Don't be a robot in the spreadsheet: Why does "making sense" make you more money than "absolute rationality"?

In the financial world, we are taught that "emotion" is the great enemy of investing. We try to become extremely cold-blooded and rational, making decisions based solely on data and probabilities.

However, Chapter 11 of "The Psychology of Money" presents a different perspective: "Rational" is theoretical, while "Reasonable" is practical for survival. It was the first time I seriously distinguished between these two words. Indeed, many things in life cannot be consistently rational because we are complex, emotional humans.

The author uses three counterintuitive examples to illustrate the difference between rationality and reasonableness:

1. The Lesson of "Fever Therapy": Rationality is Painful

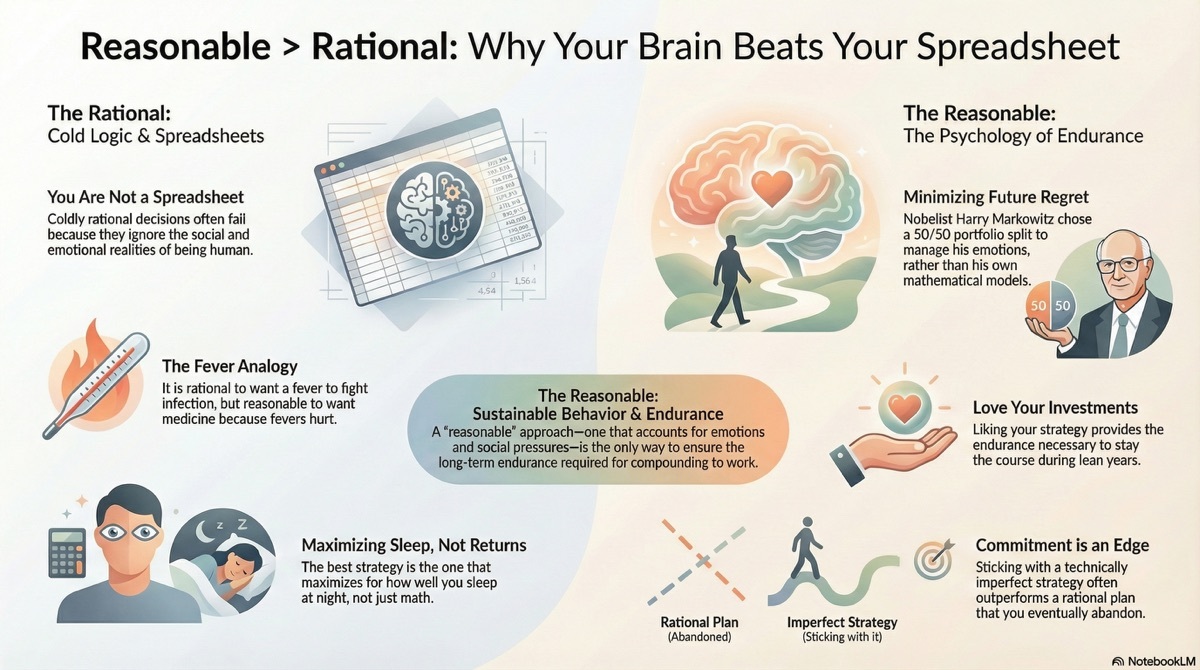

In the early 20th century, Dr. Julius discovered a brutal method to treat syphilis: injecting patients with malaria. Rational logic: Malaria causes high fever, and high fever can kill syphilis bacteria. Therefore, giving patients malaria can save their lives. Reasonable reality: Fever is extremely painful. Although science proves that fever helps the immune system, we still take fever reducers when we are sick because the human instinct is "I don't want to suffer."

Investment analogy: Research from Yale University suggests that young people should invest in the stock market with 2x leverage, which is the mathematically "rational" optimal solution. But in reality, when the stock market crashes 50% and wipes out your account, no normal person can remain unfazed and stick with it. You will break down, you will exit. A "rational" strategy that is perfect on paper, because it ignores your pain tolerance, will ultimately force you out.

2. The "Hypocrisy" of a Nobel Laureate: A Good Night's Sleep is More Important than Math

Harry Markowitz won the Nobel Prize for inventing "Modern Portfolio Theory." He is the pioneer of using mathematics to optimize risk and return.

But when asked how he invested his own money in the 1950s, did he use his Nobel-winning complex model? No. He simply and brutally put 50% in stocks and 50% in bonds. Why? Not because it was mathematically optimal, but because he wanted to "minimize future regret." Even the pioneer of financial rationality, when facing his own real money, chose a strategy that made him "feel comfortable," not the one with the highest return.

3. "Falling in Love" with Your Stock is Actually an Advantage

Traditional advice says: "Don't fall in love with your stock; it doesn't know you own it." This chapter, however, argues the opposite: you should actually have some emotional attachment to your investments.

Why? Because in long-term investing, the only important variable is commitment.

If you only see your investment as cold numbers, once it crashes, you have no reason to hold on. But if you genuinely like the company you invest in (liking its products, mission), this "irrational" emotion becomes a painkiller that helps you endure the suffering. Those investors who "deeply love" their imperfect strategy, because they can hold on, ultimately outperform those rationalists who are smart but always cut losses.

💡 Memorable quotes:

"You are not a spreadsheet. You are a person. A messed-up, emotional person."

"Instead of trying to stay coldly rational, try being a reasonable person. It works better."

"Investors who love their 'technically imperfect' strategy actually have an advantage because they are more likely to stick with it."

Stop obsessing over finding the mathematically perfect strategy with the highest return. Go find the strategy that lets you sleep at night.

If paying off your low-interest mortgage makes you feel safe, then do it—even if the math says it's not optimal.

The best strategy is not the one with the highest ROI, but the one you can stick to when the world is on fire.

$Alphabet(GOOGL.US) $Alphabet(GOOGL.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.