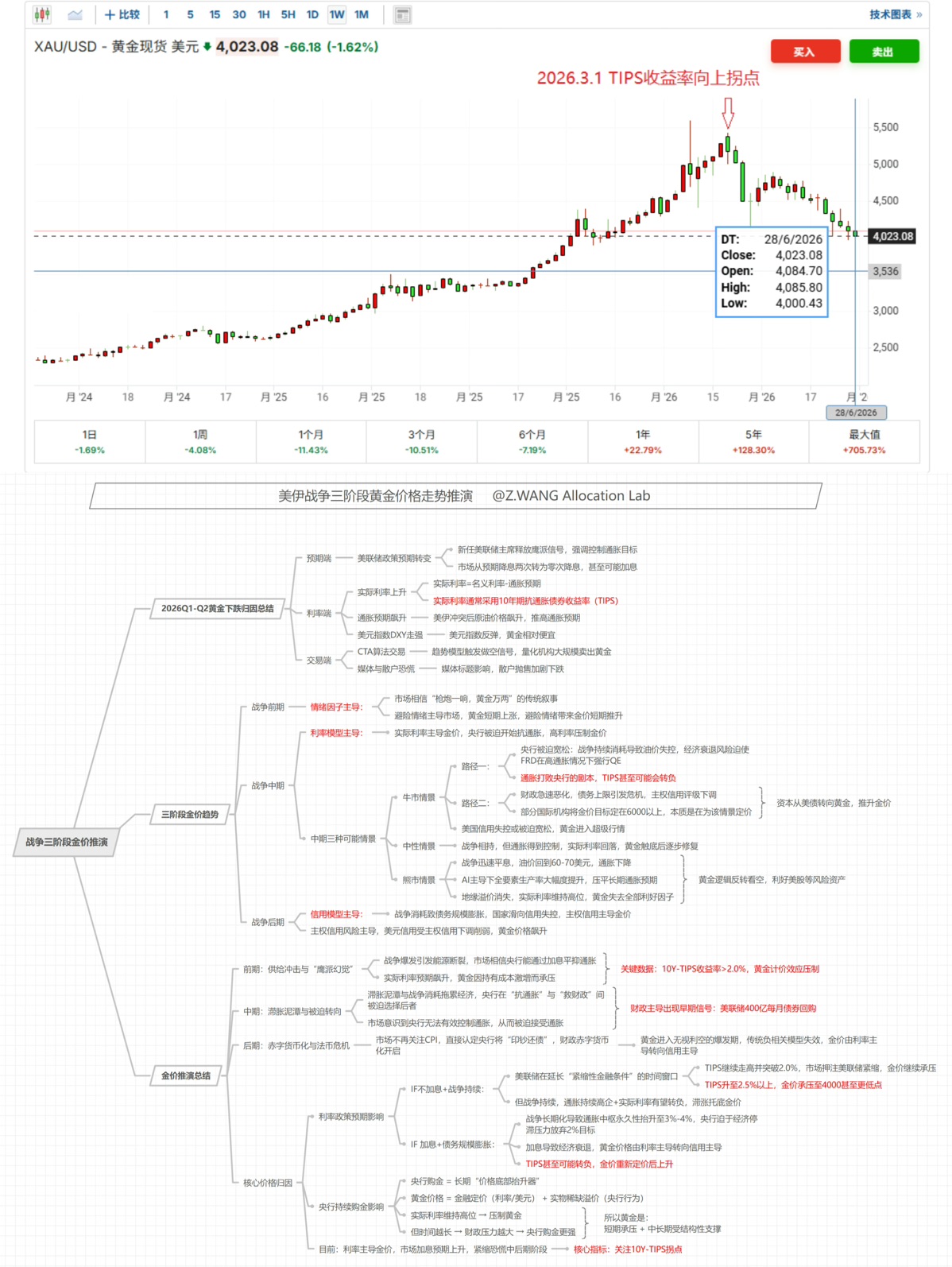

Three-Phase Gold Price Trend Projection Since the US-Iran War

The most controversial issue in the market recently is that gold continues to weaken in an environment of "high real interest rates + a strong US dollar," coupled with the Federal Reserve's persistent hawkish signals. Does this mean the previous uptrend has completely failed?

① Has the logic for gold failed?

From a traditional interest rate model perspective, the core anchoring variable for gold currently is "real interest rates (nominal rates - inflation expectations)."

TIPS data charts show that the recent 10-year TIPS have returned to above 2%, which historically corresponds to a pressured environment for gold.

Meanwhile, the US Dollar Index (DXY) remains above 100, also constituting a typical valuation suppression factor—theoretically, this combination creates a clear downward driver for gold.

② The actual price movement hasn't fully followed this logic, indicating gold is undergoing "pricing factor expansion."

· The first layer of change comes from central bank behavior.

Sustained net gold purchases by global central banks have shifted gold's marginal demand from "interest-rate-sensitive capital" to "reserve asset restructuring." This portion of demand is insensitive to real interest rates.

· The second layer of change comes from geopolitical and tail risk premiums.

Gold is reincorporating a "system uncertainty premium," including fiscal expansion, debt sustainability, and monetary credit reassessment, rather than simply being an inflation hedge.

· The third layer of change comes from structural financial mechanisms.

Gold ETFs and futures systems amplify short-term price elasticity, potentially causing periodic deviations between "paper gold pricing" and "physical marginal constraints."

Therefore, a more accurate statement is not "gold's logic has failed," but that the pricing framework has shifted from a single-factor (real interest rates) to a multi-factor (rates + dollar + central banks + credit risk) overlay model.

Under this framework, TIPS > 2% and a strong DXY only represent the "existence of a suppression factor," not a signal for the trend's end.

The key for gold is no longer whether it's cheap, but whether the global system still needs it as the ultimate credit anchor.

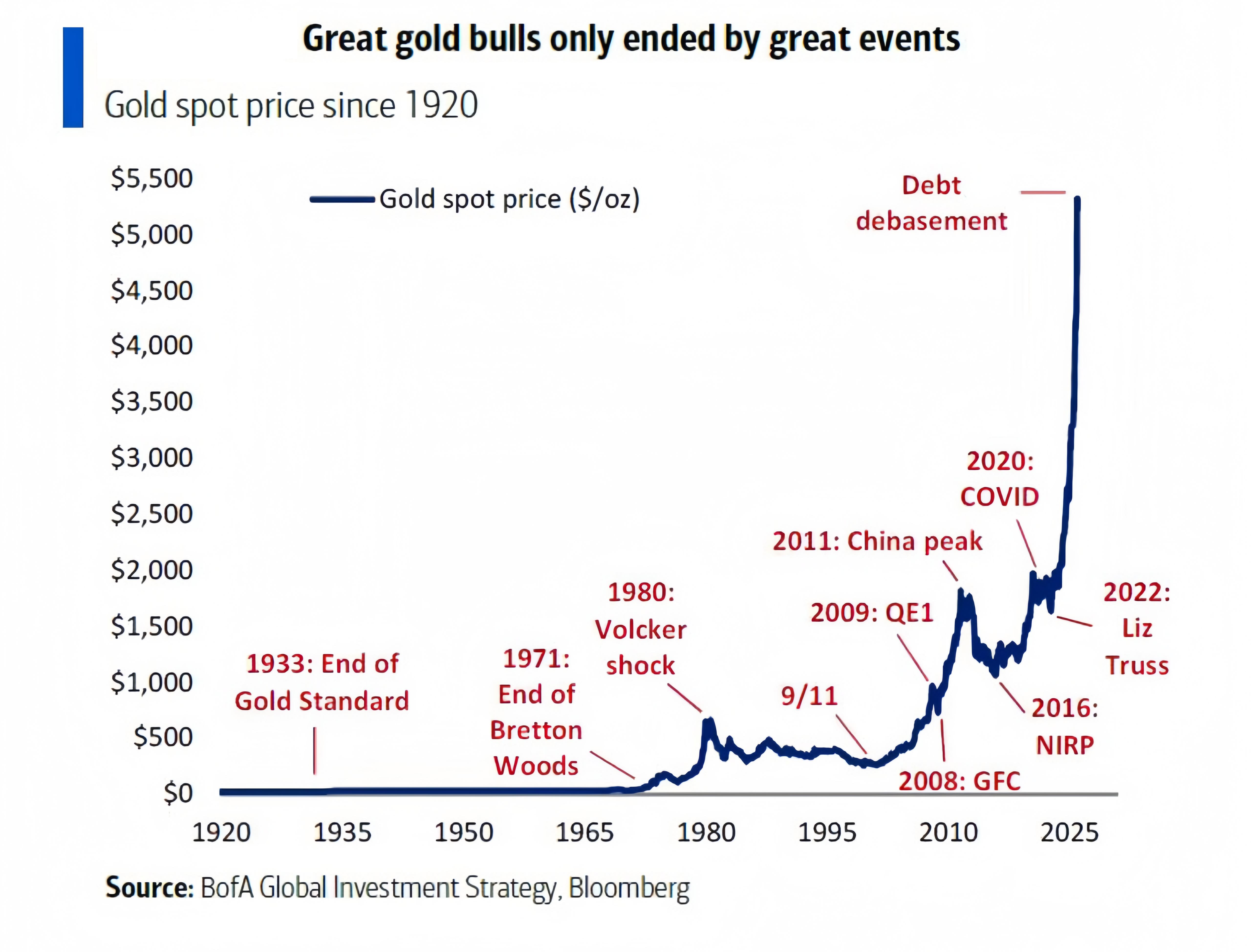

③ Gold price projection under the three-phase model since the war

In the "three-phase war model," gold typically begins to detach from real interest rate constraints during the "conflict diffusion - financialized pricing phase," entering a risk-premium-dominated range;

while in the "credit repricing phase," the market incorporates fiscal sustainability and central bank balance sheet expansion into the core of pricing.

The current situation is closer to the transition from the second to the third phase, explaining the structural reasons why gold faces short-term pressure under high TIPS and a strong dollar yet remains resilient. Simultaneously, sustained central bank gold purchases provide phased support for long-term gold prices.

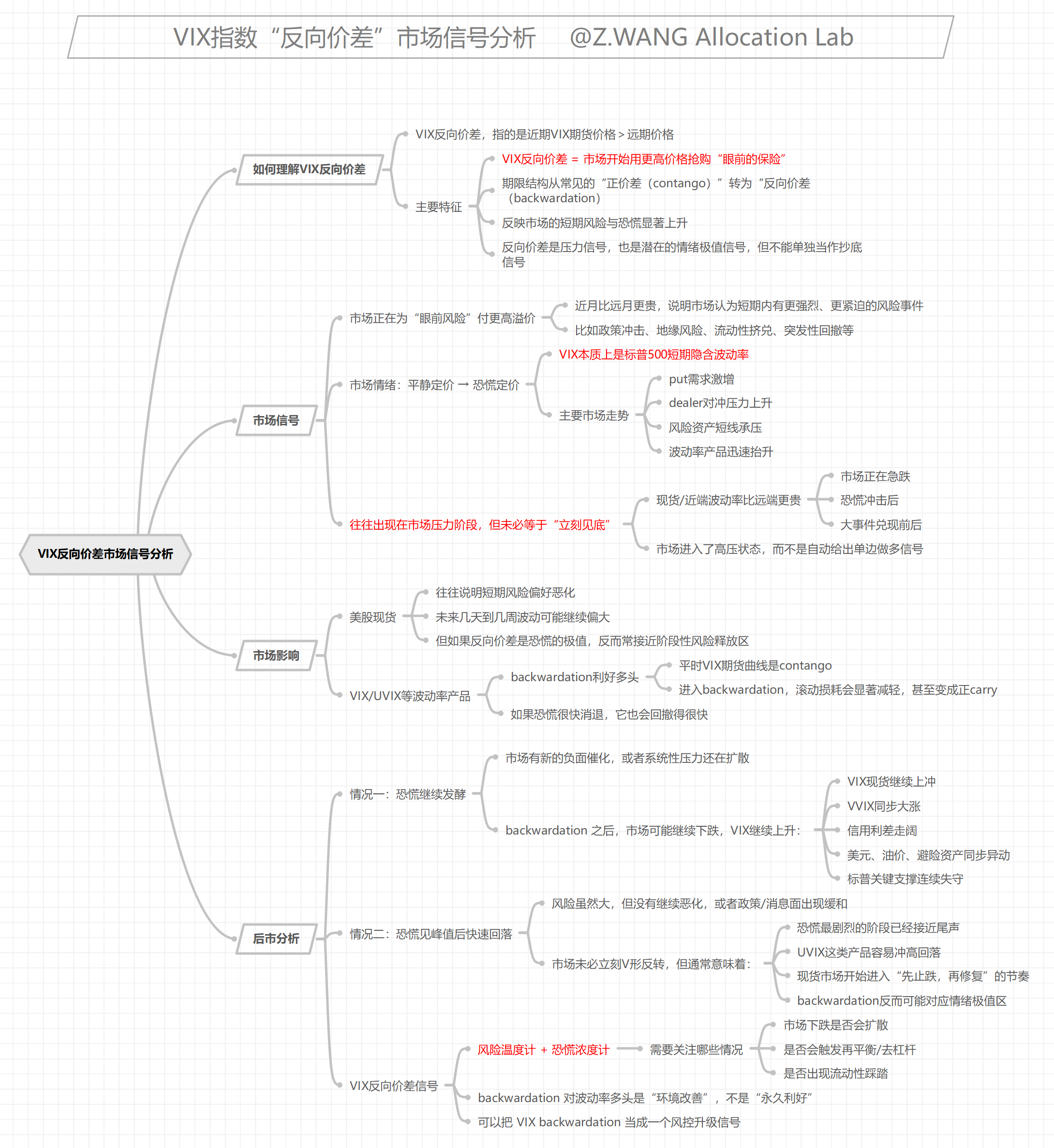

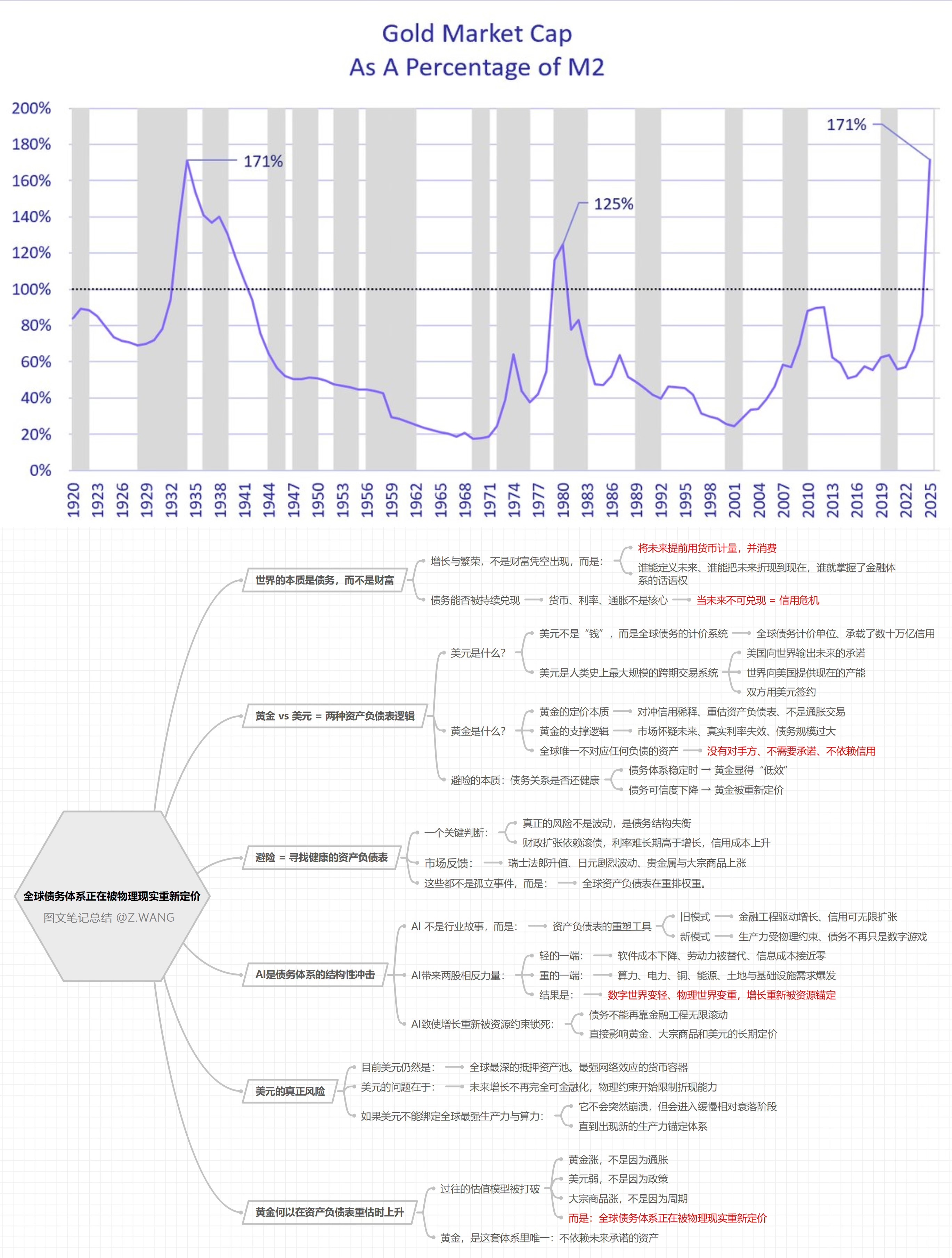

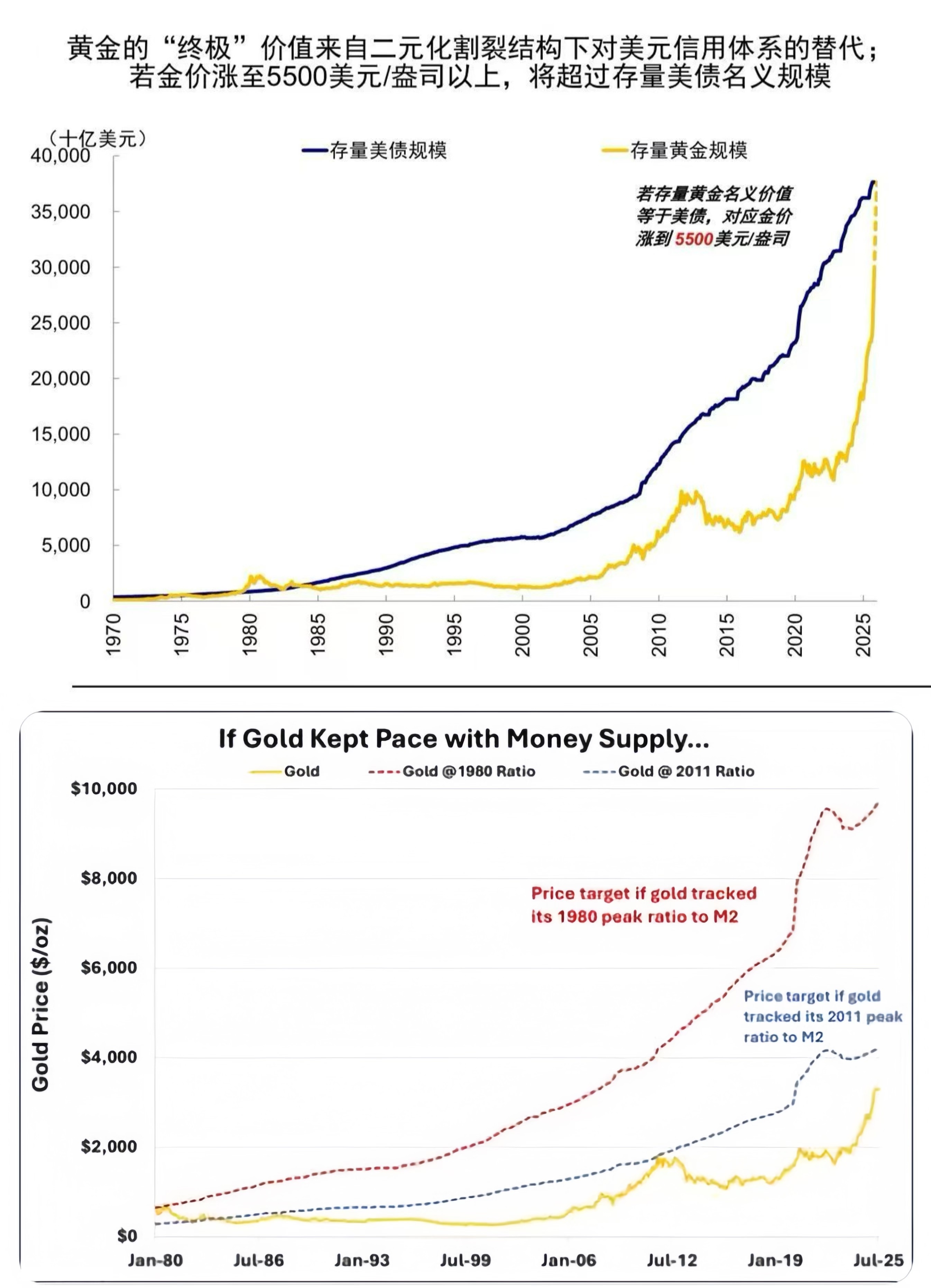

For detailed analysis, please refer to the mind map.

Data sources: TradingEconomics, Investing

$SPDR Gold Shares(GLD.US)