U.S. Equity ETF Portfolio Allocation: The Complete Guide to the Classic 60/40 Strategy

Summary: The 60/40 ETF portfolio is the investment industry's best-known asset-allocation framework: 60% equities for growth, 40% bonds to manage volatility. This article unpacks its logic, ETF selection, and rebalancing mechanics.

TL;DR: A 60/40 ETF portfolio is a long-term investment framework that allocates 60% of capital to equity ETFs and 40% to bond ETFs. Historically, this portfolio has generally delivered positive long-term returns, with volatility lower than an all-equity portfolio. However, actual figures vary depending on the indices used and the time period measured, and past performance is not indicative of future results. Although both stocks and bonds fell in 2022, the diversification rationale behind this strategy remains of interest to many market analysts—the key is choosing the right ETFs and rebalancing regularly.

For many Hong Kong investors who are new to US equities, facing thousands of ETF choices often makes it hard to know where to start. In fact, for decades the investment world has circulated a simple framework: allocate 60% of capital to stocks and 40% to bonds. This “60/40 ETF portfolio” concept originates from Modern Portfolio Theory. Its core idea is to use the low correlation between asset classes to reduce overall volatility while targeting the same return objective.

Below, we break down the core logic of the 60/40 ETF portfolio, commonly used ETF pairings, how rebalancing is carried out, and the strategy’s applicability and limitations in today’s market.

What Is a 60/40 ETF Portfolio

The concept of a 60/40 ETF portfolio is straightforward: allocate 60% of your investment capital to equity ETFs to pursue long-term growth; allocate the remaining 40% to bond ETFs as a buffer to reduce overall volatility.

Behind this ratio is an important assumption: stocks and bonds tend to be negatively correlated or weakly correlated under most market conditions. When the stock market falls, investors often rotate into safe-haven assets, pushing bond prices up and partially offsetting equity losses. This offsetting dynamic makes the portfolio’s overall volatility far lower than that of an all-equity investment.

Understanding the difference between active and passive management helps explain the characteristics of ETFs when building this kind of portfolio: they typically offer relatively lower costs, higher transparency, and flexible trading, but they also have limitations such as tracking error, liquidity differences, and exposure to market volatility risk.

Looking at long-term data over the past several decades, 60/40 portfolios have generally produced positive overall returns, and their annualized volatility has been clearly lower than that of all-equity portfolios—one reason this framework has long attracted attention. That said, specific return and volatility figures can differ materially depending on the equity and bond indices used and the measurement period, and past performance is not indicative of future results.

Common ETF Selection Approaches

When building a 60/40 ETF portfolio, selecting appropriate ETFs is key. Below are several common pairings, provided only as examples of typical approaches and not as buy/sell recommendations:

Approach 1: S&P 500 ETF + US Aggregate Bond ETF

One well-known combination uses an equity index ETF that tracks the S&P 500 Index for the equity portion, paired with a bond ETF that tracks the US aggregate bond market for the bond portion, providing exposure to US large-cap stocks and a diversified bond universe.

Approach 2: US Total Stock Market ETF + Bond Market ETF

This approach uses an equity index ETF tracking the total US stock market (including large-, mid-, and small-cap stocks) instead of a pure S&P 500 ETF, allowing the equity portion to be more broadly diversified into mid- and small-cap companies and reducing concentration risk.

Note: ETFs differ in expense ratios, tracking error, and liquidity. The examples above are for illustrative purposes only. Before investing, you should independently review the relevant product information and risks.

The Role of Bond ETFs: What It Takes to Be a Stabilizer

The role of bonds in a 60/40 portfolio is more nuanced than many investors assume. Understanding bond yields and credit risk is a prerequisite for assessing whether a bond ETF can truly serve as a buffer.

Based on many years of market data, bonds have delivered positive returns in most years and have outperformed equities in some years—this is the foundation for their buffering role in a portfolio. However, whether bonds can genuinely provide protection still depends on the interest-rate and inflation environment at the time.

The Exception in 2022

The year 2022 was the biggest test for the 60/40 portfolio in recent years. The Federal Reserve raised interest rates sharply to fight inflation, causing bonds and equities to decline simultaneously and resulting in significant losses for the year. Afterward, as the rate-hiking cycle approached its peak, the market generally observed that the pressure from simultaneous stock-and-bond declines eased. Even so, the stock-bond correlation fluctuates with the macro environment and is not fixed.

Duration Management

When selecting bond ETFs, duration is an important consideration. The longer the duration, the more sensitive the ETF is to interest-rate changes. Some investors prefer to keep the average duration of their bond ETF allocation below five years to balance yield and interest-rate risk.

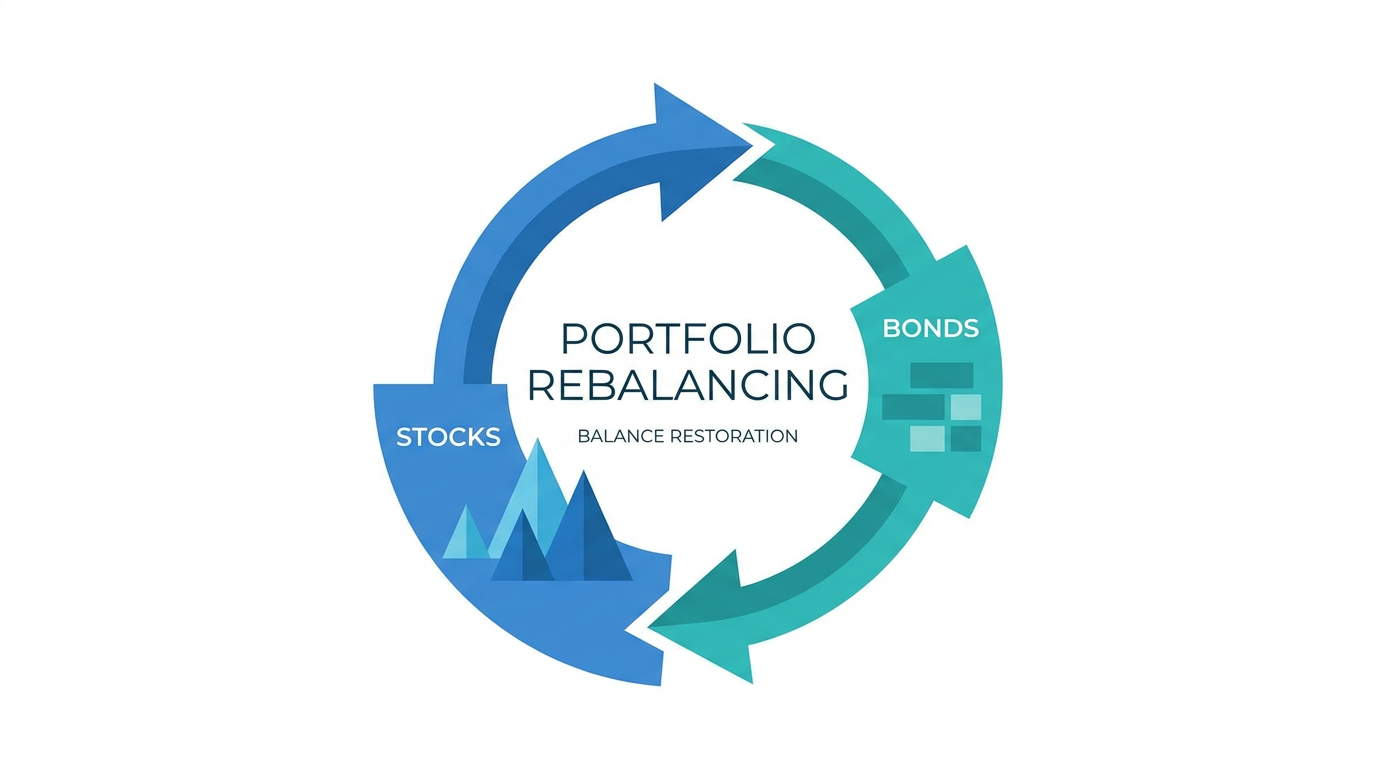

How to Execute Rebalancing

Rebalancing is the core operational step in maintaining a 60/40 portfolio. Over time, market moves can cause stock or bond weights to drift away from target. For example, after a strong equity rally, the actual portfolio mix may shift from 60/40 to 70/30—at which point an adjustment is needed.

Understanding the principles of asset rebalancing can help you set a rebalancing frequency and trigger conditions that suit you.

The 5% Threshold Rule

Set a “5% deviation threshold”: when the actual stock or bond allocation deviates from its target by more than 5 percentage points, rebalance the portfolio back to 60/40. This approach avoids overly frequent trading while effectively preventing the allocation from drifting too far.

Periodic Rebalancing

Review the portfolio on a fixed schedule—such as quarterly or annually—and decide whether to adjust based on how far it has drifted. For most long-term investors, once or twice a year is sufficient; rebalancing too frequently may instead increase transaction costs.

Note: Rebalancing should take transaction fees and potential tax implications into account. It is advisable to review Longbridge’s trading fees in advance to ensure rebalancing delivers practical benefits.

Adjusting the Allocation Based on Personal Circumstances

60/40 is not a fixed ratio. Investors can adjust it based on their own circumstances:

- Age: The “110 minus age” rule can serve as a reference, using 110 minus your age as the equity allocation percentage. A 30-year-old might consider roughly 80% in stocks, while a 50-year-old might adjust that to around 60%. Younger investors, being further from retirement, can generally tolerate a higher equity allocation.

- Risk tolerance: If portfolio declines already feel hard to endure, your equity allocation may be too high. In that case, you may consider adjusting to 50/50 or even 40/60.

- Inflation environment: In environments such as stagflation—slowing economic growth combined with high inflation—the diversification effect of a traditional stock-bond portfolio may weaken, and both asset classes may come under pressure at the same time. Some investors therefore consider adding commodities to diversify risk, but this should be decided based on one’s own understanding.

Frequently Asked Questions

Is a 60/40 ETF portfolio suitable for Hong Kong investors?

The core logic of a 60/40 ETF portfolio is equally applicable to Hong Kong investors. When trading US-listed ETFs, investors should pay attention to related fees and foreign-exchange risk. US interest-rate trends also have a major impact on US bond ETFs.

After stocks and bonds both fell in 2022, is the 60/40 portfolio still viable?

2022 was a relatively rare environment marked by an inflation shock and accelerated rate hikes. Afterward, as the rate-hiking cycle approached its peak, the market generally observed that the pressure from simultaneous stock-and-bond declines eased. Some market analysts believe the diversification rationale of the 60/40 strategy still applies, but the stock-bond relationship changes with the macro environment. Investors therefore need to be mentally prepared for short-term drawdowns under extreme conditions.

Conclusion

A 60/40 ETF portfolio provides a simple asset-allocation framework that enables investors to achieve long-term diversification across stocks and bonds with a relatively low barrier to entry. Based on historical data, this portfolio has generally delivered positive overall returns, with volatility clearly lower than that of an all-equity portfolio. The simultaneous decline in stocks and bonds in 2022 was an important reminder: under certain macroeconomic conditions, the diversification assumption may temporarily fail. Investors need to clearly understand the strategy’s limitations and adjust the allocation based on age, risk tolerance, and goals.

Which investment instrument to choose depends on your investment objectives, risk tolerance, market views, and experience level. Whatever you choose, you must fully understand how it works, its risk characteristics, and trading rules, and put in place a sound risk management plan. Longbridge Securities provides US stocks and ETF trading services. You can learn more about investing through Longbridge Academy or download the Longbridge App.