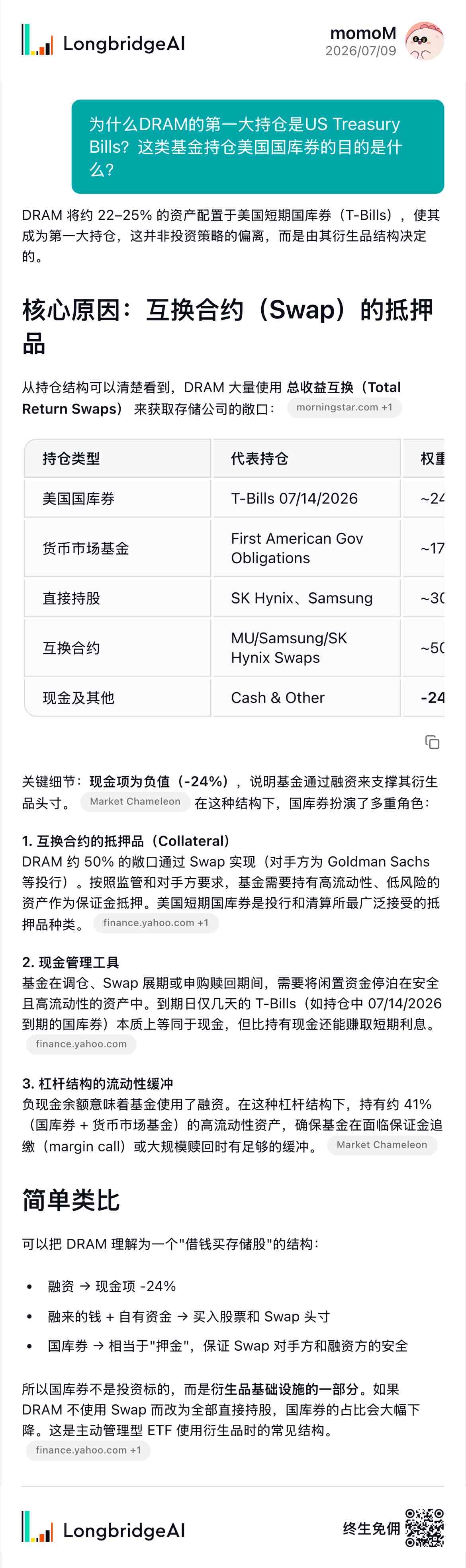

$Roundhill Memory ETF(DRAM.US) So that's how it is, financial knowledge +1

momoM

momoMSuggestions for you to follow

M

$SpaceX(SPCX.US) probably won't rise as much as our new stock today, $LIULIUMEI(06658.HK) hhhh

SpaceX

USSPCX

M

$VGT(02476.HK) South Korean retail investors' top buy【Sheng Hong Technology's core developments from April to early May 2026】

1. Business Progress: Diverging Situations Between Old and New Projects

Current main business (GB300): Production and delivery are normal. In Q1 2026, Sheng Hong's procurement of CCL (Copper Clad Laminate) increased by approximately 20% quarter-on-quarter, primarily for GB300 production.

Google Project (V8AX): The project timeline is delayed by one quarter compared to expectations. The small-batch mass production originally scheduled for Q2 2026 has been postponed to Q3. On the positive side, Sheng Hong has passed the relevant tests, received Google's order, and has begun production.

NVIDIA Rubin Platform (Next-Generation Core):

Compute Board: Previously delayed by about one and a half months due to production process issues, but overall R&D is still progressing.

Orthogonal Backplane: According to a clear schedule, the next key test is expected to be conducted and yield results in early May 2026. This is the core node the market is most focused on.

2. Market Position and Share

NVIDIA Supply Chain: In NVIDIA's switch board segment, Sheng Hong maintains a share of approximately 60%. Its share in GB300 switch board supply is also 60%, and it is expected to maintain a similar level or see a slight decline in the Rubin platform.

Competitive Landscape: Despite competition from new entrants like Jingwang Electronics, Sheng Hong's position remains solid due to its verification advantages in high-speed materials (M8) and strong production capacity reserves.

3. Capacity and Cost

Capacity Expansion: The capacity expansion plan is progressing smoothly. New capacity will be released every month in 2026, with a large amount of new capacity construction expected to be completed by year-end.

Price Trend: There is a price increase trend in the PCB industry. Sheng Hong plans to raise prices in multiple time windows such as January, March, and April 2026, passing on cost pressures (especially on the material side) to downstream customers.

VGT

HK02476

M

$XIZHI TECH-P(01879.HK), I've never seen such a huge first-day gain for a hot stock.

Trade Showcase: Trade, Show & Earn Rewards!

M

$XIZHI TECH-P(01879.HK) has a 20% clawback, so the chance of allocation should be relatively good.

M

$Tema Space Innovators ETF(NASA.US) Tema ETFs said on Tuesday that it has launched an actively managed exchange-traded fund focused on the space economy.

The Tema Space Innovators ETF provides investors with 10% direct exposure to SpaceX through a special purpose vehicle structure provided by Forge, a subsidiary of Charles Schwab (SCHW).

Tema ETFs said the fund's holdings include AST SpaceMobile (ASTS), Rocket Lab (RKLB), Planet Labs (PL), EchoStar (SATS), and Intuitive Machines (LUNR).

Echostar

USECHO

M

$AMD(AMD.US) has basically confirmed a 10-15% price increase for PC CPUs, but whether server CPUs will see a price hike is still under internal discussion. AMD is being cautious in its decision-making, as its core goal for 2026 is to capture 50% of the global data center server CPU market share, which was over 40% as of Q3 2025. Typically, AMD prioritizes price competition over price hikes to gain market share. Therefore, server CPUs are highly likely to see no price increase or only a minimal one.

$Intel(INTC.US) has not officially announced any price increases, but the market is experiencing severe shortages. This mainly affects fourth- and fifth-generation server CPUs, with around 40-50 models generally out of stock, and delivery cycles extended to 16-24 weeks. The shortages stem from overly optimistic demand forecasts for sixth-generation CPUs at the end of 2024, which led to a shift in production capacity toward the sixth generation. However, actual market demand in 2025 remains concentrated in the fourth and fifth generations (over 75% share), and North American CSPs placed large additional orders for fourth- and fifth-generation CPUs in Q2 and Q3, sparking hoarding expectations. Some domestic OEMs have proactively proposed price increases to shorten delivery times, but this is an individual action, not an official Intel strategy. Intel may use a strategic 10-20% price increase not to boost revenue but to narrow the price gap between the fourth/fifth generations and the well-supplied sixth-generation products, steering demand toward the sixth generation and optimizing production capacity.

(Repost)

AMD

USAMD

M

$Sandisk(SNDK.US) A simple analogy: Imagine a chef working on a tiny cutting board (HBM). Every time a customer adds a request—"No onions... Wait, add onions... Now make it vegetarian... And add a side dish"—these sticky notes (context/KV cache) pile up on the board. Eventually, the board is covered in notes, and the chef can't chop; this expensive chef just stands idle. The so-called "architectural refactoring" is simply establishing a reasonable kitchen workflow: Keep the most urgent notes on the cutting board (HBM), move "important but not immediate" notes to the prep table next to it (DRAM), and store the rest in a nearby filing cabinet/pantry (enterprise SSD). Then, you add a runner and an organizer (DPU + network) to fetch and place the right notes at the right time, allowing the chef to cook at full speed—this means higher throughput, lower per-token cost, and less wasted GPU time.$Micron Tech(MU.US)

Sandisk

USSNDK

M

$Sandisk(SNDK.US)NVIDIA's BlueField-4 redefines AI storage hierarchy, NAND demand opens incremental space [Northeast Computer]

Significance: NAND is no longer just a data storage hard drive, but directly participates in the inference process. #We believe this means a leap in storage valuation logic—from cyclical products to AI computing companions. #Consistent with our previous emphasis, #2026 storage narrative will change.

Space calculation: Single cabinet NAND demand surges 5x, supply-demand tension intensifies based on NVL72 Rubin architecture

1) #Single cabinet increment: Traditional GB200 NVL72 NAND configuration is about 830TB. Under the new BlueField-4 architecture, each GPU adds 16TB context space, 72 GPUs correspond to 1152TB new demand.

2) #Total capacity change: Single cabinet NAND capacity will skyrocket from ~830TB to nearly 2PB, #single cabinet usage increases over 140%. Assuming 100k Rubin architecture cabinets (including NVL72 & NVL36 conversions) shipped in 2026, new demand reaches ~115.2EB. Referencing 2025 global NAND supply (~931EB, assuming 10% growth in 2026), NVIDIA AI servers alone will account for 10.5% of global capacity. Given the high barrier of enterprise eSSD, structural shortages will emerge in high-end NAND wafers and controllers.

$Micron Tech(MU.US)

Sandisk

USSNDK

M

$BIREN TECH(06082.HK) is easy to win in the lottery, Group B with three lots, grateful for the last trading day's inclusive big red envelope🧧

M

$Tesla(TSLA.US)What a unique badge! Longbridge is really dedicated to supporting trading discipline$NVIDIA(NVDA.US)

Share My Wealth Memories 2025

M

$INSILICO(03696.HK) first all in this, then top up $FOREST CABIN(02657.HK)

INSILICO

HK03696

M

$Rocket Lab(RKLB.US)Update: 1) RKLB has mastered small rocket recovery technology, and improving profit margins relies on increasing launch frequency to lower average fixed costs, which is also RKLB's strength. In 2022, it achieved a record of 9 launches, and as of November this year, it has already conducted 18 launches, setting another company record while maintaining a 100% success rate, theoretically allowing for lower insurance costs. Gross margin has increased from about 27% last year to 37% recently, and losses are also shrinking.

2) RKLB's performance in the small rocket business is nearly perfect. To reach the next level, it needs to acquire the technology to launch larger rockets. RKLB

predicts that the gross margin for the medium-sized Neutron rocket could reach

40% to 50%, significantly higher than Electron's approximately 30%, mainly due to greater payload capacity and higher launch prices ($50M to $55M), with internal costs expected to be controlled within the $25M to $30M range. Additionally, greater payload capacity will also attract more heavyweight clients, boosting revenue and valuations.

RKLB has been working hard this year to advance the first launch of the Neutron rocket, but the latest announcement delays it to the first quarter of next year.

RKLB is somewhat like SpaceX five years ago or earlier, gradually moving from small rockets to larger ones. SpaceX is, of course, the industry leader, with massive rocket scale and payload capacity, and has already achieved recovery, along with NASA as a major client.

Rocket Lab

USRKLB

M

$Apple(AAPL.US) Now it's clear the market doesn't see you as an AI stock at all, completely unaffected by AI news...

Apple

USAAPL

M

$Tesla(TSLA.US) Is it going to announce the cooperation with $Archer Aviation(ACHR.US) tomorrow?

Archer Aviation

USACHR

M

Red lines and yellow lines are built for AI robots, blue lines are built for real people$Coreweave(CRWV.US)$Oklo(OKLO.US)$Serve Robotics(SERV.US)$SH ELECTRIC(02727.HK)$NVIDIA(NVDA.US)$Nebius(NBIS.US)

SH ELECTRIC

HK02727

M

$KUAISHOU-W(01024.HK)转:【Coco Tech Internet Sora2 Thoughts 20251002】Still can't get the invitation code, so I can only take a look around X and see the community feedback:

1. Justin Moore, a partner at A16Z, believes that Sora 2's success lies more in the product side, with Cameos and Remixing being two particularly great features that have inspired users' AIGC creative desires—such as making videos of themselves with Altman in the same frame and remixing favorite characters and clips (like putting Pikachu on the Titanic).

2. Justin tested it himself, comparing the video footage of gymnastics, and found that Sora2's generation effect is not more stable than Kling2.5. Other users have also reported that price is an important factor in AIGC creation.

3. The release of the Sora App has further advanced the impact of AI creation on existing short video platforms. I previously wrote that there might be no real influencer live streams in the AI era (*recently, Baidu shared that their digital version of Luo Yonghao is even hard to distinguish from the real one), which means the moat of short video platforms could be reconstructed, and the barriers of original content and creators may change. The future belongs to: social + model innovation features, which is very favorable for Kuaishou's layout.

As we mentioned in our roadshow, the current Kuaishou is equivalent to buying a dividend stock (with net cash of 100 billion and annual net profit of 20 billion) and getting the world's top-tier model Kling and a 1% long-term option for free—Kuaishou's competitive share in the AI era seems to have further opportunities.

KUAISHOU-W

HK01024

M

$ZIJIN GOLD INTL(02259.HK) Keeping two hands to squat in was right, although I didn't have the courage to buy heavily on the first day, still not good at trading new stocks

M

$ZIJIN GOLD INTL(02259.HK) Sold 200 out of 400, current market cap just reached the fast-track inclusion threshold for Stock Connect, ready after the 17th, reference:

If a new stock's closing market cap on its first trading day enters the top 10% of the Hang Seng Composite Index, it will be included in Stock Connect after ten trading days

1. Hang Seng Composite Index has 500 constituents, the 50th being China Unicom H at HKD 250 billion

2. If Zijin Gold's post-listing market cap reaches HKD 250-270 billion on 9.30, it will (soon) enter the Hang Seng Composite Index

3. As it has no A-shares, it will be included in Stock Connect on 10.17 (HK market closed on 10.1 and 10.7)

M

$TSLA 251003 470 Call(TSLA251003C470000.US)Heard there's a large order betting on 470 next week$Tesla(TSLA.US)

USTSLA251003C470000

M

$ZIJIN GOLD INTL(02259.HK)Key point: The company's compound annual growth rate (CAGR) of production from 2022 to 2024 reached 21.4%, ranking first among the world's top 15 gold companies, far exceeding the second place's 9.3% growth rate. During the same period, the CAGR of revenue was 28.2%. Coupled with the Fed's interest rate hike cycle and the rising gold market, the company's performance growth is expected to continue.

In summary, the company has advantages in resources, operational efficiency, and profitability, with strong potential for sustained growth and excellent fundamentals.

From the perspective of this issuance structure, the sponsors are Morgan Stanley and CITIC, a strong alliance. There are 29 cornerstone investors, even surpassing CATL's 23, with a mix of well-known domestic and foreign investors, making the lineup quite impressive. Although the clawback mechanism B is used, the fundraising amount is substantial at HKD 24.98 billion, second only to CATL's HKD 31 billion IPO in May 2025 on the Hong Kong stock market. It is the second-largest IPO in Hong Kong this year, with a public offering of HKD 2.498 billion and a large volume, which helps improve the lottery success rate.

From a market sentiment perspective, recently listed Health 160 and GenFleet Therapeutics saw their grey market and first-day trading prices rise by over 100%. Since the implementation of the new rules, no B-share mechanism stock has broken its issue price. Moreover, Zijin Gold International has excellent fundamentals and is unanimously favored by institutions. Subscription enthusiasm is expected to be high. As of 16:51 on September 19, the public offering margin financing amount was HKD 14.772 billion, oversubscribed by 4.91 times. Additionally, according to the inclusion rules of the Stock Connect, if the company's market capitalization on the first day of listing ranks in the top 10% of the Hang Seng Composite Index constituents, it will be directly included in the Hang Seng Composite Index after the 10th trading day, effective on the 11th trading day. The current inclusion threshold is HKD 164.619 billion. Zijin Gold International is expected to be included in the Connect on the 11th trading day. Interested investors can continue to monitor the subscription situation of this stock.

M

$ZIJIN GOLD INTL(02259.HK)28 cornerstone investors, the first time I've seen so many in my memory

Forward a meeting minutes: Zijin Gold International PDIE Minutes

1. As of now (excluding the newly acquired Kazakhstan project in 2025), the total reserves of existing mines are about 845 tons, of which 435 tons were added through independent exploration, demonstrating its strong exploration capability.

2. Production: 26/27 years respectively

57/60 tons, 100 tons in 30 years. To achieve the 2030 target, the company plans to supplement 30 tons of production through M&A, focusing on projects close to production with annual capacity ≥5 tons

3. 25H1 actual all-in sustaining cost

(AISC) $1548/oz

4. For every 1% increase in gold price, it is expected to drive 2.4% growth in the company's 2026 EPS

5. If using $3600/oz gold price assumption, the 2026 implied P/E ratio would drop to 11-14x

ZIJIN GOLD INTL

HK02259