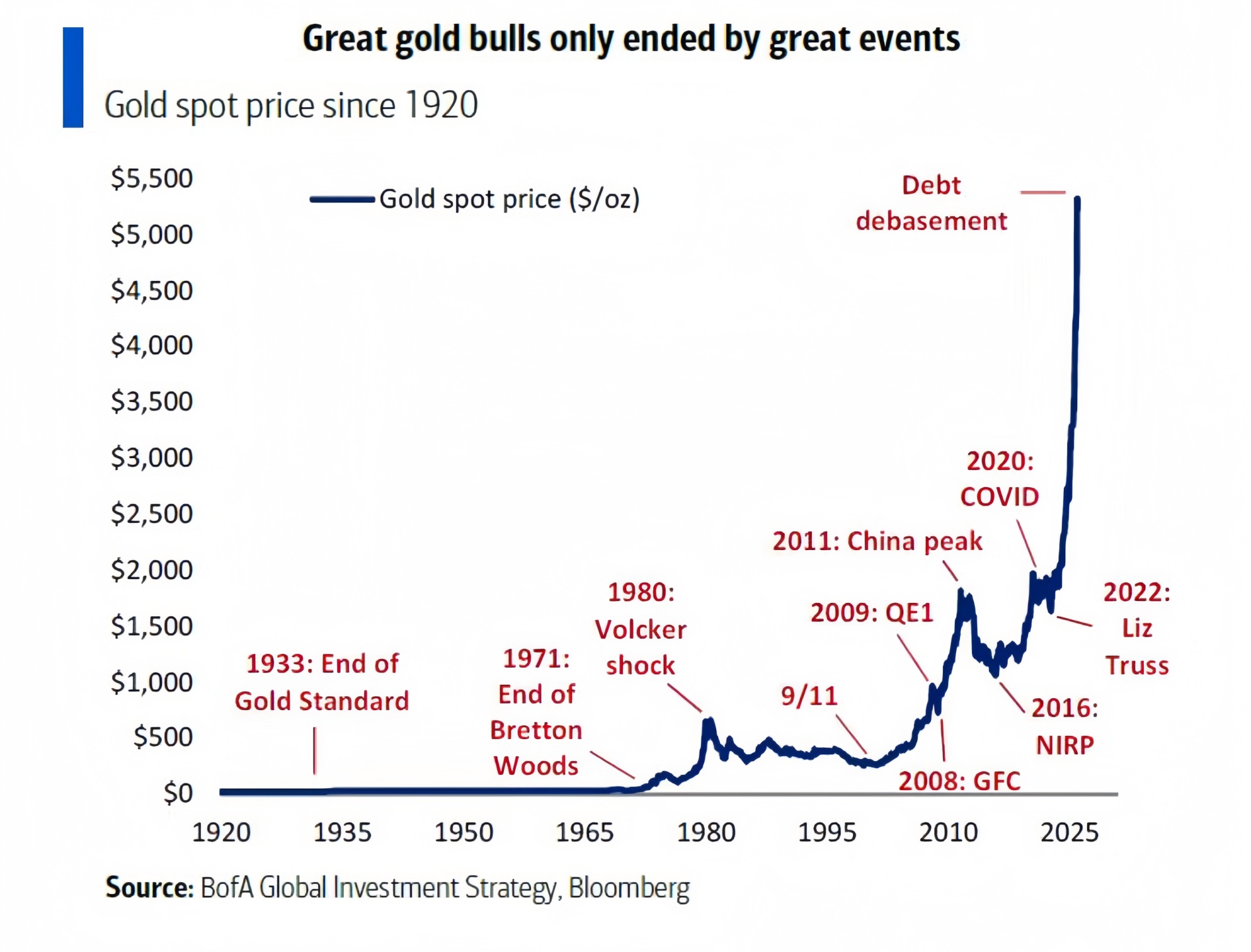

Bank of America's Hartnett: Only a 'bigger event' can end the gold bull market

Despite the recent "epic volatility" triggering a silver crash and a short-term dollar rebound, Michael Hartnett, Chief Strategist at Bank of America, still emphasizes—"Debasement is the Base Case." Unless a "destructive larger event" disrupts the liquidity logic, the gold bull market is unlikely to end.

·What Happened on Friday

A sudden stock market drop, a sharp dollar rally, and rumors of Kevin Warsh potentially replacing Powell caused an instant shift in risk asset sentiment. Silver experienced a "record single-day crash," reflecting deleveraging/liquidity shocks rather than a complete reversal of the macro narrative.

·Weak Dollar = Political Economics

Hartnett believes the dollar's weakness is not accidental but a policy inclination.

A weak dollar is seen as a tool to boost manufacturing and votes in the "Rust Belt," involving swing states like Pennsylvania, Michigan, and Wisconsin. It’s also noted that Donald Trump's approval rating during his term correlated with dollar trends.

Historical data (since 1970) shows that bear markets for the dollar average a decline of about 30%, during which gold and emerging market stocks tend to outperform.

A short-term sharp pullback ≠ trend termination; the real "end" usually comes from stronger liquidity contraction or systemic shocks.

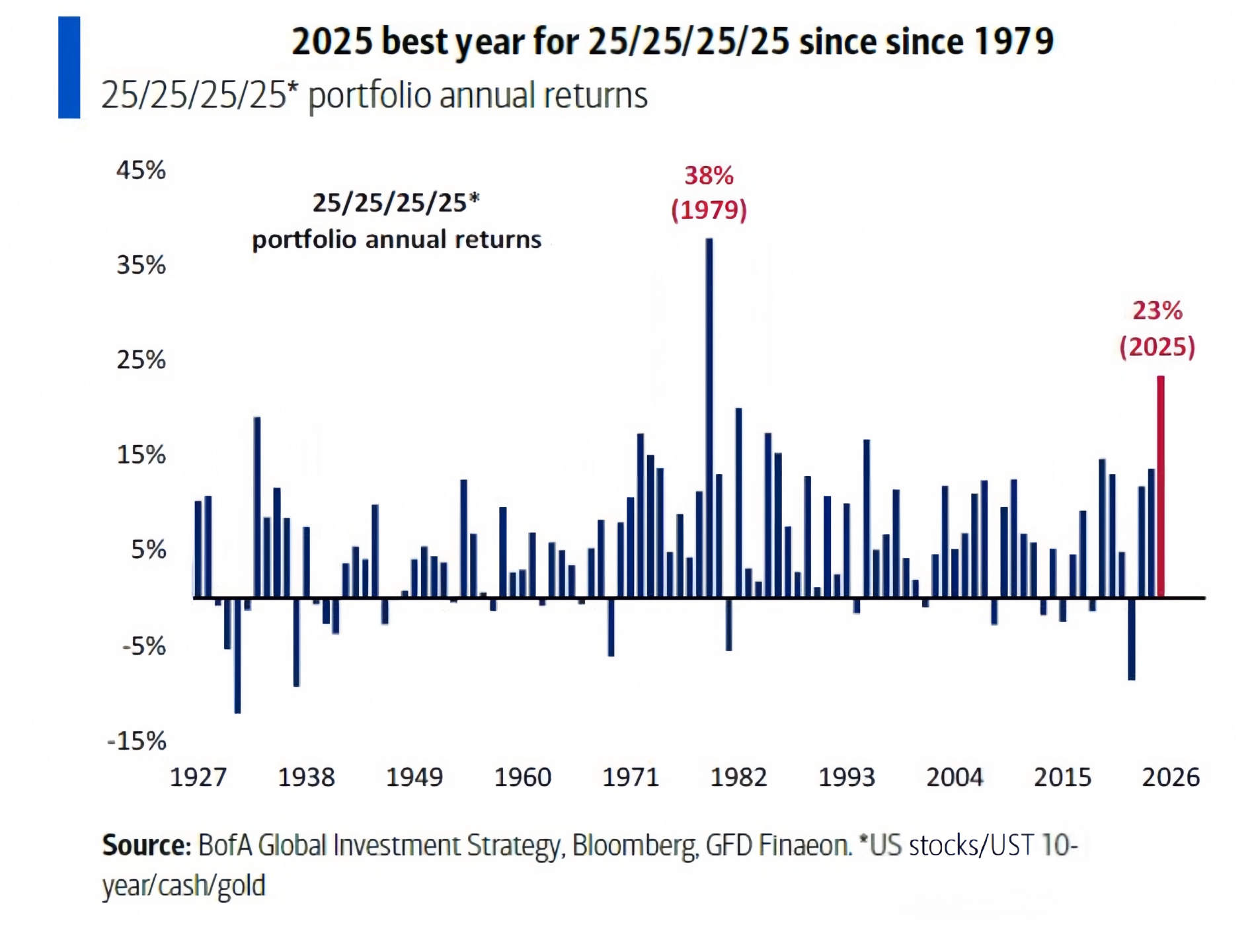

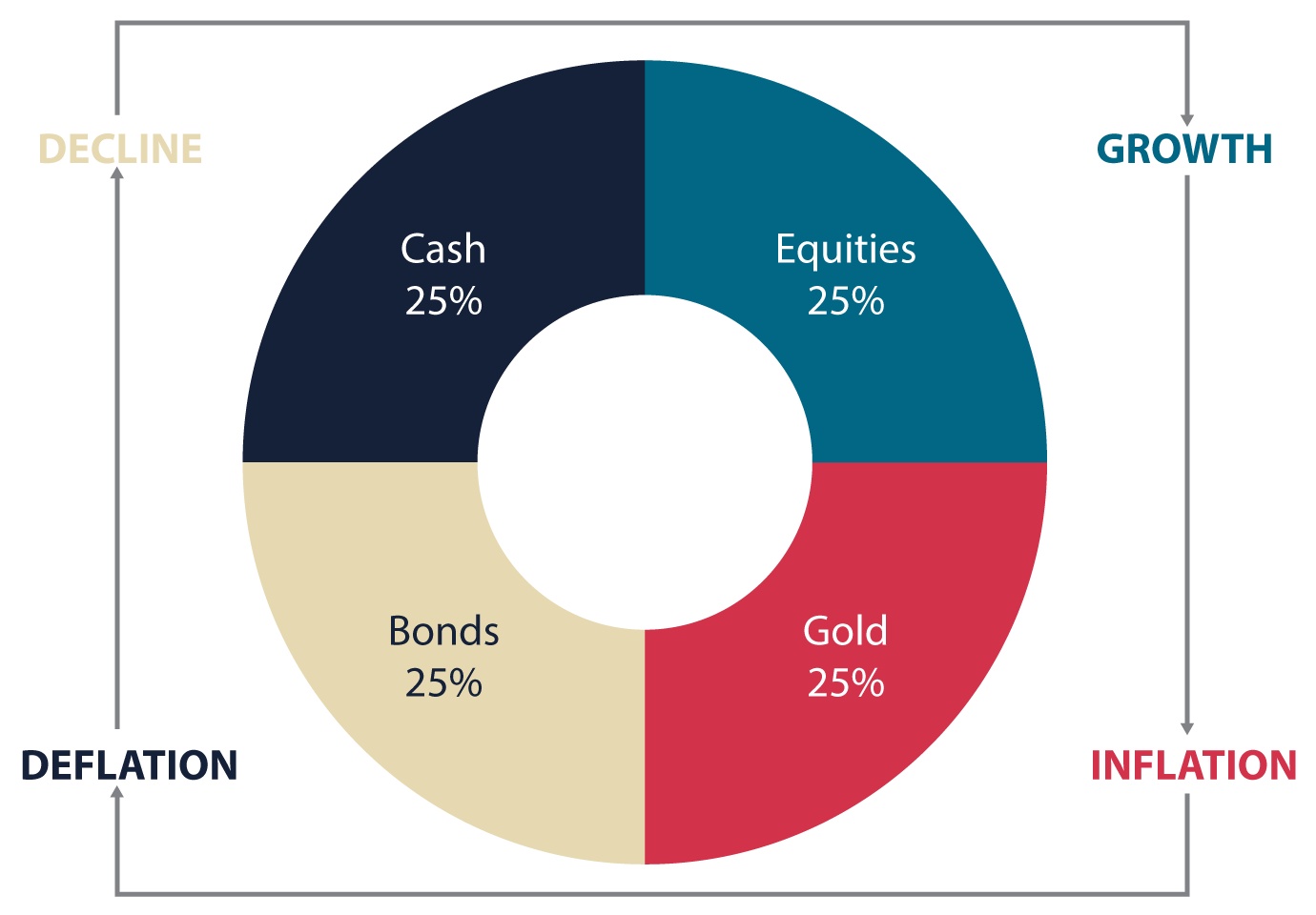

·The Return of the Permanent Portfolio

The traditional 60/40 allocation is no longer suitable; the alternative is 25/25/25/25 (stocks/bonds/gold/cash).

Use "rebalancing + four quadrants" to counter inflation volatility and growth uncertainty; the core is to reintegrate gold and cash into central allocations.

Its 10-year return is reportedly 8.7% (the best since 1992), with 2025 returns around 23% (the best since 1979), emphasizing that in an era of "currency debasement + inflation volatility," gold and cash should return to core positions.

·Major Risk Source: H1 Liquidity Deleveraging

Current trading congestion is extremely high—non-U.S. investors hold about 64% of U.S. stock market value, ~55% of global corporate bonds, and ~50% of global government bonds. A mere 5% cut in U.S. stocks and bonds could trigger ~$1.5 trillion in capital outflows; combined with the U.S. ~$1.4 trillion current account deficit and ~$1.7 trillion budget deficit, the impact cannot be ignored.

Conclusion: The short-term way to cleanse "greed" is more likely to be deleveraging rather than an immediate end to the devaluation narrative.

·2026 Trading Clues: BIG + MID:

Continuing contrarian thinking—the 2020 "pain trade" was going long on gold;

The 2026 potential "contrarian trade" may shift to going long on bonds (though this may not work amid global debt 泛滥).

The specific portfolio preference is BIG + MID: Bitcoin (B) + International stocks (I) + Gold (G) + Mid-cap stocks (MID), betting on relative winners under the new macro paradigm.

Data Source: BofA Global Investment Strategy — The Flow Show

$SPDR Gold Shares(GLD.US) $Invesco QQQ Trust(QQQ.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.