$Robinhood(HOOD.US)

HOOD 26Q1 Earnings: Revenue $1.07B, Crypto Revenue Down 47%

Key Takeaways:

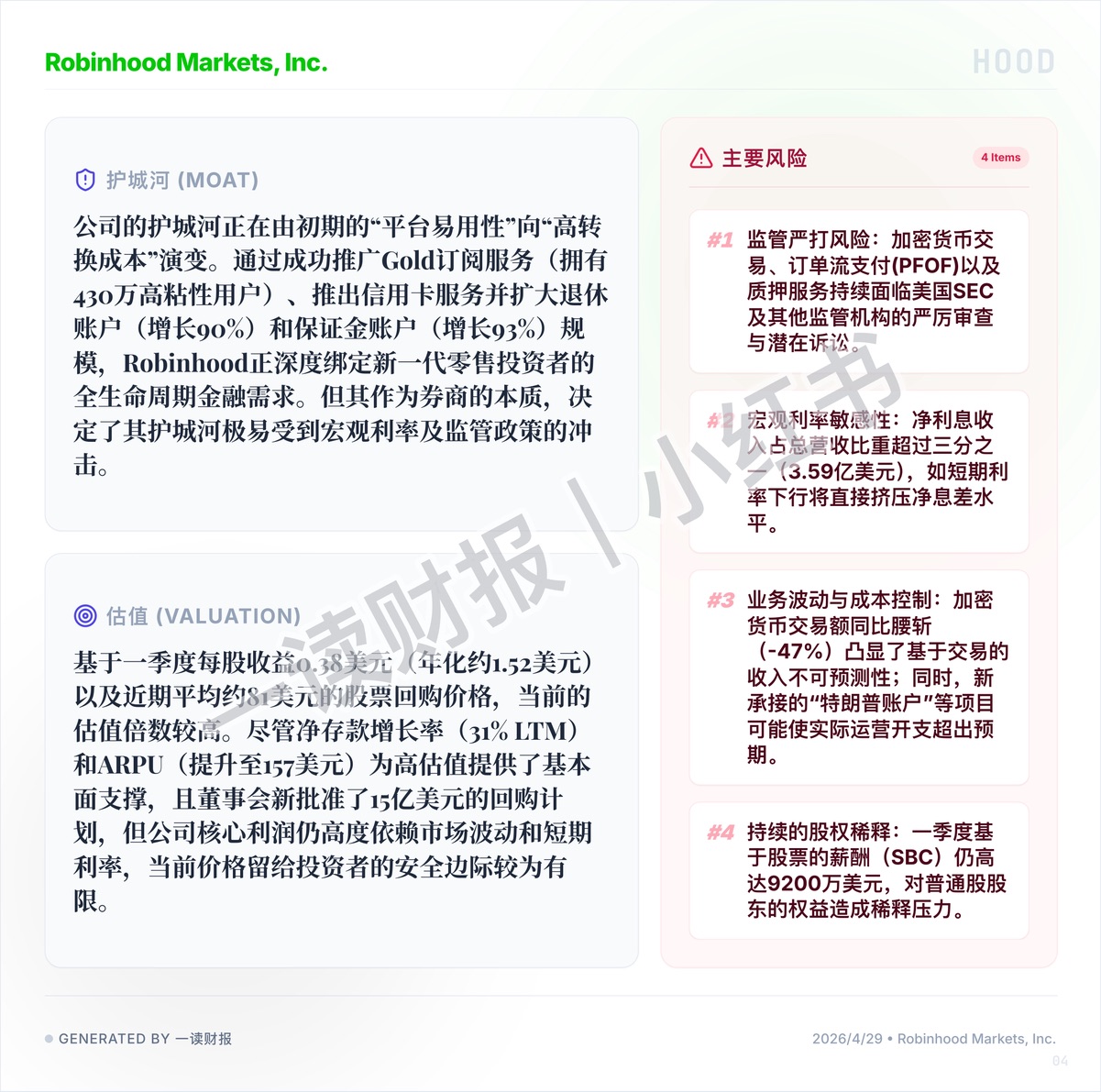

1. "Interest Income Dependence" and Rate Cut Expectations: Total revenue growth is heavily reliant on a significant increase in net interest income (contributing $359 million this quarter, over one-third of total revenue). This profit model is extremely sensitive to macro interest rates. Once the market prices in rate cut expectations, or the Fed actually begins a rate-cutting cycle, its net interest margin will be squeezed, and the superficial profit on the books will quickly evaporate.

2. "Clear Cyclicality in Crypto": As a platform that started with high-frequency trading, HOOD still exhibits strong cyclicality. Cryptocurrency transaction volume plummeted by 47% this quarter, while retail user speculative enthusiasm on the app also dropped sharply (down 48%). Furthermore, cryptocurrency trading, payment for order flow (PFOF), and staking services continue to face strict regulatory scrutiny from the U.S. SEC. The contraction of its underlying high-beta business threatens its long-term transaction fee base.

3. Loss of Capital Discipline and the "Bleeding" from SBC: The market is highly wary of management's recent capital allocation. To accommodate new custody projects like the "Donald Trump account custody," which operates on a cost-plus model with thin margins, management forcibly raised the 2026 operating expense guidance by $100 million. Combined with a single-quarter stock-based compensation (SBC) of $92 million, these actions that continuously drive up customer acquisition costs and dilute common shareholder equity significantly diminish the impact of its $1.5 billion share repurchase plan.

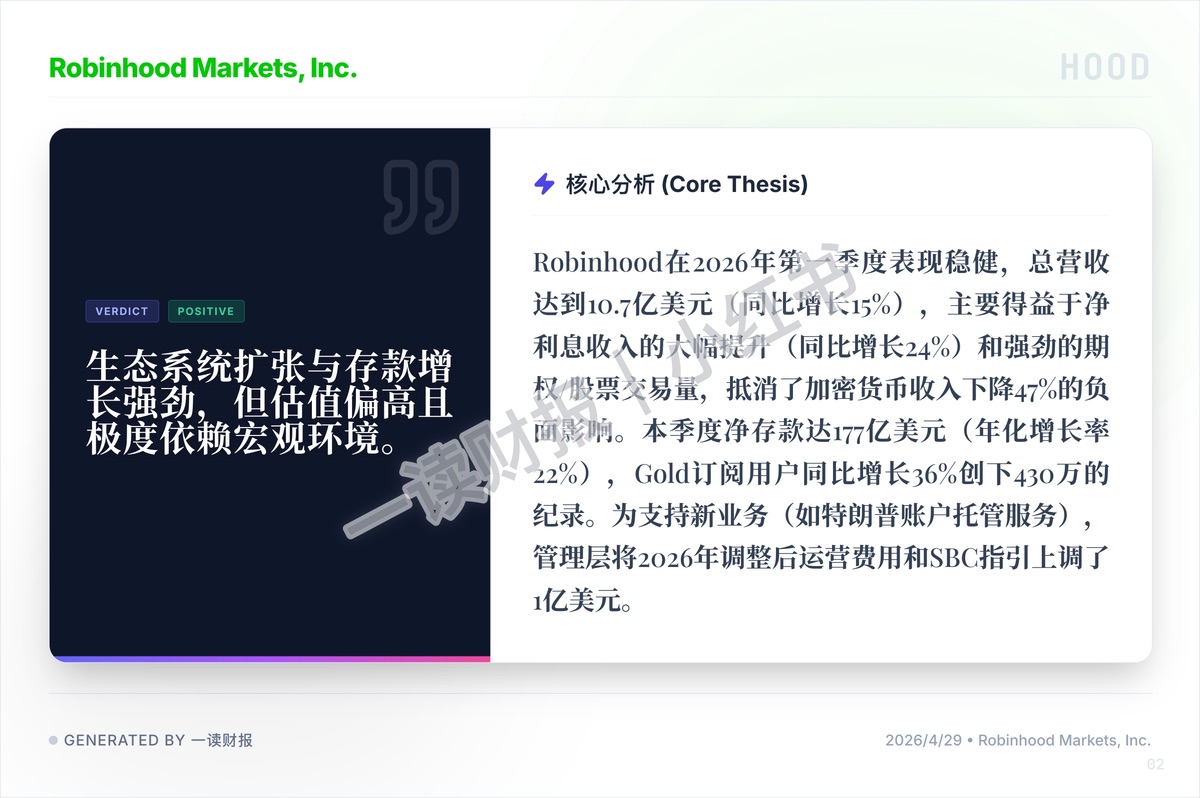

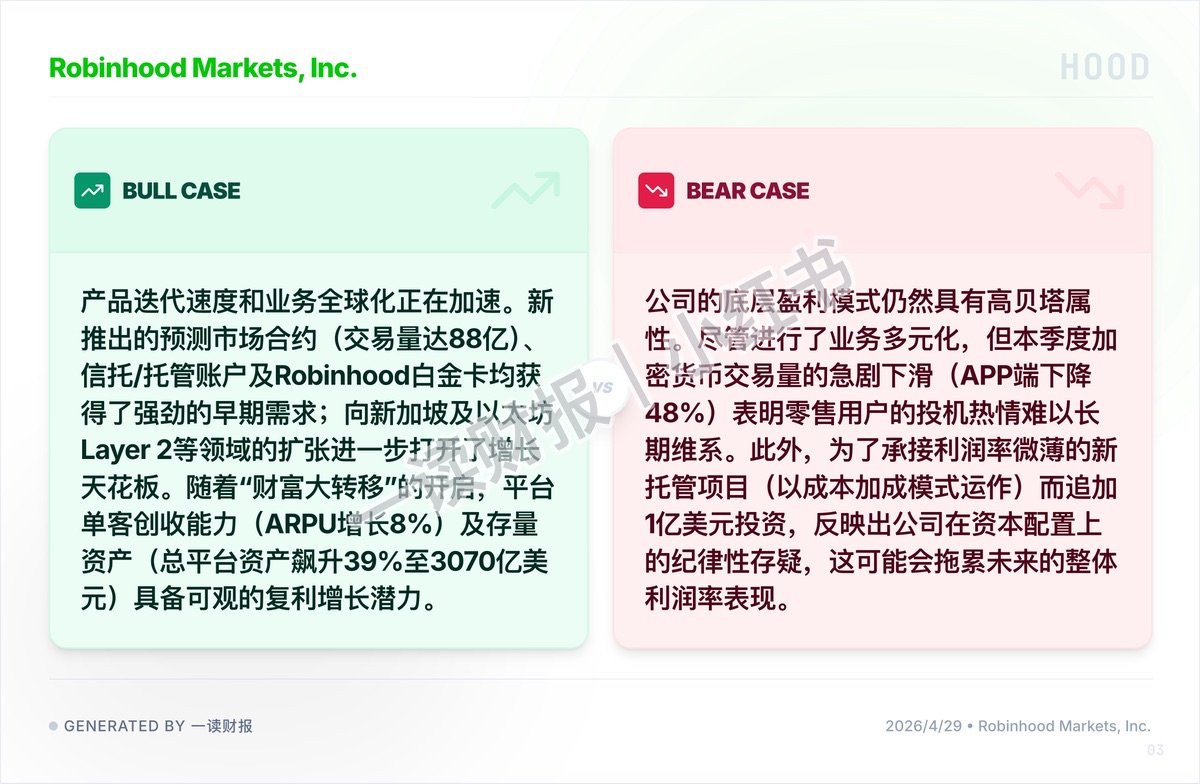

4. Strong "Wealth Transfer" and Deposit Ecosystem Moat: Despite the weakness in trading, HOOD scored a major victory in asset accumulation. It attracted a net $17.7 billion in deposits in a single quarter, Gold subscription users surged 36% year-over-year to a record 4.3 million, and total platform assets soared 39% to $307 billion. This indicates it is successfully converting platform usability into "high switching cost" stickiness through high-interest deposit-taking and credit services, deeply embedding itself into the entire lifecycle of the new generation of zero-commission investors.

5. Resilience of Options/Stock Trading and Global Expansion of New Businesses: Despite the headwinds from the crypto slump, total revenue still grew strongly by 15% to $1.07 billion (though missing market expectations). This was supported by robust options and stock trading volumes. Meanwhile, the newly launched prediction market contracts (with $8.8 billion in volume) saw extremely high early demand, and the business is decisively expanding into Singapore and Ethereum Layer 2. The accelerated pace of product iteration further raises the long-term growth ceiling for average revenue per user (ARPU).

Robinhood has maintained a facade of prosperity by relying on interest income in a high-rate environment and the asset deposits of retail investors. However, the high operating expense expectations and extreme sensitivity to its crypto business leave it lacking sufficient margin of safety at its current valuation level.

Source: Yidu Caibao, providing original earnings report downloads

#USStockEarnings #ValueInvesting #Robinhood #HOOD #BrokerageStocks #TechnicalAnalysis #BusinessMindset

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.