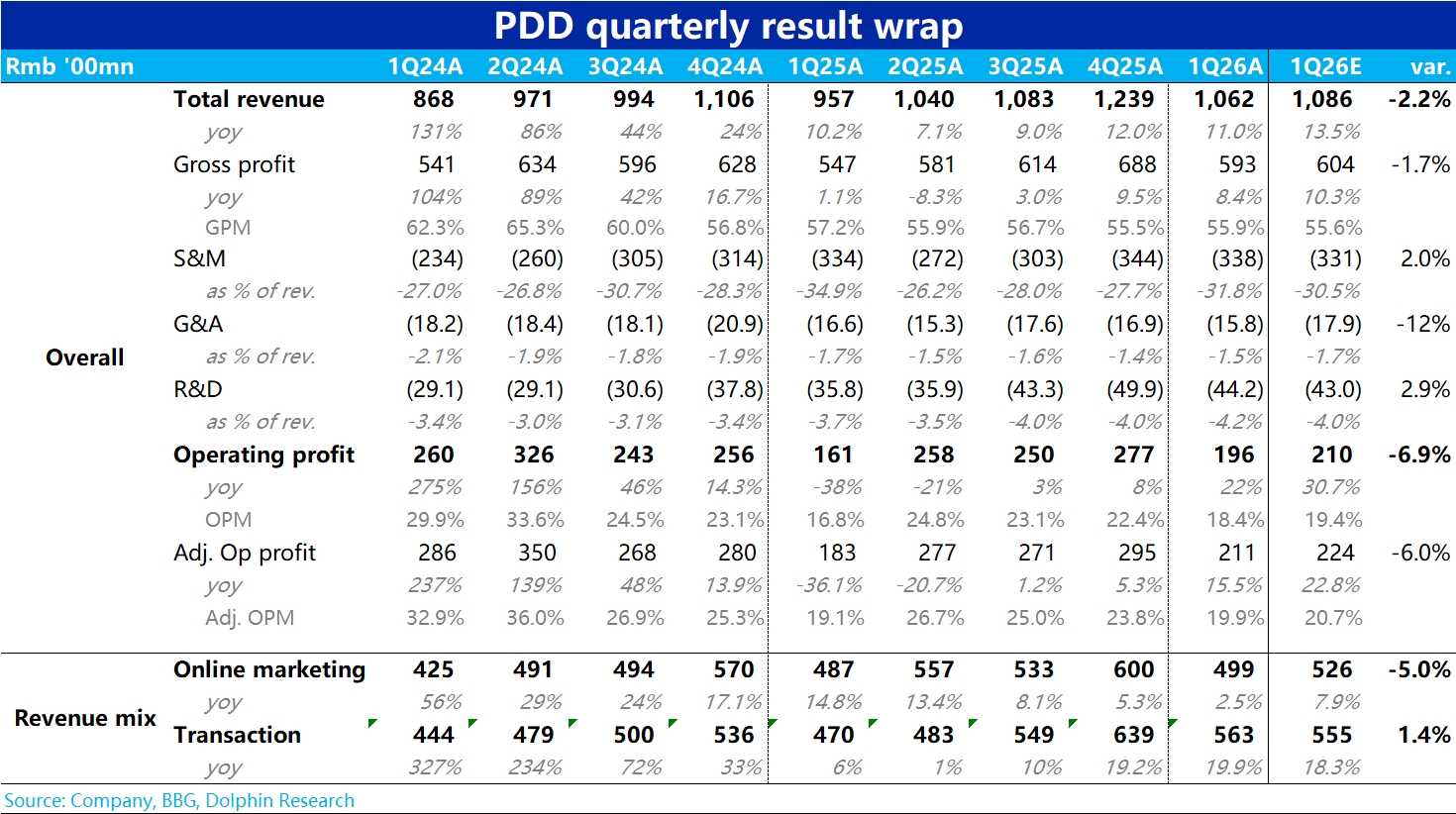

PDD 1Q26 First Take: results missed, with both revenue growth and profit below Bloomberg consensus. Details follow:

1) Total revenue rose 11% YoY, below the 13.5% the market expected. The miss was driven by marketing/ad revenue rather than transaction revenue. Marketing revenue grew just 2.5%, well under the ~8% expected.

Peers’ e-com segments accelerated vs. 4Q25, but PDD uniquely slowed QoQ. With sector GMV improving, we infer a notable drop in ad monetization. We suspect tighter e-com tax normalization hurt PDD disproportionately.

2) Commission-based revenue grew nearly 20% YoY, accelerating QoQ and slightly topping the 18% consensus. Given weak growth in the domestic core marketplace, Temu (and possibly Duo Duo Grocery) likely outperformed. That said, precise Street expectations for Temu remain fuzzy.

We estimate Temu revenue growth at approx. 25% this quarter vs. ~20% in the prior quarter. Solid, but not as exciting as media headlines about Europe and LatAm would suggest.

3) OP grew 22% YoY, with adj. OP up 15.5% YoY. While profits rebounded from last year’s trough caused by state subsidies, the recovery was ~6% below the Street. Of the ~RMB 3.5bn YoY increase in group OP, most likely came from Temu’s narrowing losses, implying limited profit growth at the core site.

Marketing spend was ~RMB 33.8bn, up 1% YoY. Given last year’s peak company-funded state subsidies, both we and the market had expected a YoY decline. $PDD(PDD.US) $PDD(PDD.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.