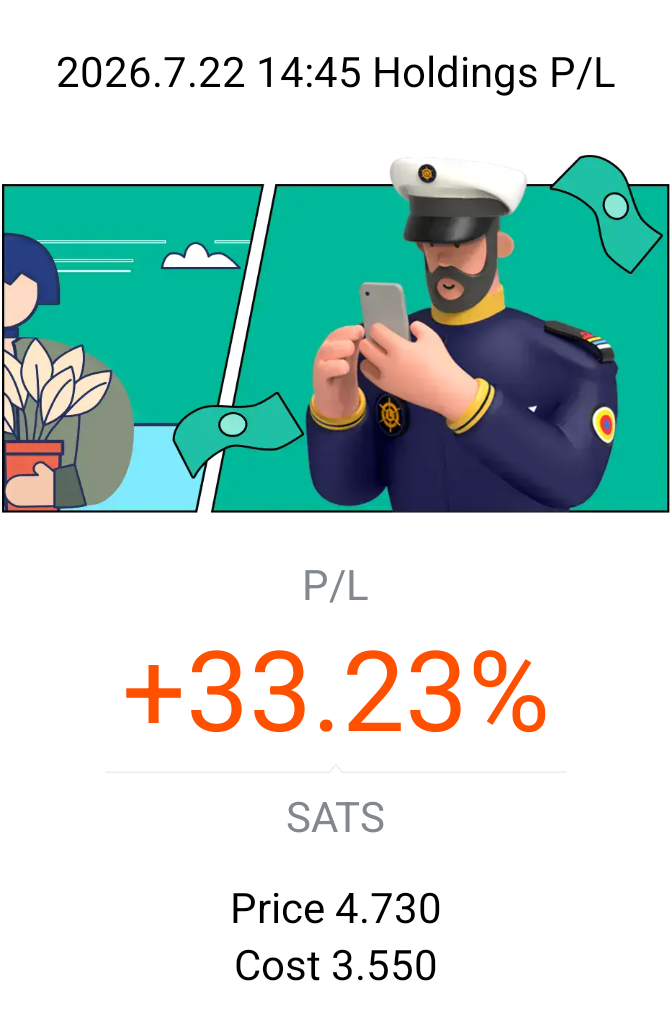

$SATS(S58.SG)

SATS has climbed to S$4.73 and is holding at a new 52-week high.

Its latest growth plan involves AI and “F1-style telemetry” across its global aviation and cargo network. But the real opportunity is not the buzzword—it is operating leverage.

SATS runs a large, complex network where small improvements in staffing, cargo flow and aircraft turnaround times can add up quickly. If the platform reduces delays and improves asset utilisation, revenue does not need to rise dramatically for margins to expand.

That matters because SATS is moving from recovery into optimisation. Aviation demand and cargo volumes have improved, earnings are recovering, and analysts have raised their targets. The next stage is proving that its expanded global footprint can generate better returns, not merely more revenue.

The risk is that the stock has already reached a fresh high, so investors are beginning to price in successful execution.

My view: the AI strategy could become a genuine margin catalyst, but the next earnings report must show measurable productivity gains. Otherwise, the headline may have moved faster than the fundamentals.