$Tesla(TSLA.US)

Haha, narrative. If I were on Wall Street, I'd also drain your liquidity.

First, there's no narrative here at all.

All this talk about EVs in winter, deliveries falling short of expectations? Pure BS.

The difference between 358,000 and 360,000 isn't even a rounding error in the financial report.

I just needed an excuse to sell off, and you handed me the knife.

Second, when capital reaches a certain scale, it has little to do with the actual business.

I'm holding hundreds of billions that need to be reallocated, OpenAI swallowed 120 billion, SpaceX needs 75 billion.

Tesla has the best liquidity, retail investors hold the most, and their faith is the strongest.

Who else should I drain? How many cars they sell is none of my business.

Third, liquidity exists to be liquid. If it's not moving, what kind of liquidity is that?

My money needs to move, it needs to go to OpenAI, to SpaceX.

In a market of finite capital, money doesn't fall from the sky.

Whoever has liquidity is the ATM. Tesla is the most obedient ATM.

So don't ask why it's falling.

It's falling because the finite market is draining you.

And after the drain, you're still over there analyzing the fundamentals.

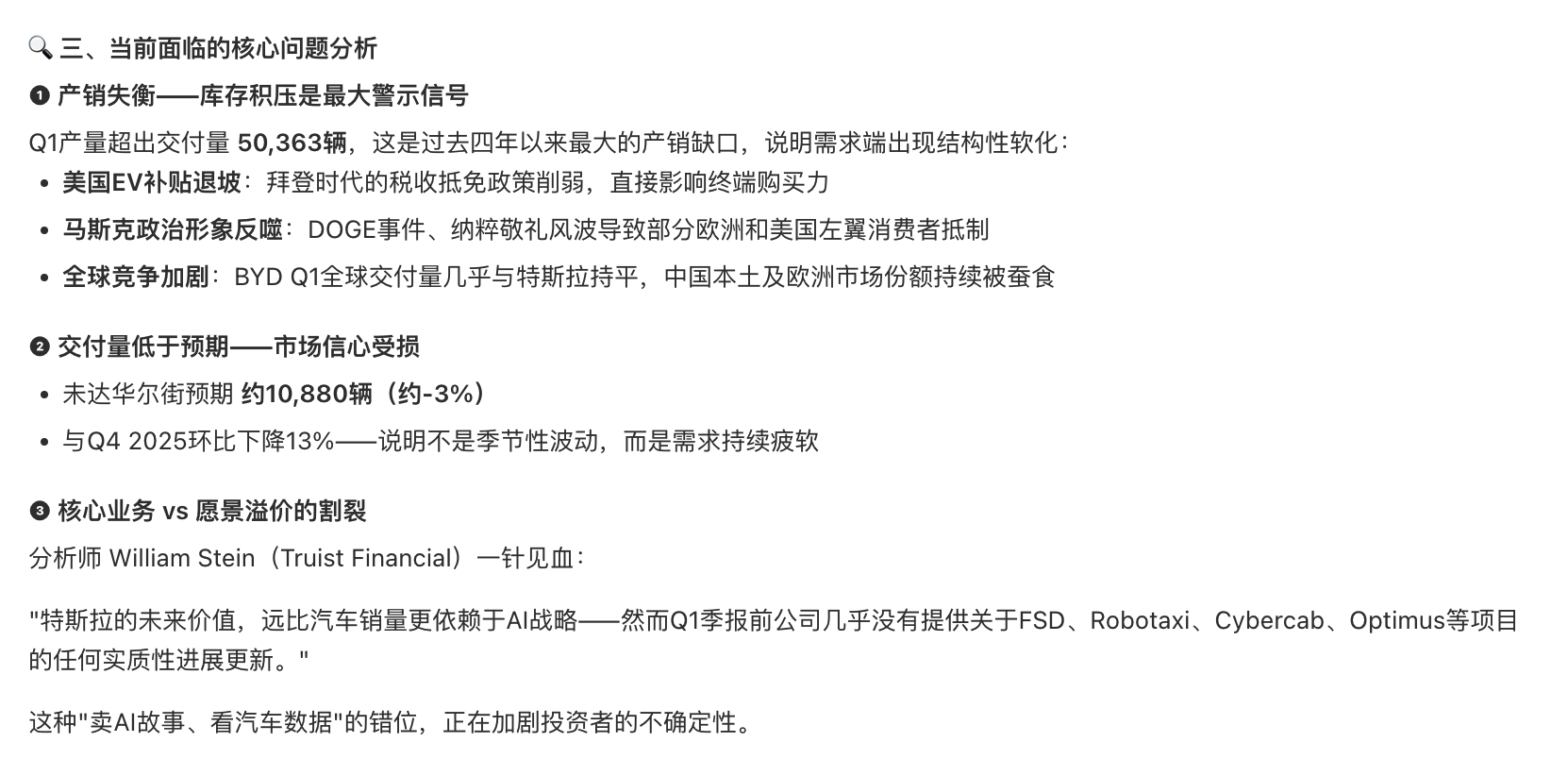

Tesla's latest delivery figures are out, and I've done a quick analysis using Longbridge's newly released skills. In one word: divergence is widening. On the surface, deliveries are still growing, but the growth rate is clearly not as 'crazy' as the past two years; it's more of a steady advance after a slowdown. Combined with the ongoing price adjustments this year, it actually signals that demand isn't as strong as imagined, at least not the kind of mindless explosion.

However, if you only focus on the delivery numbers, it's easy to underestimate its fundamentals. Tesla's current problem isn't that it can't sell, but that it 'has to work harder to sell'. Core capabilities like production capacity, supply chain, and brand strength are still there, and cash flow hasn't deteriorated significantly. Essentially, it hasn't reached the stage of a logic reversal.

What really makes the market conflicted is the issue of the valuation anchor. Previously, everyone gave it a premium as a 'tech company', telling stories about autonomous driving, energy, and AI. But now, with slowing growth, more and more people are starting to view it from the perspective of an 'automaker'. Once the narrative shifts, the valuation framework will follow it downward.

So, the bulls and bears aren't really arguing over a single earnings report; they're betting on a long-term positioning: whether it's still that imaginative tech platform or gradually returning to a rational car manufacturer.

There is indeed short-term pressure, but to be honest, the long-term story isn't over yet.

+2

+2

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.