Cash Flow Statement: Tracking Money In and Out

A cash flow statement tracks the movement of cash in and out of your business, helping you understand liquidity, manage expenses, and make informed investment decisions.

TL;DR: A cash flow statement tracks the actual movement of cash in and out of a business through three key categories: operating activities (daily business operations), investing activities (asset purchases and sales), and financing activities (debt and equity transactions). Unlike profit calculations, it shows real cash availability, helping businesses manage liquidity and investors evaluate financial health.

Understanding where your money comes from and where it goes is fundamental to financial success. A cash flow statement provides this critical visibility by tracking the actual movement of cash through your operations, investments, and financing activities. While an income statement may show profitability, only a cash flow statement reveals whether you have enough cash on hand to meet immediate obligations.

For investors trading across Singapore, United States, and Hong Kong markets, understanding cash flow statements becomes doubly important. These statements help evaluate the financial health of companies you're considering for your portfolio. According to Harvard Business School Online, the statement of cash flows bridges the gap between the income statement and balance sheet, providing a complete picture of financial liquidity. Longbridge offers financial education resources to help investors understand key financial concepts.

What is a Cash Flow Statement?

A cash flow statement is a financial report that details how cash entered and left a business during a specific reporting period, typically a month, quarter, or year. According to the Corporate Finance Institute, this statement shows how changes in balance sheet accounts and income affect cash and cash equivalents.

The key distinction that makes cash flow statements invaluable is their focus on actual cash transactions rather than accounting profits. A company can report strong profits on its income statement while simultaneously running dangerously low on cash reserves. This scenario occurs because income statements record revenue when earned (not necessarily when cash is received) and expenses when incurred (not necessarily when cash is paid).

Why Cash Flow Matters More Than Profit

Consider a manufacturing business that secures a substantial contract and records the revenue immediately. However, if the customer pays on 90-day terms while the manufacturer must purchase raw materials and pay employees immediately, the business could face a cash crisis despite showing accounting profits. For investors, examining a company's cash flow statement helps identify businesses with genuine financial strength. Companies with consistent positive cash flow from operations typically demonstrate sustainable business models.

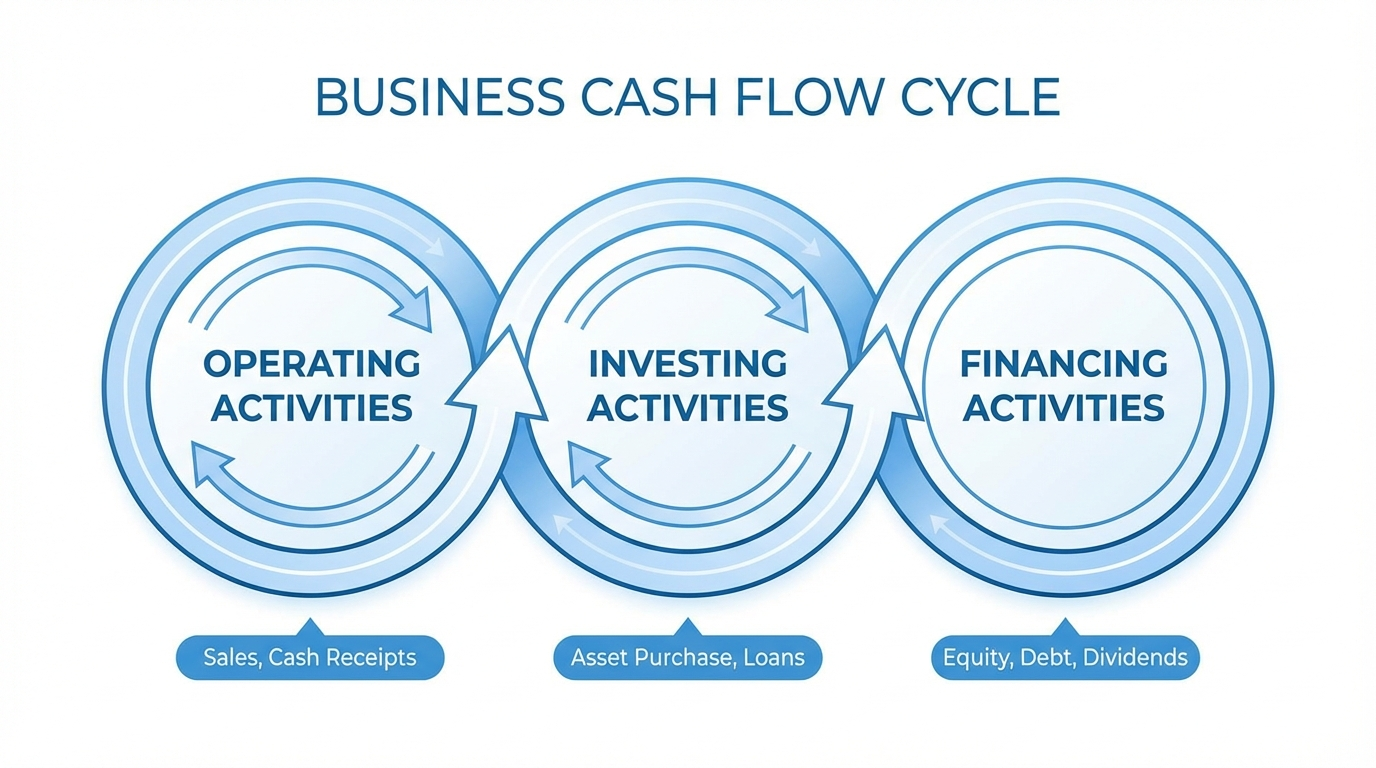

Understanding the Three Main Sections

Every cash flow statement organizes information into three distinct categories, each revealing different aspects of how a business generates and uses cash. According to research from FloQast, these three sections work together to provide a comprehensive view of financial health.

Operating Activities: The Heart of Your Business

Operating activities represent cash flows from the company's core business operations. This section answers the fundamental question: "Can this business generate cash from what it actually does?"

Common items may include cash received from customers, cash paid to suppliers for inventory, salary and wage payments, interest payments on debt, and tax payments to government authorities.

A healthy business may typically show positive cash flow from operating activities. According to Bench Accounting, this demonstrates whether a company can sustain itself without relying on external financing or selling assets.

Investing Activities: Growth and Asset Management

The investing activities section tracks cash flows related to the purchase and sale of long-term assets and investments, revealing how aggressively a company is investing in future growth.

Typical activities include purchasing or selling property, equipment, facilities, stocks, bonds, and other securities, plus making or collecting loans.

Negative cash flow here is not inherently concerning. Growing companies often show negative investing cash flows as they purchase equipment and expand facilities.

Financing Activities: Capital Structure Decisions

Financing activities encompass cash flows between the company and its owners, investors, and creditors, showing how a business raises capital and returns value to stakeholders.

Common activities include issuing new stock, repurchasing shares, borrowing money, repaying debt principal, and paying dividends.

Mature companies might show negative financing cash flows as they repay debt and return capital to shareholders. High-growth companies might show positive financing cash flows as they raise capital.

How to Prepare Your Cash Flow Statement

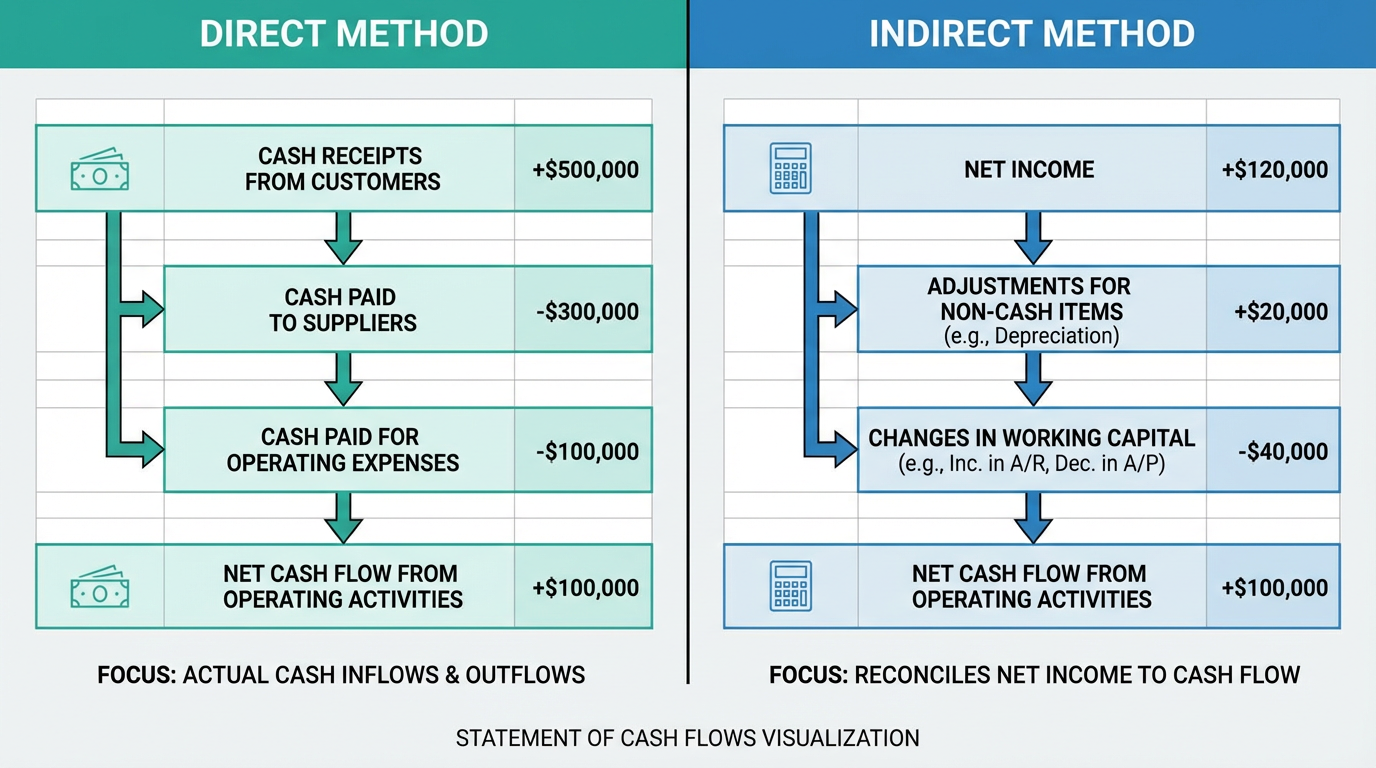

Companies can prepare cash flow statements using two accepted methods: the direct method and the indirect method. Both approaches produce identical results for investing and financing activities, but differ in how they present operating cash flows.

The Direct Method: Tracking Cash Transactions

The direct method lists all major categories of gross cash receipts and payments, including cash received from customers, cash paid to suppliers, operating expenses, interest and taxes. According to Harvard Business School Online, this approach provides more transparent information about cash sources and uses, though most companies prefer the indirect method because it requires less detailed record-keeping.

The Indirect Method: Starting from Net Income

The indirect method starts with net income and adjusts it to arrive at cash flow from operating activities. Common adjustments include adding back non-cash expenses (depreciation, amortisation), adjusting for changes in working capital accounts (accounts receivable, inventory, accounts payable), and removing gains or losses from investing activities.

For example, if accounts receivable increased, customers owe more money—revenue was recorded, but cash was not yet collected. The indirect method subtracts this increase from net income to reflect the actual cash position.

Preparation Steps

-

Gather balance sheets from current and previous periods, plus the current income statement

-

Calculate operating cash flows using direct or indirect method

-

Identify investing activities from long-term asset account changes

-

Determine financing activities from debt, equity, and dividend accounts

-

Sum the three sections to calculate net cash change

-

Verify the net change matches the difference in cash balances

Reading and Interpreting Cash Flow Statements

Understanding how to read a cash flow statement is essential for investors evaluating potential investments.

Key Metrics to Examine

Free cash flow represents the cash a company generates after accounting for capital expenditures. Calculate it by subtracting capital expenditures from operating cash flow. Positive free cash flow indicates a company has cash available for expansion, debt reduction, or shareholder returns.

Cash flow margin measures how efficiently a company converts sales into cash by dividing operating cash flow by total revenue. Higher margins may indicate better efficiency, though appropriate levels vary by industry.

Operating cash flow ratio compares operating cash flow to current liabilities. A ratio above 1.0 suggests strong liquidity.

Red Flags to Watch For

Consistently negative operating cash flow signals potential trouble, especially if it persists across multiple periods. A significant gap between reported net income and operating cash flow deserves investigation, as large gaps may indicate aggressive revenue recognition. Excessive reliance on financing activities to fund operations suggests an unsustainable business model.

Using Cash Flow Statements for Investment Decisions

For investors trading stocks, Real Estate Investment Trusts (REITs), Exchange Traded Funds (ETFs), and other securities through platforms offering diverse investment products, cash flow analysis provides critical insights that complement other financial metrics.

Evaluating Company Quality

Companies with strong, consistent operating cash flows may typically represent higher-quality investments. These businesses demonstrate their ability to generate cash from core operations without relying on financial engineering or asset sales. When evaluating stocks across multiple markets, prioritize companies showing positive and growing operating cash flows over multiple years.

Companies that generate operating cash flow substantially exceeding their capital expenditure needs have more financial flexibility for growth opportunities, economic downturns, and shareholder returns.

Industry-Specific Considerations

Different industries show characteristic cash flow patterns. Technology companies might show high operating cash flows with minimal capital expenditure needs, while manufacturing and Real Estate Investment Trusts (REITs) typically require substantial ongoing capital investment. Access to real-time market data enables investors to compare cash flow metrics across companies within the same sector.

Cash Flow and Valuation

Traditional valuation approaches focus on earnings multiples, but cash flow-based valuations provide complementary perspectives. Discounted cash flow analysis values a company based on projected future cash flows, providing an intrinsic value estimate independent of market sentiment. Companies with strong cash flow generation trading at reasonable multiples may represent attractive opportunities.

Common Misconceptions About Cash Flow Statements

Tip: While positive cash flow is generally favorable, the source matters significantly. A company might show positive total cash flow by selling assets or taking on new debt while its operating cash flow remains negative.

Many investors mistakenly view cash flow statements as technical accounting documents. In reality, these statements provide essential insights accessible to anyone who understands their basic structure. You do not need an accounting degree to benefit from cash flow analysis.

Another common confusion: profit and cash flow are not the same thing. Profit represents an accounting concept, while cash flow represents actual money movements. A profitable company can run out of cash, and a loss-making company can generate positive cash flows.

Frequently Asked Questions

What is the difference between a cash flow statement and an income statement?

An income statement shows revenues and expenses based on when they are earned or incurred (accrual accounting). A cash flow statement tracks only actual cash movements, showing when money physically enters or leaves the business.

Can a profitable company have negative cash flow?

Yes, this occurs frequently with growing businesses. A company might report profits while experiencing negative cash flow if it extends generous payment terms to customers, builds up inventory, or makes significant investments in equipment and facilities.

How often should I review cash flow statements?

For investors evaluating stocks, reviewing quarterly and annual cash flow statements provides sufficient insight into company performance. Compare statements across multiple periods to identify trends.

Why do companies add back depreciation to calculate cash flow?

Depreciation is a non-cash expense that reduces reported net income but does not involve actual cash payment. The indirect method adds back depreciation to arrive at actual cash generated from operations.

Conclusion

Mastering cash flow statements empowers investors to make more informed financial decisions. These statements reveal the true financial health of a business by tracking actual cash movements through operating, investing, and financing activities. Unlike income statements that can be influenced by accounting choices, cash flow statements provide concrete evidence of a company's ability to generate cash.

Cash flow analysis provides a crucial lens for evaluating opportunities across multiple markets. Companies with strong, consistent operating cash flows may represent higher-quality investments.

Reading and interpreting cash flow statements is foundational for evaluating opportunities across Singapore, United States, and Hong Kong markets. Explore the Longbridge app to access financial statements and market data. Learn more about essential investment concepts.