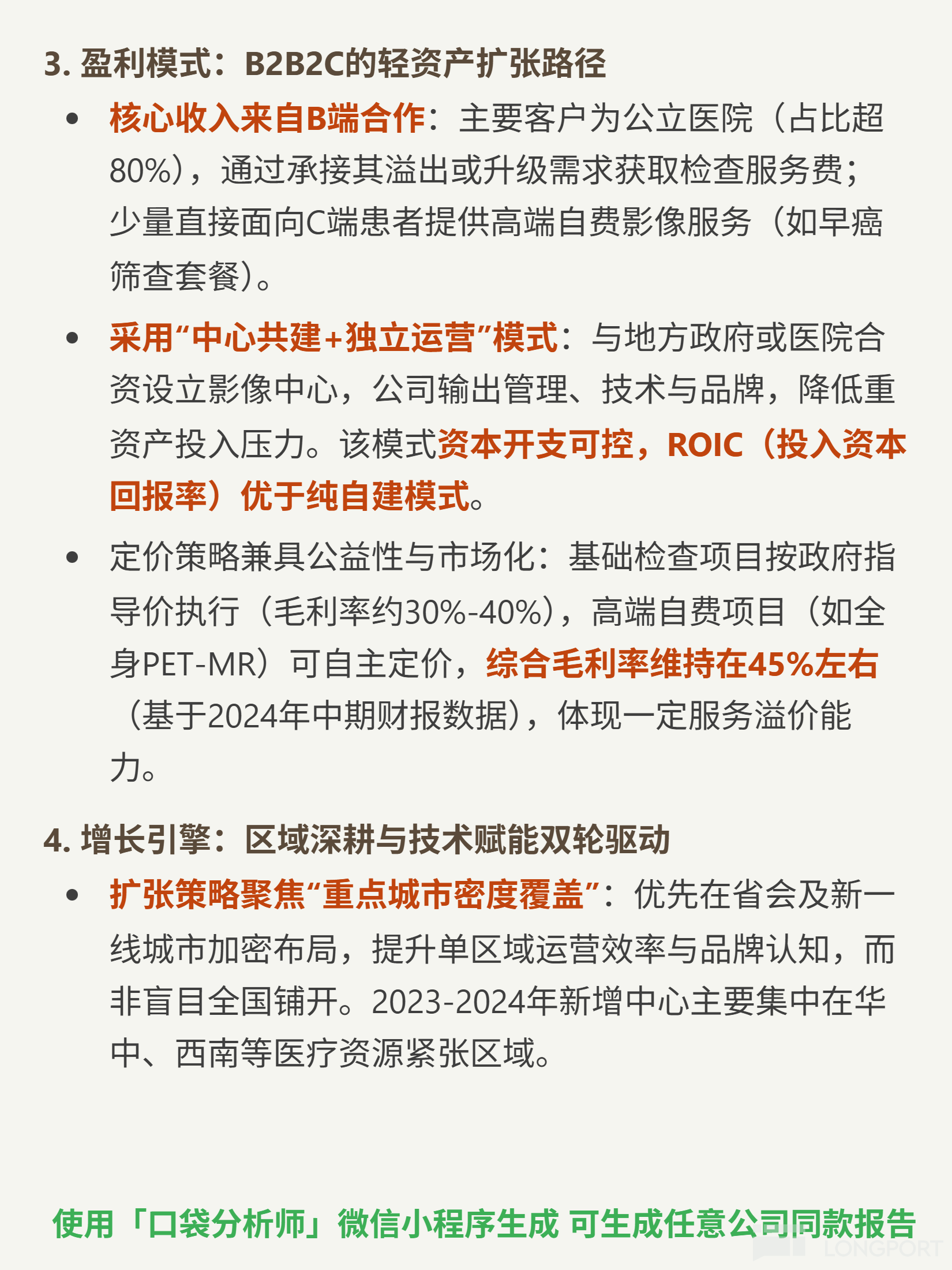

🎯Core logic: The company operates independent third-party medical imaging centers, providing MRI, CT, and other examinations and diagnoses, adopting a B2B2C model (mainly serving B-end hospital referrals). Industry penetration is less than 5% (over 30% in developed countries), with high regional barriers (requiring licenses, equipment approvals over 12 months, and hospital cooperation). Demand is quasi-essential (clinically driven, with DRG/DIP promoting hospital outsourcing). Competitive barriers are scarce licenses (operating over 40 centers) and a remote reading network of over 1,000 top-tier experts.

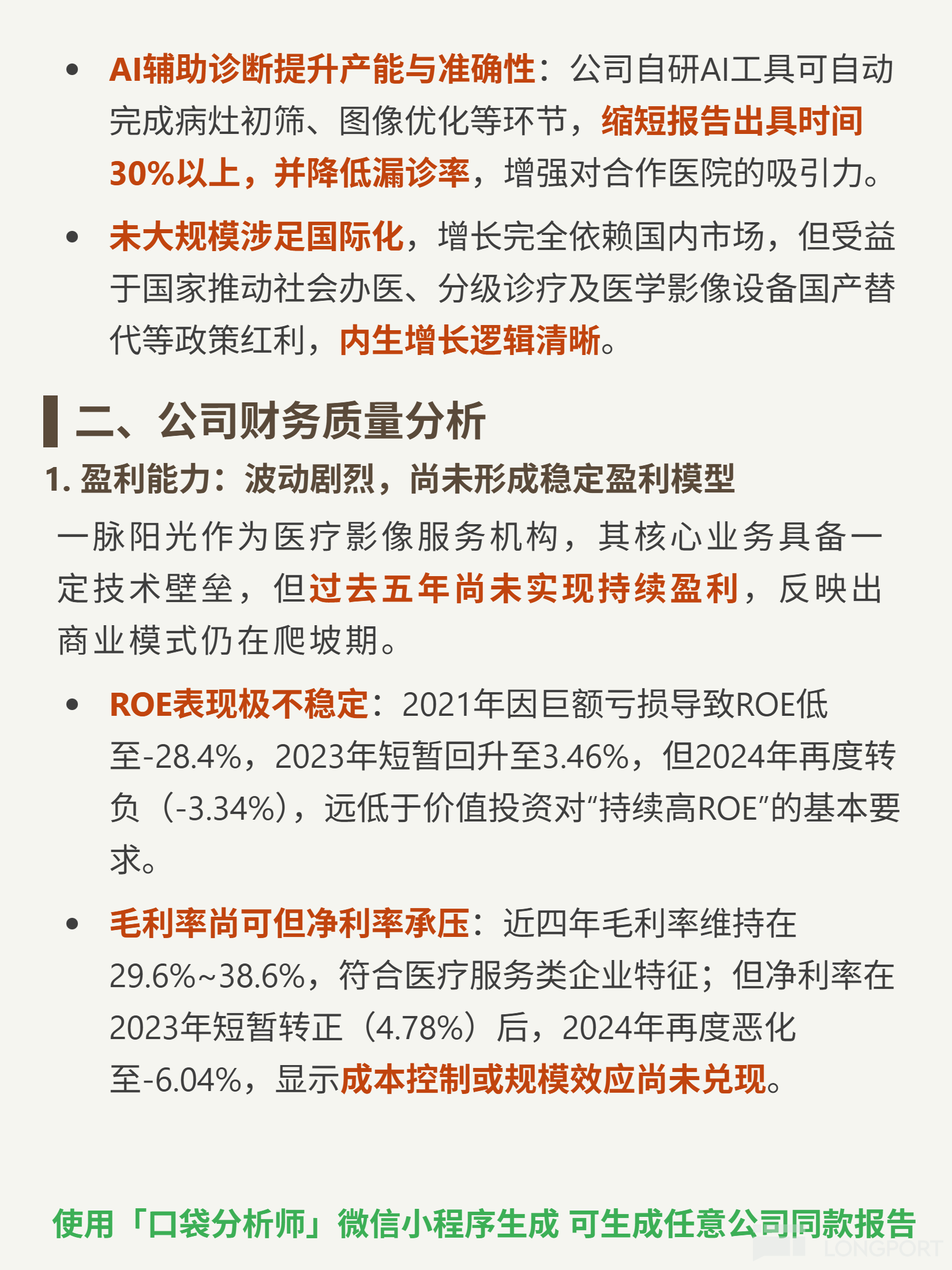

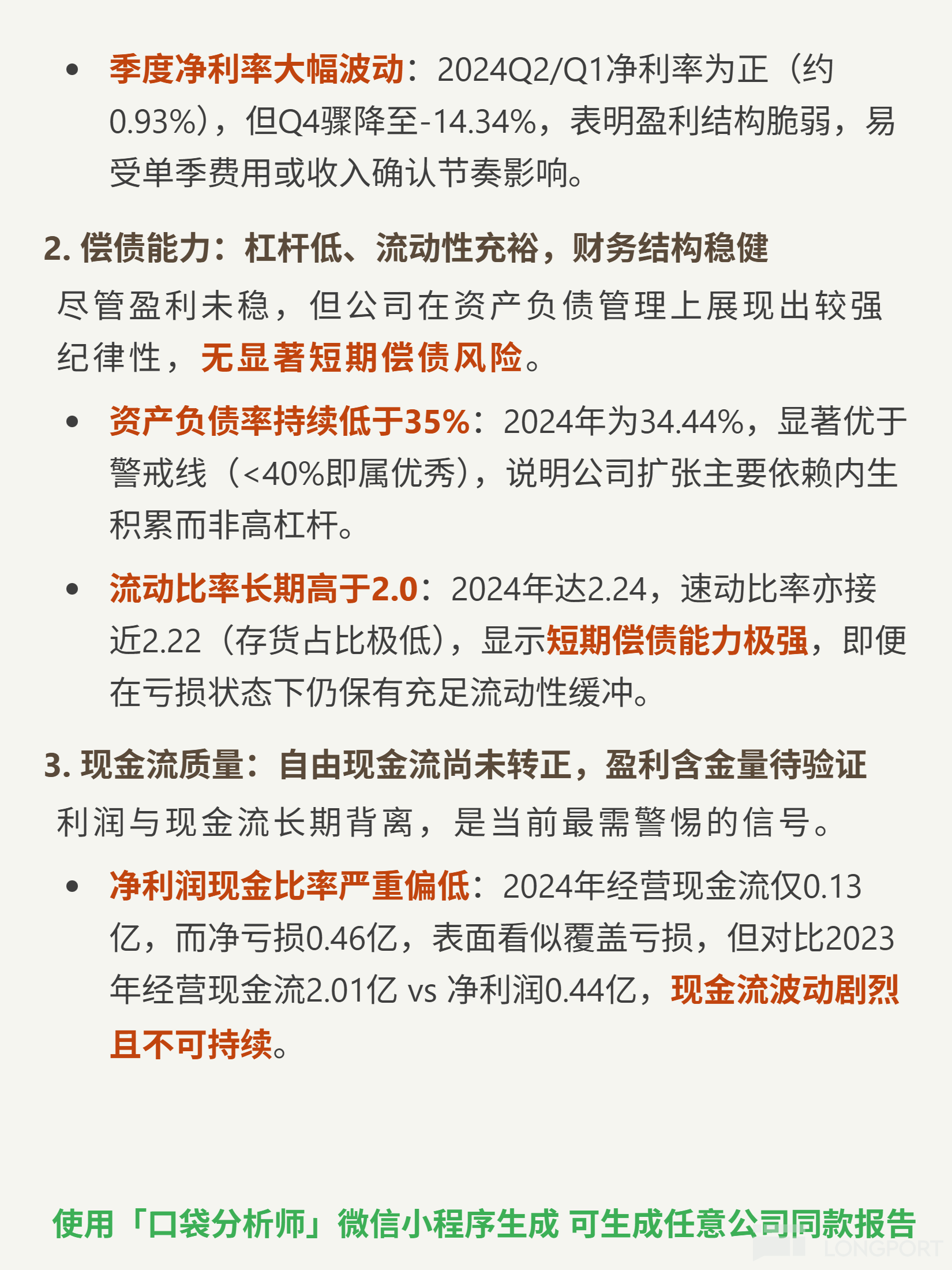

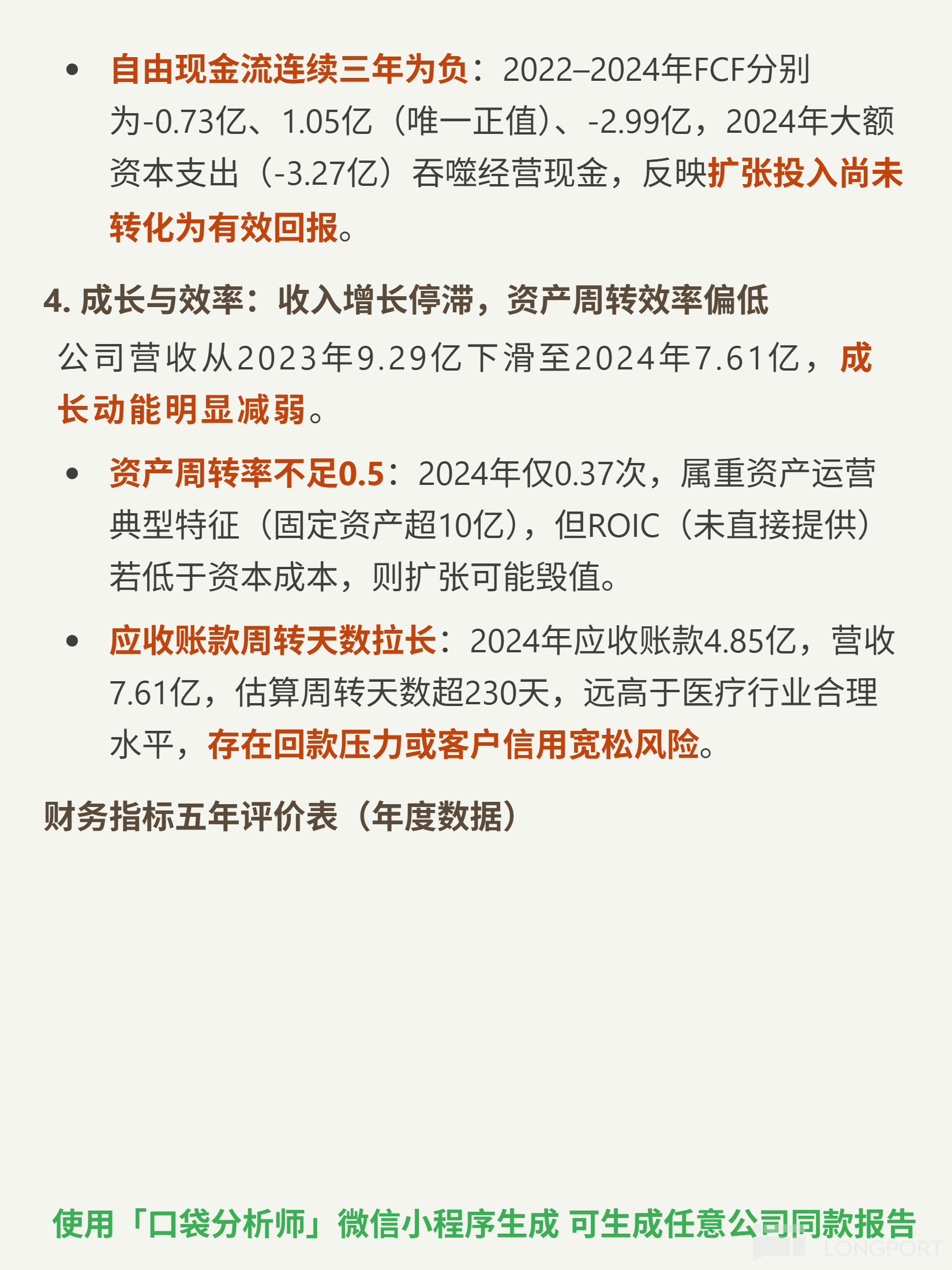

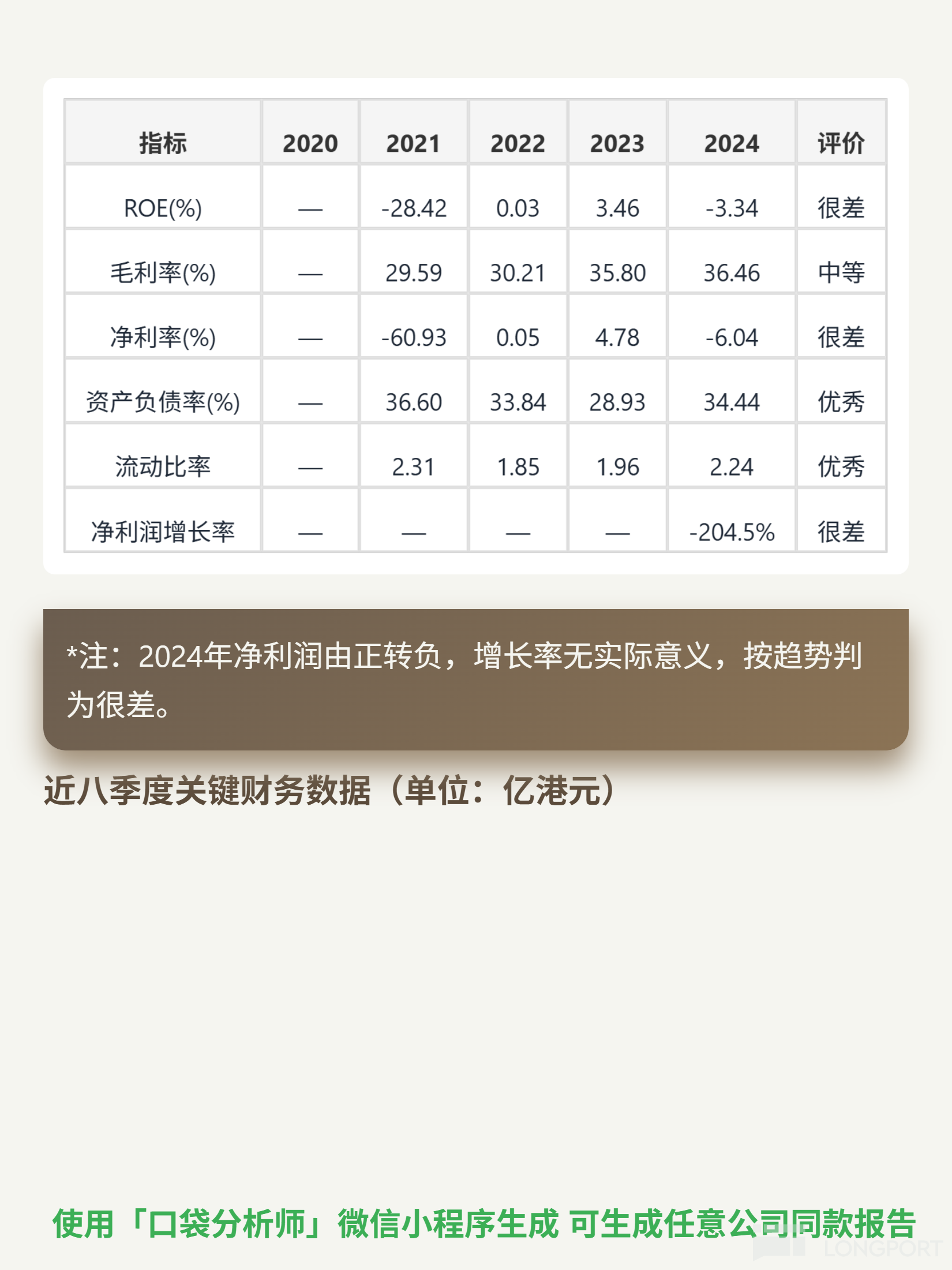

📈Financial performance: 2024 gross margin was 36.46% (moderate), but ROE -3.34%, net margin -6.04%, revenue fell to 761 million (929 million in 2023); debt repayment ability is stable (debt-to-asset ratio 34.44%, current ratio 2.24), but free cash flow was -299 million (negative for three consecutive years), accounts receivable increased by 46% (485 million), fixed assets were 1.098 billion but turnover rate was only 0.37 times, indicating low asset efficiency.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.