been holding MU since the 900s and averaged down through this whole 30% pullback. the HBM order book is basically sold out to 2028, that is not a name i want to be short into. adding on any dip under 830 🤲

Fair_Lemon5303

Hi

Fair_Lemon5303Suggestions for you to follow

F

memory into a bear market the same week samsung prints a record profit. that's the market telling you it already priced perfection. trimmed a bit of my SNDK, keeping core.

☕️ [Task Coins Giveaway] Daily Market Talk — Memory Chips Fall Into a Bear Market

The hottest trade of 2026 just cracked. Memory chips (Micron, Samsung, SK Hynix) fell into a bear market, down more than 20% from their highs, even as Samsung posted record profits. A DeepSeek in-hous...

F

memory into a bear market the same week samsung prints a record profit. that's the market telling you it already priced perfection. trimmed a bit of my SNDK, keeping core.

☕️ [Task Coins Giveaway] Daily Market Talk — Memory Chips Fall Into a Bear Market

The hottest trade of 2026 just cracked. Memory chips (Micron, Samsung, SK Hynix) fell into a bear market, down more than 20% from their highs, even as Samsung posted record profits. A DeepSeek in-hous...

F

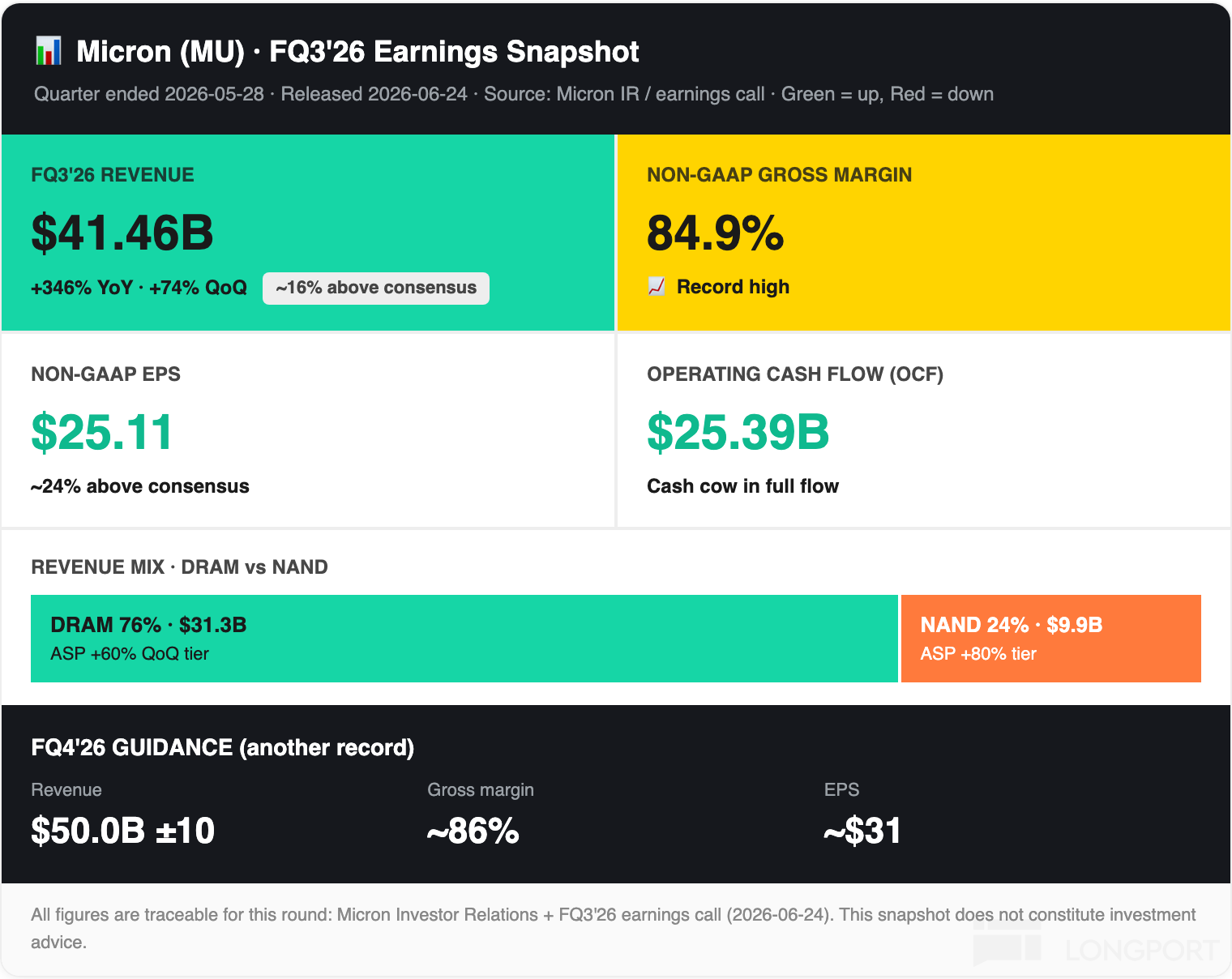

$Micron Tech(MU.US) just closed the best quarter of my investing life, up around 300 percent this year and HBM still sold out. I keep waiting for the cycle to roll over and it just doesn't. trimmed a little to lock gains but the core stays 🫡

F

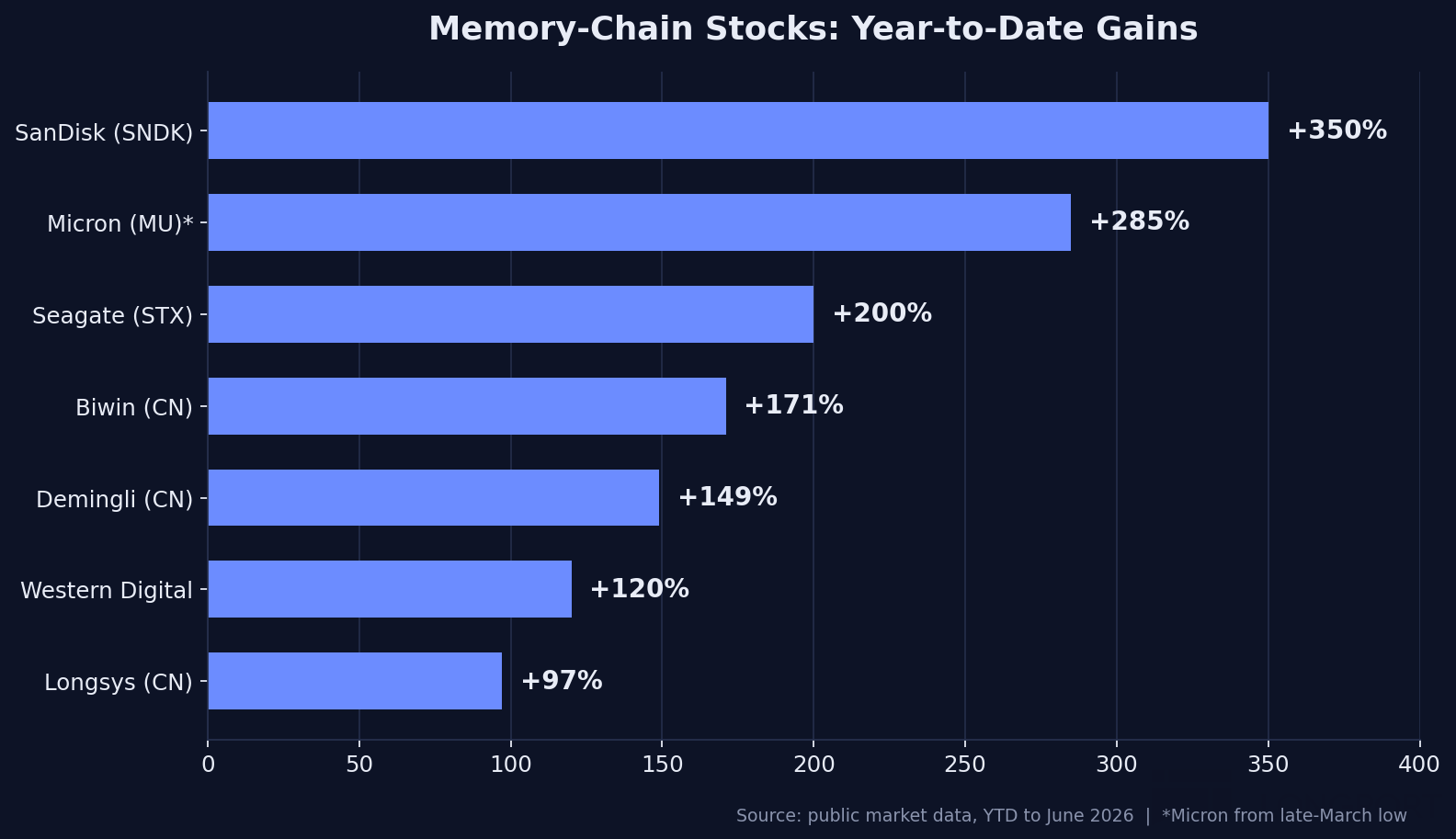

still riding this. SanDisk up 781% ytd is insane but the memory shortage is real, HBM sold out well into next year. burry has been early on nvidia for years now. holding my storage names and adding on any dip 🚀

☕️ [Task Coins Giveaway] Daily Market Talk — Burry Shorts Nvidia, Tesla & Caterpillar

US stocks just wrapped their best quarter since 2020, then Michael Burry crashed the party with fresh shorts on Nvidia, Tesla and Caterpillar, calling it an AI bubble. Back home, S-REITs are recycling...

F

still riding this. SanDisk up 781% ytd is insane but the memory shortage is real, HBM sold out well into next year. burry has been early on nvidia for years now. holding my storage names and adding on any dip 🚀

☕️ [Task Coins Giveaway] Daily Market Talk — Burry Shorts Nvidia, Tesla & Caterpillar

US stocks just wrapped their best quarter since 2020, then Michael Burry crashed the party with fresh shorts on Nvidia, Tesla and Caterpillar, calling it an AI bubble. Back home, S-REITs are recycling...

F

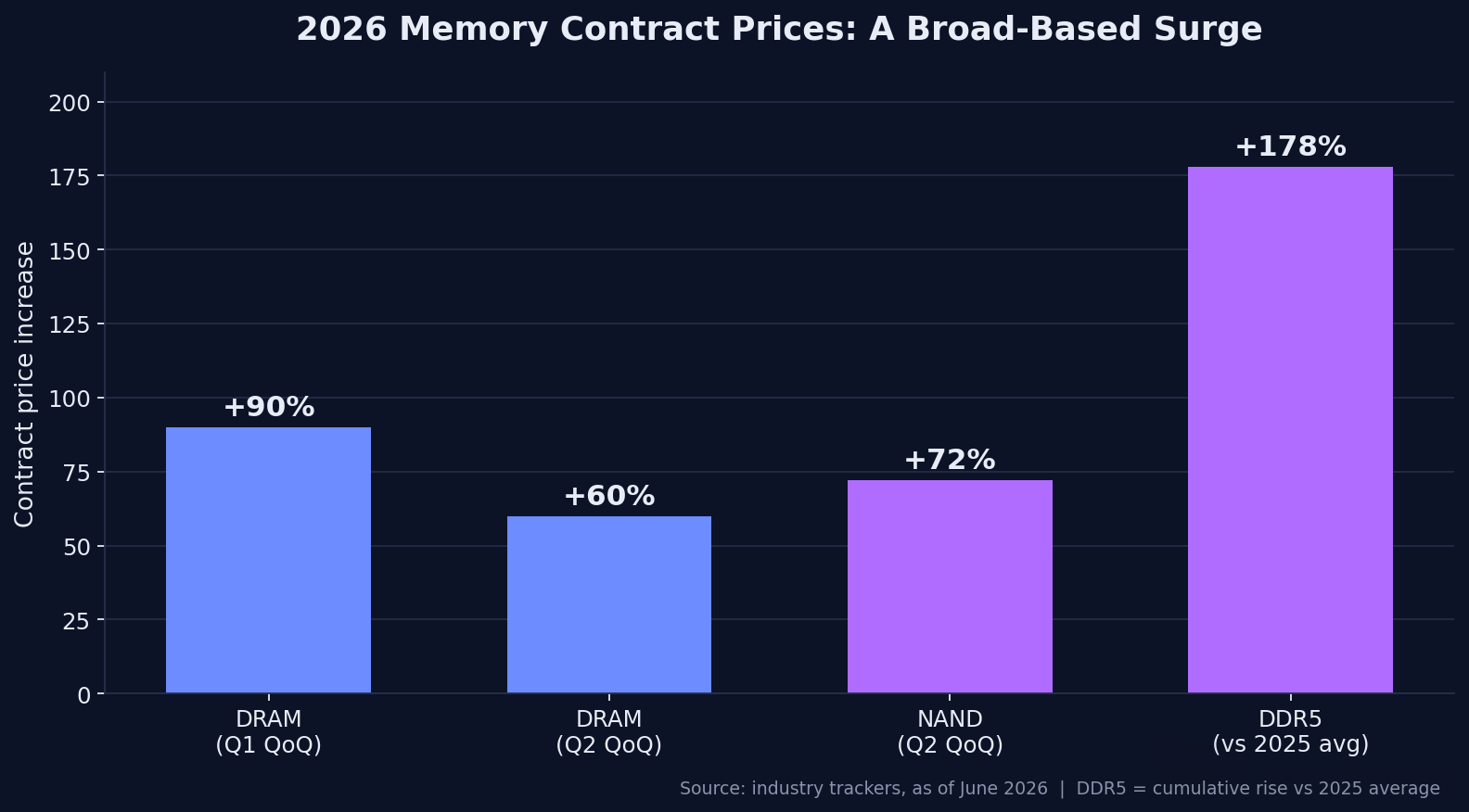

Been holding $Micron Tech(MU.US) since the 600s and the thesis hasn't changed lah. HBM4 sold out through next year, DRAM spot prices still climbing, Q4 guide pointing at around 50 billion in rev. The only thing that scares me now is my own cost basis feeling too good 😮💨

F

$Apple(AAPL.US) aside, this Micron dip is the one I'm actually watching. down 6.69% but Q4 guide is still $50B, the business didn't change in one red day. added a small tranche here, will add more if it tags $1,080.

F

Memory Stocks Are Hitting Records Everywhere — But This Isn't 2018 All Over Again

AI quietly cornered the world's memory — and turned the market's most hated cyclical into its hottest trade. Here's who's cashing in, and how to play it from the SGX.

F

+3

+3

Micron Earnings: Whether Short Orders or Long Contracts, the Pricing Power Is Still in Their Hands! The AI Memory Cycle Keeps Getting Confirmed! What Is the "SCA" the Earnings Call Kept Mentioning?

$2x Long Micron Technology ETF - Direxion (MUU.US)$$2x Long MU ETF - GraniteShares (MULL.US)$$Micron Tech(MU.US)'s earnings are out — let's take a look at the segment profits.1. Cloud Memory /...

+3Micron After the Pullback: Supercycle Still On?

F

been waiting weeks for memory to pull back and here it is. started nibbling Micron and SanDisk into the close. if the FQ3 number tonight confirms data center demand is still there, this 13% dip is gonna age really badly 👀

[Task Coins Giveaway] Daily Market Talk — Chip Rout Before Micron's Make-or-Break Night

After today's memory crash and with Micron set to report tonight, is this a dip worth buying or the first real crack in the debt-funded AI capex story?

F

been waiting weeks for memory to pull back and here it is. started nibbling Micron and SanDisk into the close. if the FQ3 number tonight confirms data center demand is still there, this 13% dip is gonna age really badly 👀

[Task Coins Giveaway] Daily Market Talk — Chip Rout Before Micron's Make-or-Break Night

After today's memory crash and with Micron set to report tonight, is this a dip worth buying or the first real crack in the debt-funded AI capex story?

F

been holding Micron since the $900s and refused to trim on the way up, now it's printed its first ever close above $1,200 and up about 7% today. the Anthropic HBM deal is the kind of multi-year anchor I was waiting for. holding straight into Wednesday's print, no fade here 🔥

F

holding my MU into Wednesday's print even with the ±12% implied move. the Anthropic deal basically locks in HBM demand thru 2026, not fading this one. did trim a third into the rip just to sleep at night though

☕️ [Task Coins Giveaway] Daily Market Talk — Micron Tops $1,200 Before Earnings

It's all about AI today. Micron ripped nearly 7% to a record above $1,200 on a long-term memory deal with Anthropic, two days before its earnings. SpaceX went the other way, cracking 16% back below it...

F

holding my MU into Wednesday's print even with the ±12% implied move. the Anthropic deal basically locks in HBM demand thru 2026, not fading this one. did trim a third into the rip just to sleep at night though

☕️ [Task Coins Giveaway] Daily Market Talk — Micron Tops $1,200 Before Earnings

It's all about AI today. Micron ripped nearly 7% to a record above $1,200 on a long-term memory deal with Anthropic, two days before its earnings. SpaceX went the other way, cracking 16% back below it...

F

MU past 1 trillion and Apple just told the whole world memory costs quadrupled. you don't get a louder demand signal than that. still long

F

gave back 6 today after that monster run. honestly healthy, nothing goes up in a straight line. still holding my core, still above 1000

F

SanDisk pulling back with the rest of storage after that parabolic run. honestly overdue, you cannot melt up forever without a breather

F

Micron Sold Off 6%. Is the Memory Supercycle Cracking, or Just Catching Its Breath?

Micron handed back about 6% on a day the whole chip complex got hit, but it is still trading above a thousand dollars. After the kind of run memory names have had, a down day was overdue. The question...

F

SanDisk around 2093 now, up 724% this year. the NAND shortage is every bit as real as HBM and it keeps printing new highs 🔥

F

MUU is the leveraged Micron play and with MU back over 1000 it is flying. only for people who can stomach 2x on a cyclical though 💪

F

memory is unstoppable right now, $Micron Tech(MU.US) back over 1000 and HBM sold out through 2026. the supercycle thesis just keeps getting confirmed 💪

F

WDC +16, Micron back over 1000, the whole storage group at records. NAND and DRAM both sold out, this supercycle has real legs 💪

☕️ [Task Coins Giveaway] Daily Market Talk — Memory Stocks Smash Records, Nasdaq Hits All-Time High

Storage chips and Nvidia power Nasdaq to a record, SpaceX tops USD 2.5T on day two, and a US-Iran ceasefire deal moves to reopen Hormuz.

F

WDC +16, Micron back over 1000, the whole storage group at records. NAND and DRAM both sold out, this supercycle has real legs 💪

☕️ [Task Coins Giveaway] Daily Market Talk — Memory Stocks Smash Records, Nasdaq Hits All-Time High

Storage chips and Nvidia power Nasdaq to a record, SpaceX tops USD 2.5T on day two, and a US-Iran ceasefire deal moves to reopen Hormuz.

F

$Sandisk(SNDK.US) printed an all time high near 2021 and closed around 1980, up 692% this year. NAND shortage is every bit as real as the HBM story and nobody is talking about it enough 💪